Cap Rates Hold Steady Across Major CRE Sectors

Investor sentiment is strengthening as the industry appears to be entering a new cycle.

Cap rates stabilized across major commercial real estate property types in the second half of 2025, signaling most pricing resets have already occurred, the markets are nearing equilibrium and commercial real estate appeared to enter a new cycle, according to a new CBRE survey.

Most respondents also believe yields have reached their cyclical high. However, those surveyed differed on when cap rates may begin to compress. The survey is based on approximately 3,600 cap rate estimates from more than 200 CBRE capital markets and valuation professionals in more than 50 U.S. markets provided in early December.

Responses to the survey come as volatility is easing and investor sentiment is strengthening despite continued concerns over the U.S. economy, trade policy and future interest rates.

Tommy Lee, co-head of capital markets, U.S. & Canada, for CBRE, said in prepared remarks the market is transitioning from volatility toward stability. Lee said most investors now expect cap rates to hold steady or decline. Combined with clearer risk pricing and improved capital availability, the stabilization of cap rates is paving the way for renewed investment activity, Lee stated.

READ ALSO: Investors Plan to Buy More CRE in 2026

In fact, the report noted transaction activity is rebounding with the commercial real estate market seeing transaction volume increasing by about 19 percent last year. And current trends are indicating a more active investment landscape in 2026, according to CBRE. The report noted the CBRE Lending Momentum Index is well above the prior five-year average. Several price indices are no longer falling and debt is becoming more available with higher loan-to-value ratios and more lenders entering the market. Borrowers are also finding more predictable underwriting conditions.

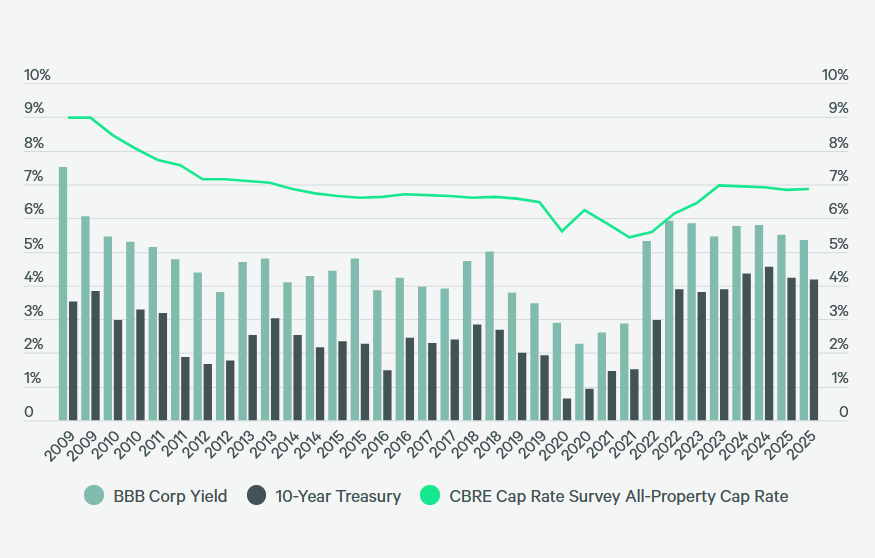

The report noted the volatility of 10-year Treasury yields that peaked in the first half of 2025 in mid-January at almost 4.8 percent continued into the early part of the summer, peaking in the second half in July at around 4.5 percent. But that volatility had eased by the end of the year, with yields ranging between 3.9 percent and 4.2 percent. CBRE stated factors included lower inflation and an expectation of continued economic growth.

Closer look at cap rate expectations

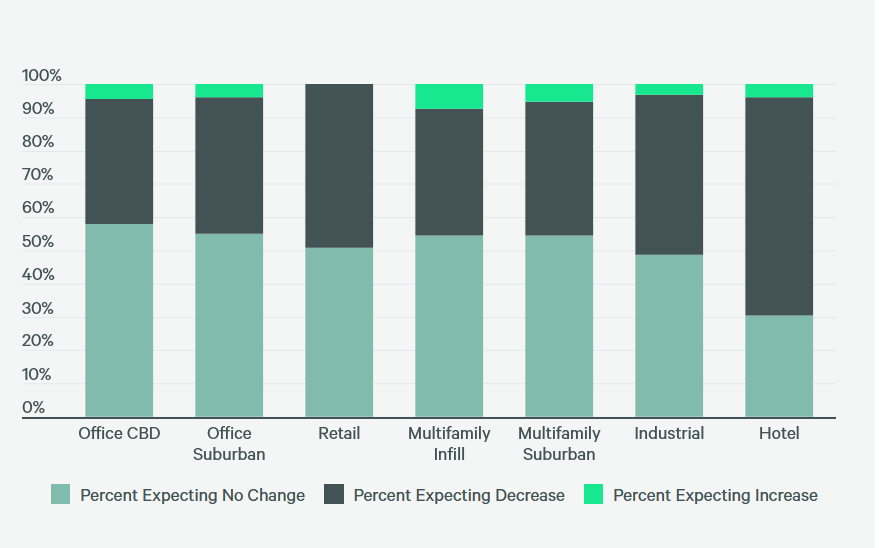

Respondents were much more optimistic about expected changes in cap rates during the next six months, with nearly 50 percent of all survey participants saying they expect retail, industrial and hotel cap rates to decline.

By comparison, in the first half of 2025 survey, nearly one-quarter of respondents believed cap rates were past their peak and would begin to decrease over the second half of 2025. In the current survey, the most common response across all categories was “no change.” However, many respondents expect decreases and unlike the previous survey, opinions are split almost equally between expecting declines and no change.

Changes seen in office data

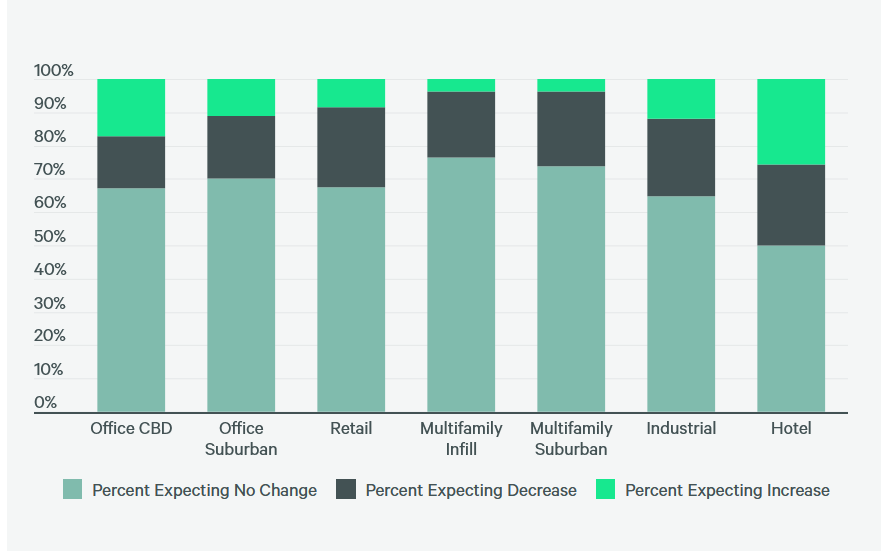

Shifts between cap rate expectations were seen between the first half and second half of 2025 surveys from respondents predicting increases in cap rates for CBD office and suburban office. The survey also noted the average spread between lower and upper office yield estimates had stopped widening in the second half of 2025 for the first time since 2022. CBRE stated those changes show the office sector is continuing to stabilize with more emphasis on market pricing.

“The office landscape remains incredibly diverse, with prime, well-located assets trading in a functional market while distressed product continues to work its way through the system,” Matt Carlson, an executive vice president & co-head of office capital markets for CBRE, told Commercial Property Executive.

“We’re seeing a wide disparity in pricing and performance that varies significantly by location, product type and market-by-market dynamics. That divergence will continue to define valuations and cap rates as we move through 2026,” Carlson added.

You must be logged in to post a comment.