2025 Retail Net Lease Sales Volumes and Cap Rates

How the sector is faring, according to the most recent data.

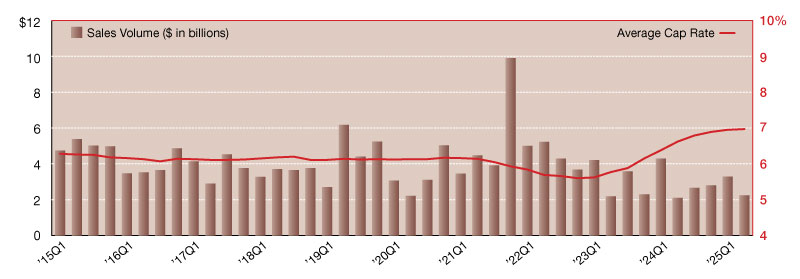

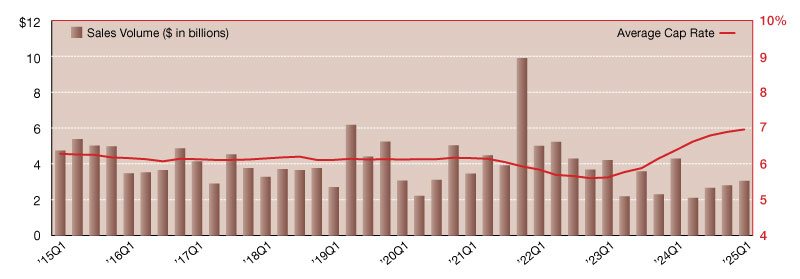

The single-tenant retail sector posted $2.2B in third-quarter sales volume, down 13.5 percent from the second quarter and nearly 17 percent year-over-year. Cap rates recorded slight upward pressure, rising 1 basis point to 6.93 percent, and by 13 basis points year-over-year.

The Southeast region dominated transaction activity in the third quarter, recording $653.7 million in volume and accounting for 29.7 percent of the total. The West followed with $430.9 million, representing 19.6 percent of overall volume. The Southwest ranked third with $373.3 million, or 16.9 percent, while the Northeast recorded $361.0 million, representing 16.4 percent. The Midwest contributed $261.3 million, or 11.9 percent of total volume, and the Mid-Atlantic region trailed with $123.2 million, accounting for 5.6 percent.

READ ALSO: Will Deregulation Turbocharge Tokenization?

By region, cap rates ranged from a low of 6.08 percent in the Northeast to a high of 7.60 percent in the Midwest. All regions, except the Northeast, recorded a modest increase over the prior quarter. Average cap rates are up 133 basis points from the recent low of 5.60 percent recorded in the fourth quarter of 2022.

Private buyers accounted for 68 percent of single-tenant retail acquisitions through the third quarter of 2025, followed by institutional investors at 8 percent. The private share rose sharply by 11 percent in 2024, while private investment activity increased by 2 percent over the same period. REIT/Listed acquisitions fell from 26 percent of investment activity in 2024 to 11 percent as of the third quarter of 2025.

—Posted on April 24, 2025

After three consecutive quarters of increasing activity, the single-tenant net lease retail sector posted a 31.7 percent quarter-over-quarter decline, reporting just $2.2 billion in second quarter investment sales.

Cap rates rose two basis points to 6.97 percent, up 35 basis points year-over-year. The increase reflects continued pricing recalibration, most notably for assets with shorter lease terms or non-credit tenants. However, cap rates for top-tier operators remain compressed in high-demand categories like quick service restaurants.

READ ALSO: Investment Matters: Flair for Open-Air Centers

Several retail segments stood out this quarter for their resilience and investor appeal. Fast casual, QSRs and drive-thru formats continue to attract capital, supported by strong brand performance and operational efficiency. Automotive service centers and aftermarket parts retailers also saw robust activity, with investors favoring long-term leases and regional or national operators. Convenience stores and gas stations, led by 7-Eleven-leased properties, traded frequently during the quarter, underscoring investor appetite for essential service retail.

Discount retailers and dollar stores remained a bright spot, despite recent headlines about store closures. Freestanding grocery stores—including Aldi and Dollar General Market—also traded at a high clip, benefiting from consistent foot traffic and demand from budget-conscious consumers. These concepts continue to attract investors seeking tenant durability and recession-resilient retail. While pricing remains bifurcated, the outlook for single-tenant retail is generally positive, with assets backed by essential service tenants, strong credit profiles and brands in expansion mode expected to remain in high demand.

—Posted on December 22, 2025

The single-tenant net lease retail sector demonstrated encouraging stability in early 2025, with sales volume climbing to $3.05 billion. Though volume was down year-over-year, healthy first-quarter performance marked a bright spot in an otherwise cautious capital markets environment. The modest quarter-over-quarter improvement reflects a continued appetite for well-located retail assets, especially those leased to creditworthy tenants and positioned in high-traffic areas.

READ ALSO: Why Convenience Stores Could Be the Smart Money Play of 2025

Cap rates in the segment averaged 6.96 percent in first quarter, up 7 basis points from fourth-quarter 2024 and 58 basis points year-over-year. Average rates have risen for nine consecutive quarters from a low of 5.60 percent reached at year-end 2022. Two years is a short period of time for investors to adjust to a 136-basis point swing. Investment strategies needed to be reassessed as asset values declined and fewer 1031 exchange buyers were active in the market.

Net lease retail sector in detail

The sector’s buyer profile during early 2025 revealed private investors dominating the landscape, making up 47 percent of acquisitions. Institutional buyers followed with 20 percent of the market, while international capital returned to the sector, jumping to 15 percent market share compared to just 1 percent for full-year 2024.

Retail’s quarterly gains were bolstered by persistent demand for necessity-based tenants and single-tenant quick service restaurants, which continue to exhibit strong operational resilience and robust growth. Evolving consumer preferences and economic uncertainties, however, may temper broader retail asset performance going forward.

Looking ahead, the market’s trajectory will depend on consumer spending trends, investor confidence and macroeconomic developments, such as the risk of a recession. While financing constraints and underwriting complexities present ongoing challenges, the sector’s reliance on stable and growth-minded tenants and continued interest from private investors may help sustain activity in the near term.

John Tagg is the Research Manager at Northmarq. He is responsible for coordinating the production and distribution of research reports that support the company’s commercial real estate brokerage and investment sales teams across local offices nationwide.

—Posted on August 29, 2025

You must be logged in to post a comment.