CRE Lending Momentum Improves

Growth in permanent loan financing was a big ingredient in six months of progress.

As 2025 closed out, lending conditions for commercial real estate extended their recent winning streak, CBRE said in a new report. The reason for this improvement is multifaceted, CBRE stated, and includes higher loan origination volumes, increased average loan sizes, relatively stable spreads and improved loan-to-value ratios.

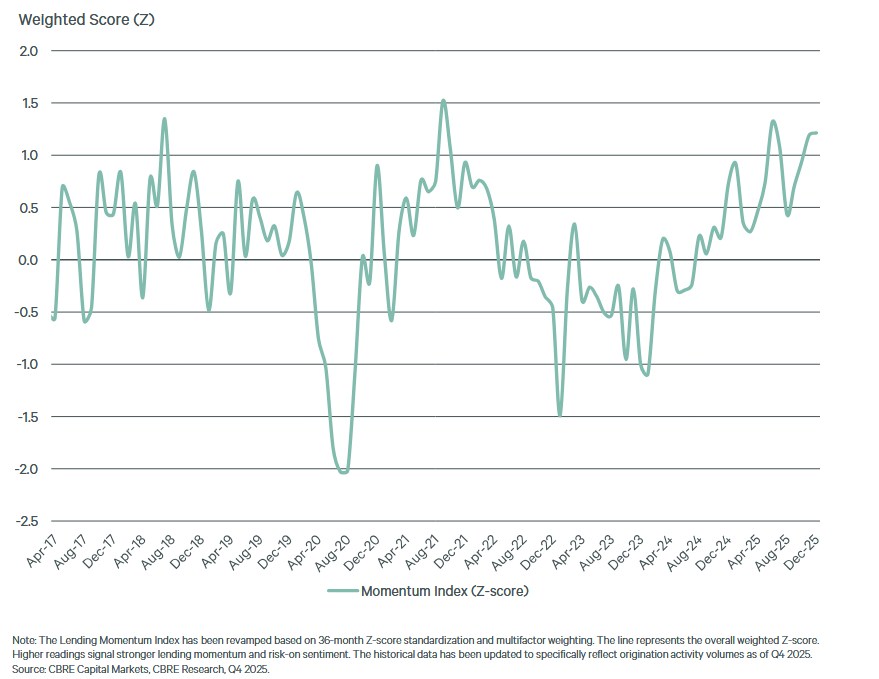

As Commercial Property Executive reported last November, CBRE’s third-quarter Lending Momentum Index (which tracks CBRE-originated commercial loan closings in the U.S.) reached its highest level since 2018—1.04—buoyed by stabilizing borrowing costs and tighter spreads, along with a major year-over-year increase in permanent loan financing.

Well, that was then, and this is now, and now is even better, as the index at year-end hit 1.2. That was a 67 percent year-over-year increase, to a level that CBRE says is comparable to 2018. That degree of growth, the company explained, “was driven by a 26 percent year-over-year increase in permanent loan financing, with December marking the highest monthly level since 2021.”

CBRE is seeing a bifurcated but increasingly healthy commercial real estate lending market, where rising delinquencies and legacy loan sales in the secondary markets are being readily absorbed by a deep pool of capital, according to a statement by James Millon, the firm’s president & co-head of capital markets, U.S. & Canada. He added that credit spreads continue to tighten, backed by a strong liquidity profile and nearly 100 percent market participation.

READ ALSO: Navigating the Distressed Asset Life Cycle

Spreads on commercial mortgage loans in the fourth quarter were unchanged from the previous quarter, at an average of 197 basis points. These figures are based on fixed-rate, seven- to 10-year loans with 55 percent to 65 percent loan-to-value ratios, CBRE explained.

Into the specifics

Among non-agency loan closings in the fourth quarter, alternative lenders, including debt funds and mortgage REITs, dominated at 40 percent of total volume, up substantially from 23 percent a year prior. Debt funds were the main player, with their lending volume increasing 112 percent year-over-year.

The second-largest slice of non-agency closings came from banks, at 35 percent, which was down from 43 percent a year earlier. CBRE added, however, that “bank origination volume increased 73 percent quarter-over-quarter, reflecting continued re-engagement in the market.”

Third place was occupied by life companies, which totaled 19 percent of non-agency loan volume in the fourth quarter, down from 33 percent a year ago.

In last place, although with their own momentum, CMBS lenders represented 7 percent of non-agency loan volume, up from just 1 percent the prior fourth quarter. This lending volume, CBRE observed, was “supported by active private-label CMBS issuance, as market-level issuance reached $158 billion in 2025, its highest annual total since 2007.”

On the underwriting side, the report stated that the major metrics improved a bit in the fourth quarter, mirroring broader trends in commercial real estate. Loan constants and mortgage interest rates declined by 10 and 15 basis points, respectively, from the third quarter, as debt service coverage ratios increased to 1.36, from 1.35. And despite overall lower borrowing costs, “lender prudence persisted, with debt yields increasing 9 basis points to 9.8 percent.”

Finally, average commercial real estate LTV ratios increased to 60.9 percent in the fourth quarter, a modest rise from 60.0 percent a year earlier, “reflecting a modestly less conservative approach by lenders.”

You must be logged in to post a comment.