Working Out Distressed Office—One Square Foot at a Time

Why lenders and borrowers are still pacing themselves as demand evolves.

Many commercial real estate lenders will tell you the “extend-and-pretend” phase for office buildings is over, but that doesn’t mean they’re eager to own a bunch of marginalized assets. Instead of the foreclosure dramas that played out in previous cycles, lenders and special servicers are trying to eke out as much value as possible from properties while keeping the borrowers in place.

In some cases, they continue to extend or modify loans in hopes that a leasing recovery at the local level will improve a dire financial condition. In other instances, they’re hoping that a buyer will pay enough to minimize a loss, especially for less desirable properties or those that can be converted into other uses, such as residential.

“We’re seeing dribs and drabs of resolutions because we don’t have a heavy hand forcing distressed properties to mark values to market,” said Shlomi Ronen, founder & managing principal of Dekel Capital. “It’s not like the great financial crisis, where assets were repriced within two years and we knew we were at the bottom.”

A deep market

With plenty of distress to work through, the office market is unlikely to return to a sense of normalcy anytime soon. Some $63 billion in office assets remained in distress at the end of the first quarter of 2026 vs. $54 billion a year earlier, according to MSCI Real Assets.

On the plus side, the company noted that future distress in the office sector is declining—a projection of $68.9 billion vs. $88.4 billion some 12 months prior.

Moreover, the CMBS office loan special servicing rate of 16.75 percent in May represented a decline of nearly a percentage point from April and was heavily influenced by two big New York office loans that were extended and modified, according to Trepp. The rate was still a percentage point higher than a year earlier, however.

READ ALSO: What the Debt Maturity Wall Means for Investors

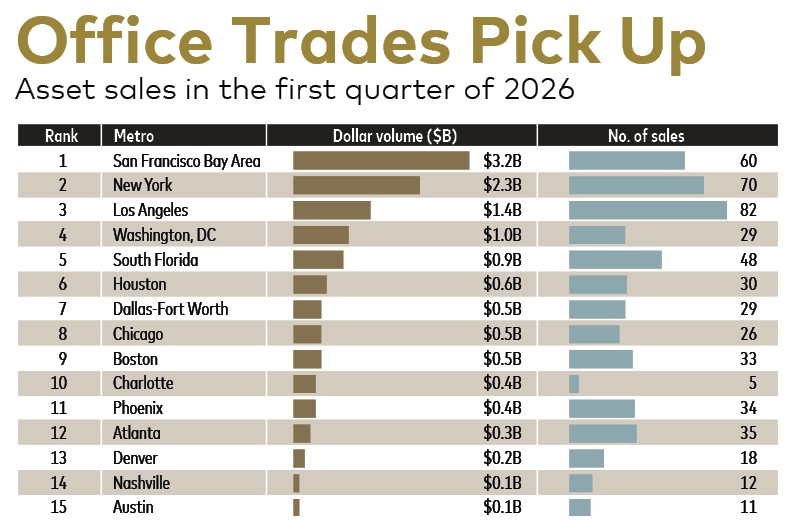

Meanwhile, office sales reached $20.5 billion in the first quarter, a year-over-year increase of almost 39 percent, according to Avison Young. Roughly 5.9 percent of the 1,159 deals represented distressed sales, the brokerage reported. Since 2022, the percentage of distressed sales has typically ranged between 4.4 percent and 6.6 percent.

Beyond the slower pace of resolutions, this round of office distress differs from the GFC in more deep-seated ways, observers say. A credit shock caused the GFC, and borrowers and lenders tended to butt heads regarding loan extensions, loan restructurings and short sales. Still, neither side could fathom the notion that corporations would stop leasing space.

That wasn’t the case following the pandemic. Not only did the lockdowns illustrate that people could work from home but they also exposed a glutted office market, as tenants reduced their space needs and upgraded to high-quality buildings in a discounted environment. Combined with the spike in interest rates that pummeled property values, the new occupier paradigm has fostered a spirit of collaboration between lenders and borrowers, noted Jim Costello, executive director & co-head of the MSCI Real Assets research team.

“The most common approach to resolving distress in the GFC was the lender would take the property through a foreclosure and then sell it, but it was painful because sponsors fought to keep their properties,” he pointed out. “This time, sponsors and lenders are trying to find the best solution together because they’re dealing with an asset that doesn’t have the same fundamental economic value that it did before the pandemic.”

Working out strategies

Such cooperation can help fetch a better price for an asset in a short sale vs. selling the note at a discount, noted Matt Carlson, an executive vice president & co-head of U.S. capital markets at CBRE. Loan sales typically don’t include a lot of property due diligence or tours, and Carlson has seen a number of would-be loan sales turn into consensual short sales thanks to the sponsor’s involvement in the marketing process. The arrangement has the added benefit of allowing the sponsor to avoid foreclosure.

READ ALSO: $100B in CMBS Loans Mature This Year. Here’s What’s Ahead.

“There have been situations where the borrower has said: ‘We’re out of money, but we want to maintain the strong relationship with this lender, and we’re going to do everything we can to help them,’” said Carlson. “Lenders are also aware that the best scenario is to work with the sponsors because they know all the leasing details and have the best information about the building.”

Lender type often dictates how resolutions progress, observed Erik Edeen, a principal & senior director of U.S. investment sales for Avison Young. Balance sheet lenders that want to avoid absorbing a big loss will typically write down their loans over time before executing a short sale, for example. In the CMBS market, distressed loans first go on a watchlist and eventually enter special servicing where they can spend several quarters or years while the servicer figures out the best management, leasing and disposition strategy, he added.

READ ALSO: Who’s Winning, Who’s Losing in the CMBS Space

Case in point: Avison Young was recently assigned the listing for a two-building, 318,945-square-foot office park in suburban Atlanta that was part of a larger Adventus Realty Trust CMBS foreclosure in late 2024. The brokerage managed and leased the buildings on behalf of special servicer Rialto Capital and increased occupancy to 85 percent from 78 percent before the decision to sell was made.

“I think we’re getting to a place where leasing is rebounding in certain markets, but there’s always some calculation as to whether a market is only temporarily distressed or if it isn’t going to get much better over the long term,” said Edeen. “I don’t know if a major bounceback is going to be available in a lot of assets that have yet to see some green shoots.”

Discounts only go so far

To date, private investors are driving the lion’s share of distressed transactions as institutional investors stay on the sidelines, observers say. But opportunistic office buyers need to look beyond discounts relative to prior value or replacement cost, advised Mark Green, CIO of Cottonwood Group, an investment firm focused on CRE private equity and debt that closed a $1 billion special situations fund in August 2025.

Among other variables, Green suggested buyers needed to realistically assess the long-term demand for an asset, the likelihood of a refinancing down the road, and the amount of capital needed to stabilize the property, including multiple years of leasing costs. Cottonwood is evaluating potential distressed office deals, and Green expects the opportunities to grow. But the firm remains highly selective even as price discovery and leasing activity improve.

“Many office assets remain burdened by upcoming maturities, refinancing challenges, capital expenditure requirements and ownership structures that are increasingly difficult to sustain in the current environment,” he said. “We believe the market requires significant differentiation today—not all distressed opportunities are attractive simply because they are distressed.”

You must be logged in to post a comment.