Why Retail Shines On

Most metrics are looking up, according to a new CBRE report.

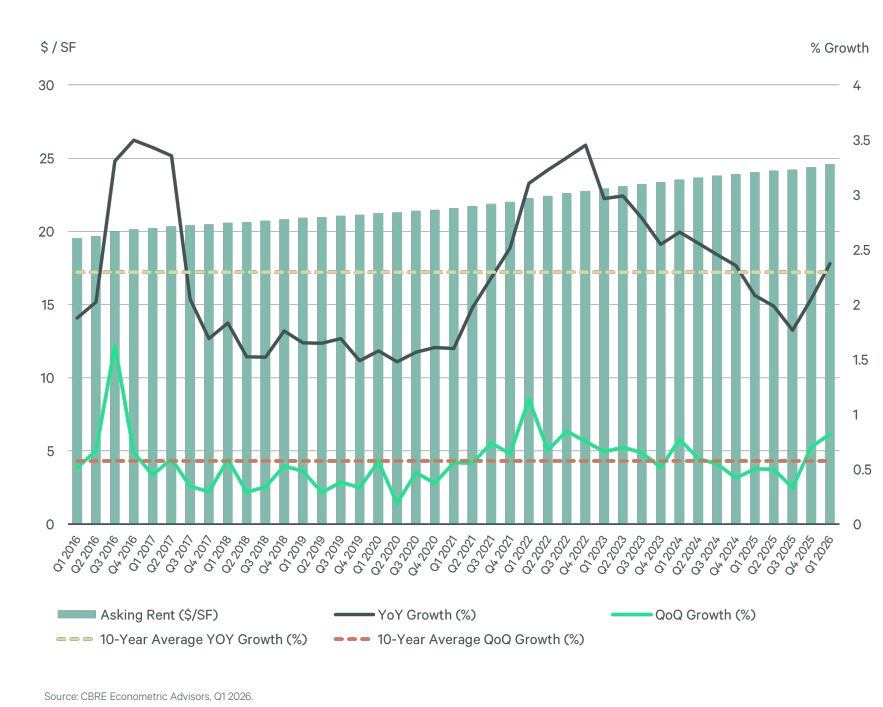

As retail deliveries stall, rents continue their upward trajectory. The growth rate edged out the 10-year average, with an annual rent increase of 2.4 percent through March, according to the latest CBRE quarterly retail report.

Meanwhile, three consecutive quarters of positive net absorption kept the availability rate low, at just 4.9 percent at the end of the first quarter. However, the reading was 10 basis points higher compared to the one registered in December 2025 on account of several high-profile store closures, such as the ones triggered by Saks Global’s Chapter 11 bankruptcy.

This space may not remain vacant for long, as a new tenant dynamic emerges. “Last year was the first time that more retail space was leased by service tenants than by tenants selling actual goods, which reflects the general shift in consumer behavior away from goods and toward services,” Ebere Anokute, Head of Retail Research for the Americas at CBRE, told Commercial Property Executive.

Record-low retail deliveries also placed downward pressure on the availability rate. During the first quarter, just 4.7 million square feet of retail space came online, the lowest quarterly figure ever recorded by CBRE.

A combination of factors including rising construction costs, a shortage of jobs and a lack of available development land leads to a tempered retail pipeline outlook, Anokute reasoned. “If interest rates come down in the near term, it’s possible that could lead to more construction financing, but that’s not what we’re seeing currently. The pipeline will likely remain measured in both the near and long term.”

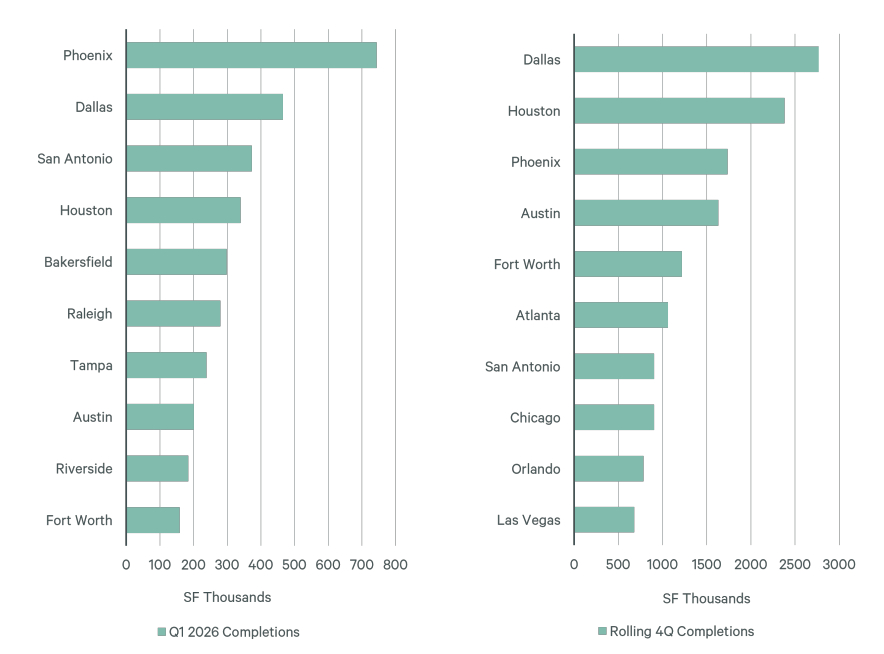

Retail deliveries soar throughout the Sun Belt

Markets across the Sun Belt stood out as having the highest delivery count, with Texas metros taking up five of the top 10 entries across the rolling four-quarter completion count.

“Although most new retail development is in the Sun Belt, the overall levels of development that we’re seeing are still at historic lows. The strong population growth in the region is underscoring retail real estate demand, so while that continues, the balance between supply and demand should remain healthy,” Anokute claimed.

Indeed, while Sun Belt metros had the highest development activity, many of the same markets also topped the absorption metrics. For instance, new construction projects in Phoenix bumped the market into first place for both retail deliveries and absorption volumes during the first quarter.

READ ALSO: Unlocking the Sun Belt’s Retail Potential

This region’s performance hasn’t gone unnoticed by investors. Just last month, Ares Management Corp. entered a definitive merger agreement with Whitestone REIT. The $1.7 billion deal includes a nearly 5 million-square-foot portfolio of retail assets across Phoenix, Dallas, San Antonio, Houston and Austin, Texas.

Location drives an even steeper performance gap

The dominance of the Sun Belt coincides with the divergence between downtown and suburban retail performance, both fueled by hybrid work arrangements and ongoing domestic migration. The availability chasm between downtown and suburban retail properties clocked in at 137 basis points in March.

Investment followed throughout markets with a heavy suburban tilt, such as the Inland Empire. Two months ago, one of the largest Southern California deals closed when Brookfield Properties sold the 1.2 million-square-foot Victoria Gardens in Rancho Cucamonga, Calif.

However, downtown owners can stay competitive by taking advantage of the daytime population that congregates in and around their properties, likely office buildings, Anokute concluded. This can include agreements with tenants that cater to the needs of office workers, such as dry cleaners, nail salons or boutique fitness companies.

You must be logged in to post a comment.