M&A Activity to Rebound This Year

Data centers are still the star, but one property type is making a comeback.

This year, commercial real estate mergers and acquisitions activity is expected to outpace 2025, according to a new report by Deloitte.

Last year, the pace of M&A activity came in slower than expected, constrained by rate uncertainty and widening valuation gaps, though the data center sector and public-to-private sectors saw heightened activity.

“After 2025’s historic decline in deal value, the CRE M&A market is entering 2026 with abundant capital and renewed buyer leverage,” Deloitte Managing Director, Real Estate M&A and Restructuring Services Leader Jonathan Keith told Commercial Property Executive. “But success will come down to timing and conviction. The opportunity is there, but investors who can navigate uncertainty and act decisively will be best positioned to capture it.”

In 2026, with capital abundance and timelines tightening, investors appear willing to accept that today’s rate environment may represent a new normal, the report noted. The question now isn’t so much whether activity will return, but where those deals will be—unless geopolitics gets in the way. That is still a wild card.

“Evolving geopolitical instability—particularly in the Middle East—has introduced an additional layer of uncertainty that could influence energy markets, inflation expectations, and broader investor sentiment,” the report explained.

READ ALSO: Will Deregulation Turbocharge Tokenization?

“While it remains too early to assess the full implications for real estate capital markets, the question for the remainder of 2026 may be less about whether opportunities exist and more about who’s prepared to act on them—and where.”

Macroeconomic considerations

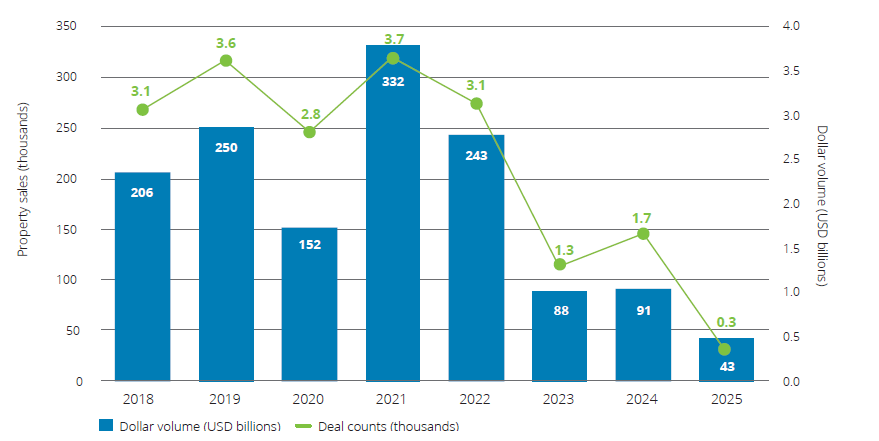

Last year, there were 43 M&A deals in the U.S. commercial real estate sector, with a dollar volume of $300 million, down from 91 deals totaling $901 million in 2024. But both of those years were dwarfed by the early 2020s, especially the low interest-rate environment of 2021, when 332 U.S. deals totaled $3.7 billion. The market in 2025 was driven by opportunistic or highly targeted transactions, Deloitte noted.

As interest rates started to rise, many sellers extended hold periods in hopes of lower financing costs. At the same time, buyers struggled to underwrite deals in the face of higher rates and uncertain exit assumptions. M&A deals in the industry slowed down.

Now the picture is in flux.

The anticipated transition in Federal Reserve leadership, and the potential recalibration of monetary policy that may follow, adds another layer of uncertainty. But lower rates are now a distinctly possible policy trajectory.

Even so, predictability may matter more than dramatic cuts, the report posited.

“Financing remains broadly available, particularly through private credit and alternative lenders, and a steadier policy backdrop could help valuation expectations reset,” Deloitte reported. “Together, these dynamics may release a backlog of recapitalizations, portfolio sales, and platform-level transactions that have been building beneath the surface.”

Data centers still the star sector

In CRE M&A, data centers are still the sector to watch, the report found. Demand tied to artificial intelligence, cloud computing and digital infrastructure continues to attract investors of all stripes: private equity, sovereign wealth funds, infrastructure investors and other strategic operators.

CBRE’s $1.3 billion acquisition of Pearce Services, completed in November 2025, is a solid example of capital’s ongoing inclination toward scaled digital infrastructure platforms, Deloitte said.

Nevertheless, the structure of transactions may shift in 2026. Many large public platforms have already been taken private or recapitalized, and competition for stabilized data center assets is intense. As a result, activity may concentrate more on joint ventures, campus expansions, and development partnerships, as opposed to outright platform acquisitions.

Also, local factors are going to determine the patterns of growth for the sector. Competition for assets is going to intensify even more, energy will face constrains, and permitting timelines will remain uncertain, as will community and official pushback against the growth of the sector.

Office is no longer out of bounds

In several major U.S. markets, return-to-office trends have raised occupancy in high-quality buildings, and investors are showing greater willingness to jump back in the market in places where tenant demand is visible. Newer, amenitized properties in markets such as New York City and select West Coast cities are attracting renewed interest.

In late 2025, Rithm Capital’s acquisition of Paramount Group and its portfolio of office assets, all Class A, illustrated how capital can reenter the sector when basis and quality align, the report noted.

“Yet the divide within office remains pronounced,” the report says. “Older Class B and Class C properties continue to face structural headwinds, and the capital required for repositioning often competes with uncertain leasing prospects.”

That dynamic may create selective distressed or value-driven opportunities, especially where conversion to residential or alternative uses is feasible. Public-private incentives may accelerate office-to-residential and mixed-use conversions, with government support. Overall, office deal activity may increase in 2026, but transactions are likely to remain highly asset-specific rather than broad-based, Deloitte predicts.

You must be logged in to post a comment.