2026 CMBS Delinquency Rates

Trepp's latest data on CMBS delinquency rates. Read the report.

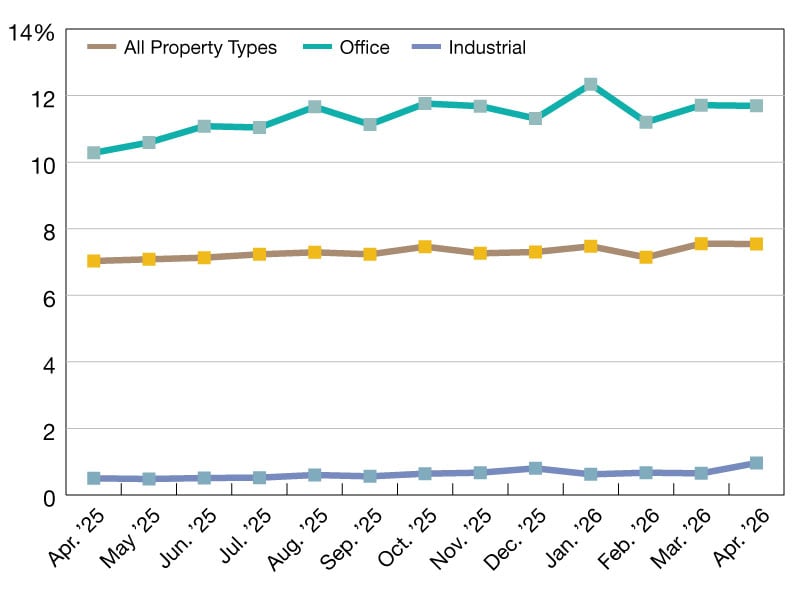

The Trepp CMBS Delinquency Rate decreased by 1 basis point to 7.54 percent in April 2026.

The five largest newly delinquent loans accounted for just over $1.26 billion of the roughly $2.63 billion in newly delinquent loans, including a Houston office loan, a New York City office loan, a San Francisco multifamily loan, a NYC multifamily loan and a national warehouse and distribution portfolio.

This month broke from the recent trend of non-performing matured balloon loans dominating the newly delinquent loan list, with 42 percent of newly delinquent loans this month being non-performing matured balloons, 40 percent were 30-days delinquent, and the remainder were in foreclosure or real estate owned (REO).

Among all newly delinquent loans, non-performing matured balloon was the most common delinquency classification, consistent with prior months.

Delinquency rates by property type

At the property-type level, two of the five major property type rates increased while three moved lower. Industrial moved modestly higher by 31 basis points to 0.96 percent due to one portfolio loan going 30 days delinquent. Multifamily increased 56 basis points to 7.71 percent, pushing above last month’s high-water mark, primarily from the two large multifamily loans mentioned above. Both went 30 days delinquent.

Lodging posted the largest decrease of 79 basis points to 6.52 percent, reversing the March increase as two large loans changed status to performing, matured balloon from non-performing. Retail had a slight markdown of 31 basis points to 6.31 percent as two premium outlet loans also became performing, matured balloons. The office rate is largely in line with March, declining 2 basis points to 11.69 percent.

READ ALSO: Why Smaller Investments Are Drawing a Crowd

If loans past their maturity date but current on interest (classified as performing matured balloon) were included, the delinquency rate would register 9.06 percent, down 1 basis point from March. This figure sits 152 basis points above the headline rate of 7.54 percent and continues to highlight the role of maturities in overall CMBS performance. The seriously delinquent rate (60+ days delinquent, in foreclosure, REO, or non‑performing balloons) also decreased, declining to 7.27 percent (from 7.29 percent).

The percentage of loan balance in the 30-day delinquent bucket is 0.27 percent, essentially flat versus March (0.26 percent).

The figures assume defeased loans are included in the denominator unless otherwise specified.

—Posted on May 22, 2026

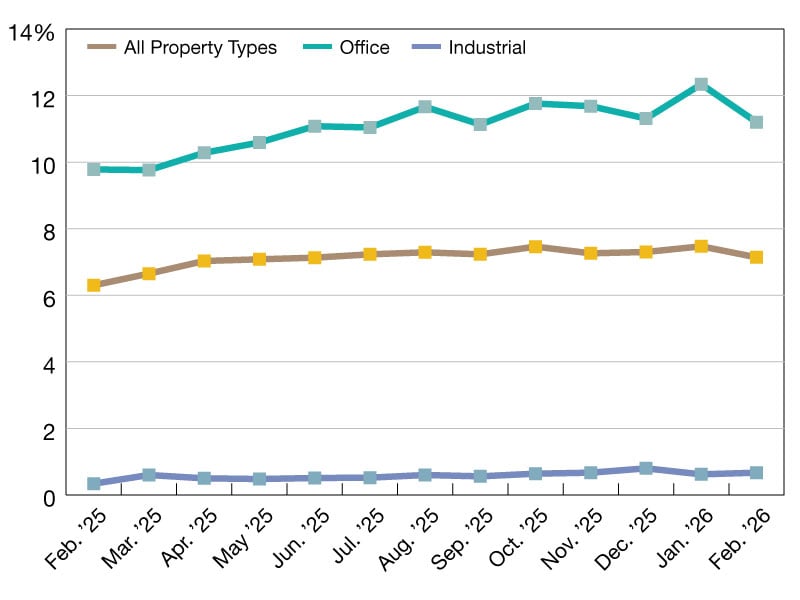

The Trepp CMBS Delinquency Rate increased by 41 basis points to 7.55 percent in March 2026, reversing February’s decline.

The five largest newly delinquent loans accounted for just over $2 billion of the almost $5.1 billion in newly delinquent loans, including a West Coast hotel portfolio, a Midwest office loan, a Northeast retail center loan, a national hotel portfolio and a Pacific Northwest office portfolio, which pushed the rate higher.

READ ALSO: Will Deregulation Turbocharge Tokenization?

In addition, roughly 40 percent of the newly delinquent loans this month were considered performing matured balloon last month. Continuing the sideways delinquency trend as loans mature, go delinquent, cure and become delinquent again.

Among all newly delinquent loans, non-performing matured balloon was the most common delinquency classification, consistent with prior months.

At the property-type level, four of the five major property type rates increased while one edged down slightly. Lodging posted the largest increase, jumping 137 basis points to 7.31 percent, the first time it has been above 7 percent since its recent April 2025 peak of 7.85 percent.

Delinquency rates by property type

Office rose 51 basis points to 11.71 percent, maintaining the elevated range established over the past year, but remaining below January 2026’s recent high of 12.34 percent. Retail increased 32 basis points to 6.62 percent, rising from February’s recent low of 6.30 percent but remaining below the higher readings observed in 2024 and early 2025, when that rate averaged 6.71 percent.

Multifamily increased 30 basis points to 7.15 percent, pushing slightly above its prior high-water mark of 7.12 percent in October 2025, and well past its marks from one year ago of 5.44 percent and 1.84 percent two years ago. Industrial dipped slightly to 0.65 percent from 0.67 percent, continuing to sit near the bottom of the major property-type delinquency spectrum.

If loans past their maturity date but current on interest (classified as performing matured balloon) were included, the delinquency rate would register 9.07 percent, up 32 basis points from February. This figure sits 152 basis points above the headline rate of 7.55 percent and continues to highlight the role of maturities in overall CMBS performance. The seriously delinquent rate (more than 60 days delinquent, in foreclosure, REO, or non‑performing balloons) also increased, rising to 7.29 percent (from 6.89 percent).

The percentage of loan balance in the 30-day delinquent bucket is 0.26 percent, essentially flat versus February (0.25 percent).

The figures assume defeased loans are included in the denominator unless otherwise specified.

—Posted on April 22, 2026

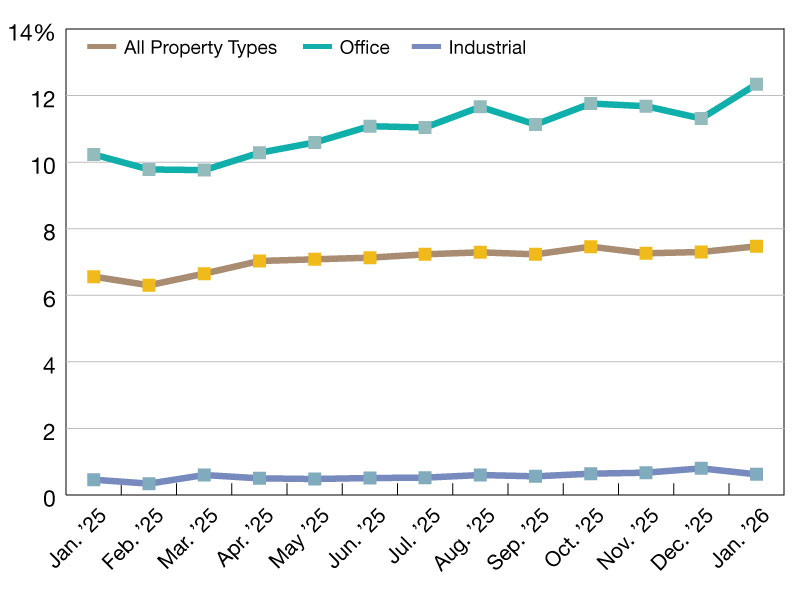

The Trepp CMBS Delinquency Rate reversed course in February 2026, decreasing 33 basis points to 7.14 percent. The decline came thanks to a net decrease in overall delinquent loan balance, which was primarily driven by the execution of modifications and extensions of five large, matured office loans and four large mall loans.

The office extensions ranged from one month to almost three years. Three mall loans received extension modifications, while the other oscillated between performing and nonperforming matured status for the past two years, as the borrower and special servicer negotiate.

READ ALSO: Strategies for Success in Commercial Real Estate

Three of the five major property types declined while two increased. Office posted the largest decline, falling 114 basis points to 11.20 percent, pulling back from January’s all-time high of 12.34 percent. The office rate has declined in three of the last four months. Retail decreased 74 basis points to 6.30 percent, the lowest retail reading since August 2024 (6.21 percent).

Rate changes across asset classes

Multifamily edged down 9 basis points to 6.85 percent. The rate sits 27 basis points below its October 2025 high of 7.12 percent.

The lodging rate increased 38 basis points to 5.94 percent following January’s 5.56 percent, which had been the lowest reading since March 2024 (5.45 percent). The sector remains below the April 2025 peak of 7.85 percent. Industrial increased 5 basis points to 0.67 percent from January’s 0.62 percent. This follows a rise from a December 2024 low of 0.29 percent to a December 2025 high of 0.80 percent.

If loans past their maturity date but current on interest (classified as performing matured balloon) were included, the delinquency rate would be 8.75 percent, down 39 basis points from January.

This figure sits 161 basis points above the headline rate of 7.14 percent and continues to reflect the influence of maturities on overall CMBS performance.

The seriously delinquent rate (60+ days delinquent, in foreclosure, REO, or non‑performing balloons) also declined, falling 20 basis points to 6.89 percent. The percentage of loan balance in the 30 days delinquent bucket is 0.25 percent, down 13 basis points from January.

Our figures assume that defeased loans remain in the denominator unless otherwise specified.

—Posted on March 25, 2026

The Trepp CMBS Delinquency Rate increased again in January 2026, climbing 17 basis points to 7.47 percent.

The increase was driven by a net increase in delinquent loans of almost $1.6 billion, primarily driven by the office sector.

For the second straight month, three of the five major property types saw increases to their delinquency rates, while two pulled back, although the mix was different in January.

READ ALSO: Cap Rates Hold Steady Across Major CRE Sectors

The largest rate increase was in office, which rose 103 basis points to an all-time high of 12.34 percent. The previous high was 11.76 percent back in October last year. The second largest rate increase was multifamily’s, which seesawed back up by 30 basis points in January to 6.94 percent, following a decrease of similar magnitude of 34 basis points the month prior.

The retail rate increased by 12 basis points to 7.04 percent, still 78 basis points off of its recent peak of 7.82 percent in March 2025, but the sixth monthly increase since the beginning of 2025.

The lodging rate saw the largest retreat, 105 basis points lower to 5.56 percent, down to its lowest level since March 2024 when the rate was 5.45 percent. The industrial delinquency rate broke its three-month streak of increases, dropping 18 basis points to 0.62 percent.

Newly delinquent loans

January’s balance of newly delinquent loans totaled just under $5.4 billion, while over $2.6 billion of delinquent loans cured over the same period, and $1.1 billion of delinquent loans paid off, resulting in a net delinquency increase of about $1.6 billion.

The office sector was the largest net contributor to the increase in the delinquency rate, while a large lodging loan that cured in January helped to offset some of the increase in the headline delinquency rate.

If we were to include loans that are beyond their maturity date but current on interest (delinquency status of performing matured balloon), the delinquency rate would be 9.14 percent, up 39 basis points from December. That is also 167 basis points higher than the headline rate of 7.47 percent, highlighting ongoing maturity-related stress.

The percentage of loan balance in the 30 days delinquent bucket is 0.38 percent, up eight basis points from December.

Our figures assume that defeased loans remain in the denominator unless otherwise specified.

—Posted on Feb. 24, 2026

You must be logged in to post a comment.