BOMA Special Report: CRE’s Recovery is Here

BOMA International President and COO Mary Lue Peck reported that while capital is returning, not all asset types and classes are benefiting.

The CRE industry has moved beyond the capital paralysis observed in 2024 and 2025, but success continues to vary widely across asset types and classes, BOMA International President and COO Mary Lue Peck argued in her annual State of the CRE Industry address. The talk came on the second full day of the organization’s annual conference and expo in Long Beach, Calif.

Seventy percent of senior executives say capital is more accessible now than it was last year, Peck reported, and more than half expect property values to rise.

“The recovery is here,” Peck proclaimed. “It is selective, and it is very, very uneven. But it is here.”

READ ALSO: BOMA Day One Takeaways: Staying Human in the Age of AI

Investors are now evaluating operational performance when looking at assets, moving beyond traditional underwriting metrics. They want to understand in granular detail the costs of maintaining a particular building, along with the tools the current team has deployed to bring down those costs, Peck argued.

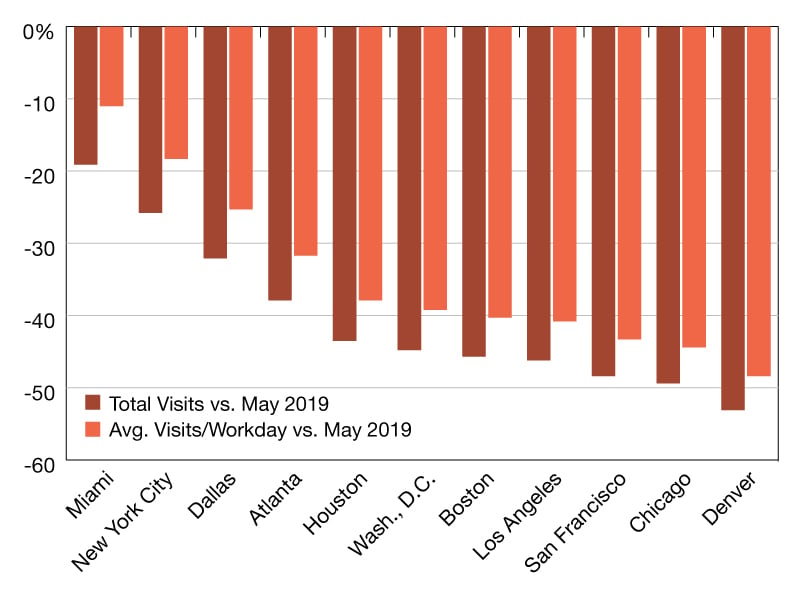

And in the modern hybrid work environment, office property managers need to admit that some days of the week—such as Fridays—will likely lead to much lower building utilization rates, while so-called peak days can bring buildings near their full capacity once again.

This means that building services, staffing and energy uses need to be flexible and account for real-time demand.

“The planning challenge isn’t the monthly average or the daily average,” Peck said. “It’s the peak day.”

The kinds of buildings that attract capital

The industry remains extremely bifurcated in terms of investment volume, vacancy rates and access to capital, something that CRE experts highlighted in a recent CPE webinar on the industry’s midyear outlook.

Peck pointed to the May Yardi Matrix national office report, which showed more than 85 percent of the national office construction pipeline is for Class A space. At the same time, distress continues to rise across the sector. Since 2024, distressed properties accounted for 19.4 percent of the 800 million square feet of space that changed ownership—up 6.2 percent from the deals closed between 2021 and 2023.

The recovery is increasingly benefitting smarter buildings that can provide detailed insights into their daily operations.

“The ones that are attracting capital today behave more like living systems,” Peck said. “They generate data, they respond, they adapt, and they tell their owners how they’re performing in real time.”

This bifurcation extends into the industrial sector as well. While the latest Yardi Matrix national industrial report found that in-place rents were up 5 percent and vacancy has plateaued, according to Peck, these figures don’t tell the whole story. Higher clear heights, flatter floors and access to power are among the key differentiators in industrial demand right now.

“The takeaway isn’t that the sector is soft,” she said. “It’s that the premium is narrowing to buildings that earn it, and right now that comes down to location, operations and resilience.”

You must be logged in to post a comment.