$100B in CMBS Loans Mature This Year. Here’s What’s Ahead.

And how the market’s recalibration presents both risks and opportunities for investors.

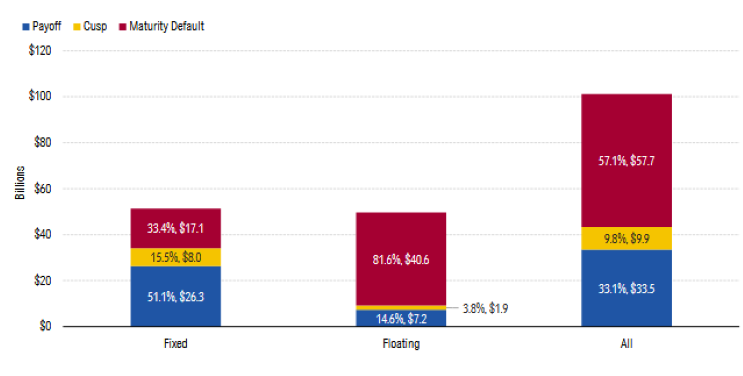

More than $100 billion in fixed- and floating-rate CMBS loans are maturing this year, according to Morningstar’s commercial real estate outlook for 2026. Over half of these loans will not repay at maturity, the report found.

More specifically, Morningstar expects that about $57.7 billion will have a maturity default, with a further $9.9 billion on the cusp between default and payoff.

The outlook states that while the most troubled assets may be slated for foreclosure and other liquidation resolution strategies, many loans are expected to be approved for modifications to extend the maturity dates and provide the borrowers with more time to secure replacement financing and/or stabilize the collateral properties.

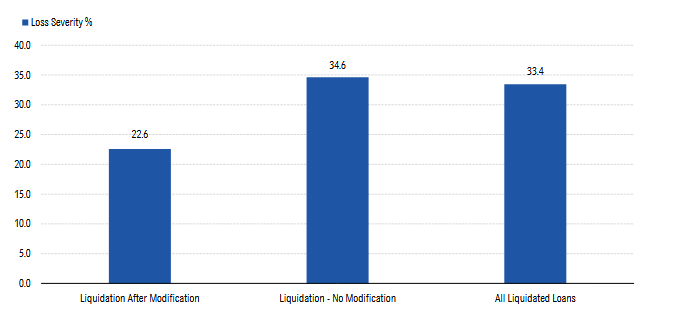

Further, “the historical data suggest that modified loans are ultimately resolved with lower loss severities compared with loans without modifications.” Morningstar’s own analysis of loss severities for loans liquidated between 2010 and November 2025 shows a 12 percentage point decrease in liquidations after modification.

“The CMBS maturity wall in 2026 should be viewed less as a systemic shock and more as a clearing mechanism,” Kidder Mathews Senior VP Mike King told Commercial Property Executive. “Many loans coming due were originated at peak valuations, and the inability to refinance reflects structural repricing rather than sudden deterioration in asset performance. Brokers are increasingly involved earlier, helping lenders and borrowers assess exit paths well ahead of maturity.”

“The market is not broken,” he concluded, “it is recalibrating, and that recalibration is creating both risk and opportunity.

Integra Realty Resources CEO Anthony Graziano’s thoughts are similarly temperate: “The CMBS maturity wall warnings have been a consistent predictive theme for over a decade, but nearly every warning has proven unfounded.”

He added that the forecast conclusion is on point; however, 2026 will see more kicking of the can down the road as servicers and investors wait for value recovery.

“The hidden headline in the data is the gap between acquisition and refinancing cap rates,” Graziano said. He explained that the acquisition market is targeting higher returns to capital, leaving existing assets stuck in limbo refinancing at values that are not well-supported by the acquisition market, adding that the overall value of assets needs to consider required returns to equity in the capital stack.

“The report calls for declining cap rates as overall interest rates come down, but that forecast ignores any possibility for equity surcharges considering transaction illiquidity and underlying risks of elevated valuations throughout the market,” he added.

Graziano concluded that the entire market is caught in the squeeze play of whether to put good money after bad following a short 2021–22 period of quickly escalating prices, and the ensuing pickle of escalating rates against a much more volatile economic and policy backdrop.

READ ALSO: Will Stability Win Over Volatility in 2026?

Abby Corbett, global head of investor insights & principal economist at Cushman & Wakefield, said it’s important to clarify that of the more than $1 trillion in commercial real estate loans maturing over the next two years, “only about 15 percent of these maturities sit within the CMBS universe between now and 2034, distributing risk across a wide range of lenders.… while refinancing needs are undeniably large, the data points to a multiyear workout cycle, similar to the adjustment following the GFC, rather than a sharp, near-term systemic shock.”

She noted that refinancing activity is already exceptionally strong, adding that “U.S. refinance origination volume is up 42 percent year-over-year, the highest level on record outside the 2020–22 low-rate era.” Meanwhile, tight corporate bond spreads continue to push institutional investors toward commercial real estate debt in search of relative yield, fueling a more than 50 percent surge in private real estate debt fund formation. “These funds (often targeting transitional assets or maturity-driven opportunities) are expanding the menu of recapitalization and refinancing options even for challenged segments.”

From a historical perspective, Corbett said, consider that while “outright distressed sales and acquisitions have risen from virtually zero to 2.7 percent of sales, this still pales in comparison to the GFC peak of roughly 10 percent.” And there is substantial opportunistic private credit and equity capital actively seeking these situations, creating a competitive buyer pool for assets that do come to market, she observed. “Taken together, these dynamics suggest a sector working through a necessary recalibration, not one facing an imminent systemic break.”

Negative office outlook—or not that bad?

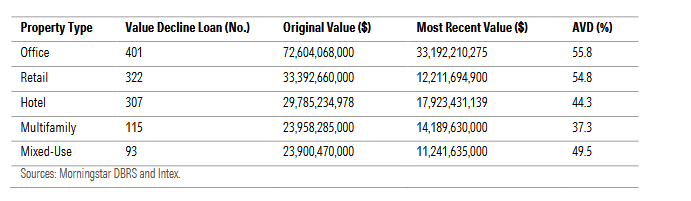

Along with acknowledging the ongoing bifurcation of the office market and the sector’s sensitivity to individual market and property dynamics, the Morningstar outlook highlights servicer reactions to interest shortfalls, likely being “driven by the severity of the declines in appraised values from the issuance appraisals when properties are re-valued following a default.”

The average value decline from the original appraisal to the most recent appraisal in a dataset of about 1,250 loans is the highest—at 55.8 percent—for office properties. Overall, Morningstar’s outlook on office for 2026 is negative.

“In New York City, office fundamentals began to meaningfully recalibrate in 2025, driven by a clear bifurcation between high-quality assets and obsolete stock,” David Giancola, senior managing director, JLL Capital Markets, New York, told CPE.

He added that vacancy statistics alone can overstate weakness, as a significant portion of vacant space sits in buildings that are being converted or are no longer competitive. “That structural supply reduction is quietly tightening effective availability and supporting leasing momentum at the top of the market.”

“From an office finance perspective,” he continued, “this matters because lenders and investors are underwriting real performance—tenant demand, utilization trends and achievable rents—rather than broad sector sentiment.”

READ ALSO: Return-to-Office Numbers Hold Strong

Marianne Skorupski, director of National Office Research | U.S., at Colliers, emphasized the volume of investment in the office sector. She remarked that “office investment activity has continued to rebound, with total volume reaching $73.3 billion in 2025, up 15.8 percent from the previous year. While this figure remains significantly lower than the $142.2 billion in transactions recorded in 2021, the growth seen in 2025 signifies the second consecutive annual increase in volume. The number of properties traded reached 4,820, representing a 10 percent increase from 2024.”

Skorupski noted the Bay Area’s 2025 surge in office investment, driven by leasing from AI companies. She added that improvements in office leasing fundamentals nationwide are fostering cautious optimism for a sustained recovery.

“Investors are identifying opportunities through distressed sales, acquiring properties at a discount, and subsequently making capital improvements to attract new tenants. In multiple markets, buildings are being traded in anticipation of redevelopment, as non-competitive properties are earmarked for conversion to alternative uses.”

Don’t bet against the US consumer

While Morningstar’s overall 2026 credit outlook for office is negative, the company rates retail as stable. That’s despite an average value decline of 54.8 percent, nearly equal to that of the office sector, with about $18 billion in retail loans scheduled to mature in 2026. Still, Morningstar describes the retail sector as “pockets of stress related to oversupply and/or obsolescence in some markets and asset classes.”

Though one of retail’s saving graces is limited new supply, Morningstar noted “mixed sentiment around the health of the consumer, with some observers stating that lower interest rates and inflation could strengthen consumer purchasing power in 2026. However, it is still unclear what will happen if, in 2026, unemployment continues to trend upward and tariffs affect the cost of goods.”

Scott Aiese, senior managing director, JLL Capital Markets, is somewhat more bullish. “Retail stands out as one of the healthiest components of the investment market heading into 2026. Years of structural adjustment have fundamentally reset retail’s supply-and-demand dynamics, positioning the sector far more defensively than many investors once expected.”

He added that new construction has slowed dramatically, vacancies are at historic lows and tenant demand continues to expand, particularly for well-located urban and neighborhood retail. These conditions are supporting rent growth and attracting institutional capital that had largely stepped away from the sector over the past decade.

READ ALSO: High-Street Retail Regains Traction in the ‘New’ Downtown

“From a capital markets perspective,” Aiese commented, “this is translating into more attractive financing conditions, as lenders are showing increased appetite, cap rates have converged with other asset classes and transaction activity is accelerating.”

For her part, Nicole Larson, manager, National Retail Research | U.S. at Colliers, is similarly optimistic about the retail sector, predicting that “amid a period of modest global growth, stabilizing inflation, and income gains, the retail sector is poised to deliver the most substantial total returns worldwide between 2025 and 2029. Retail stands out for its combination of steady yields, resilient income performance, and more balanced valuations following several years of adjustment. With total returns forecast to average 6.5 percent annually, retail is positioned to outperform all other major sectors.”

The sector’s “recalibrated fundamentals and improved yield profile make it one of the most compelling opportunities across the commercial property spectrum,” Larson told CPE. “Many institutional players remain under-allocated to the asset class, offering upside potential for transaction volume in the year ahead.”

You must be logged in to post a comment.