LaSalle IM: Why 2026 Feels Like ‘Groundhog Day’ for CRE Investing

It's not quite a repeat of 2025, but there are a lot of common themes. Here's how the firm has adjusted its strategy.

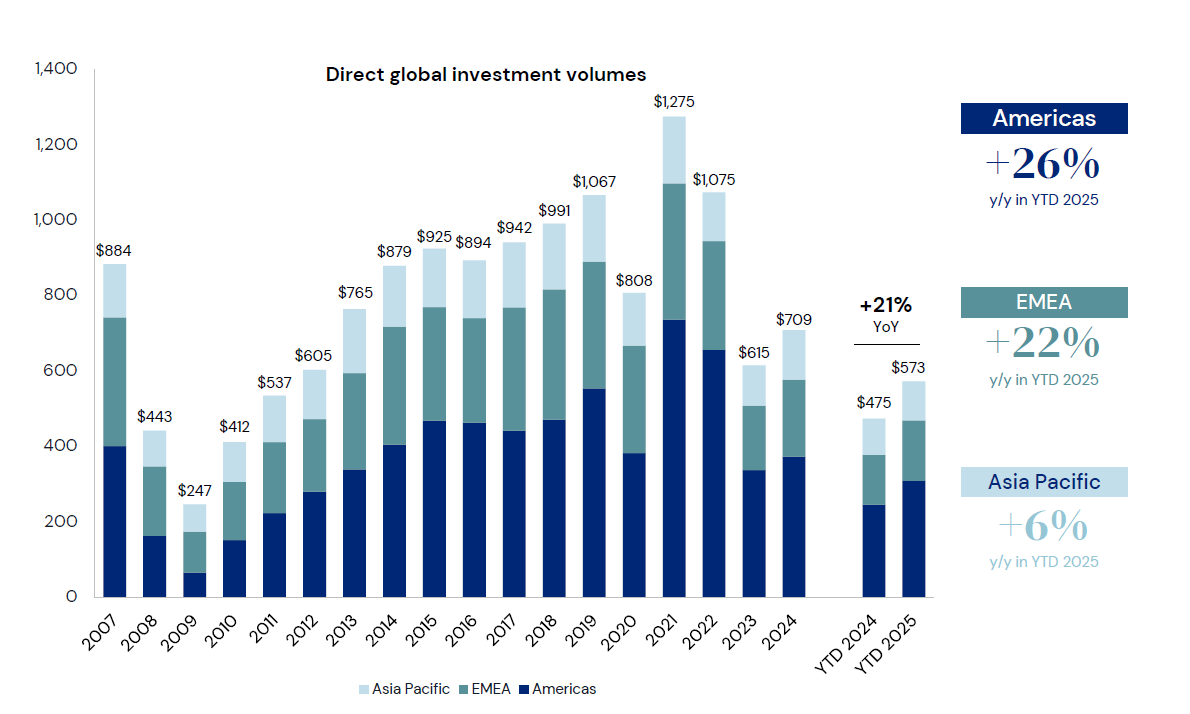

Commercial real estate investment going into 2026 feels like the start of a new cycle, with distinct causes for both optimism and concern. If these sentiments sound similar to those held by many in the industry at the start of 2025, it’s because they are.

Leadership at LaSalle Investment Management expressed these feelings of déjà vu at a Jan. 16 press conference, having previously forecasted a new dawn for commercial real estate investing at the start of 2025. But while some major themes have carried over, there are some distinct trends that set this year apart.

Breaking the cycle

Both lingering and acute economic and geopolitical uncertainty, a slowdown of new construction and rising vacancy rates are causes for concern, while strong capital raising numbers and steady appraisal metrics for most asset classes are reasons to be optimistic.

“It feels like Groundhog Day, where we’re stuck in this loop of optimism and disappointment,” said Brian Klinksiek, the firm’s global head of research & strategy, in reference to the 1993 comedy starring Bill Murray.

Movie references continued throughout the discussion, with Klinksiek referring to a dreaded stagflation scenario as a “phantom menace” that stalks the global economy, a nod to the first Star Wars prequel. While there’s no economic data to suggest that a recession-inflation combination is imminent or likely to occur, the uncertainty emanating from the Trump administration’s economic policies, particularly around trade, don’t exactly make a forecast easy.

READ ALSO: 3 Economic Trends to Watch in 2026

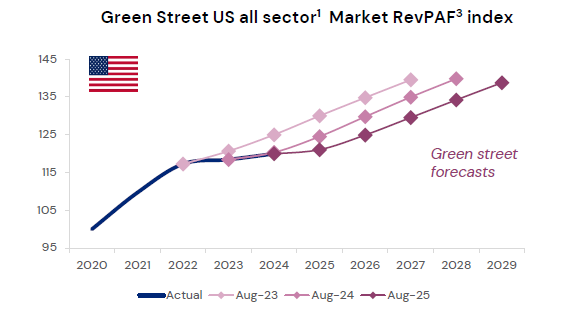

The most likely scenario for commercial real estate, according to Klinksiek, is a later and slower recovery for most asset classes. “Expectations of a steep recovery are likely to not be met,” Klinksiek predicted.

Consensus-driven data from Green Street forecasts a sector-wide average recovery to nearly $125 per square foot, a 4 percent increase from 2025. But any recovery is contingent on positive supply fundamentals, which can only be driven by rent increases. “This is the foundation for a recovery of new fundamentals,” Klinksiek said.

Red light, green light

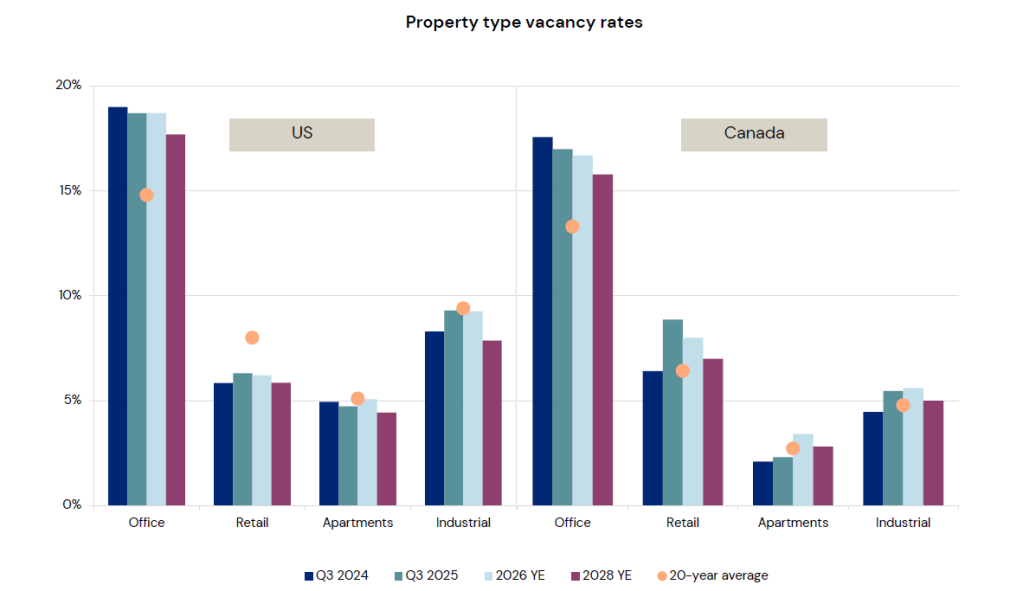

If and when a recovery does occur, not all sectors will fare equally. The firm sees industrial outdoor storage and affordable housing as investment priorities. “Just about every market needs affordable housing, and here is opportunity to grow rents modestly over time,” said Richard Kleinman, the firm’s chief investment officer for its Americas Region.

Logistics, self storage, medical offices, transitional lending and ground-up development occupy a sort of middle ground, having both attractive and selectively attractive value, driven mainly by vacancy rates. For the time being, LaSalle is skipping office, life science and data centers, seeing them as too volatile to allocate capital toward.

Downstream of demand is asset quality, which Tara McCann, head of Americas investor & consultant relations describes as being driven by a combination of positioning, managers and cash flows.

For its part, LaSalle is focusing on more income-driven assets, rather than those that will appreciate in value long term. “Hopefully, we’ll see a return everywhere, but that is contingent on capital,” McCann said.

You must be logged in to post a comment.