Will AI Disrupt Life Science Real Estate?

Lower demand could mean years of surplus space, a new study warns.

The fastest-growing “tech” in the biotech sector likely isn’t organic at all, but rather artificial intelligence, a new report from JLL cautions. And as this paradigm shift, already well underway, continues to take hold, it will have a profound effect on demand for life science real estate, according to the report.

JLL’s 2025 life science real estate perspective and cluster analysis highlights AI as one of three future-facing themes that are confronting the biotech sector, the other two being China’s rise in the life sciences and the return to supply-demand equilibrium—eventually.

Of those three factors, AI gets perhaps the most attention, driven in large measure by how deeply it’s starting to affect the life science real estate sector, in lasting ways.

“Nearly three years after the initial release of ChatGPT, and many more years since the first AI applications began cropping up in biotech research environments, we are beginning to see signs of its structural impact on real estate needs,” JLL stated. “By altering how science is conducted, and by whom, it will impact the size and shape of demand well after this market cycle.”

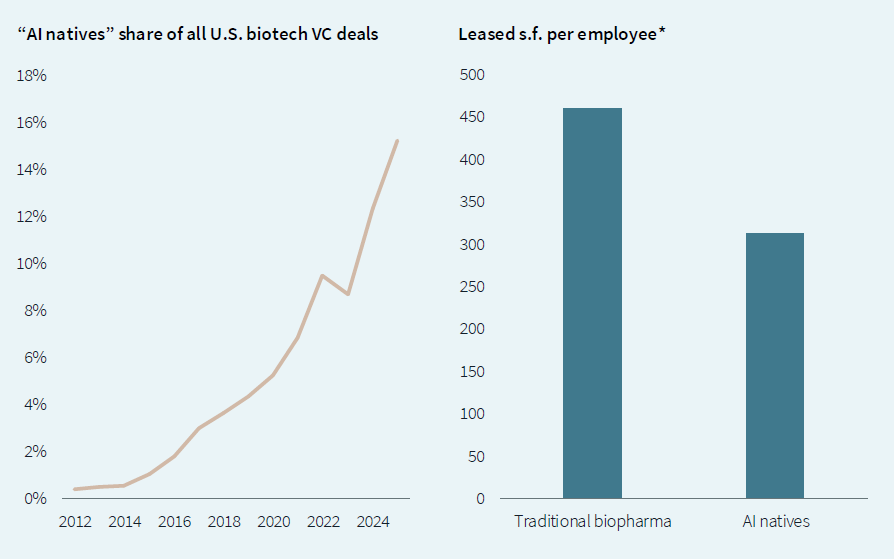

To understand why the report puts so much emphasis on AI, consider two specific sides of this: the massive growth of AI-native biotechs and how much space they’re leasing, versus traditional biopharma.

The report puts both into numbers: “AI-native biotechs are growing rapidly, accounting for one-sixth of all biotech VC deals year-to-date. The nature of the physical space they need is just beginning to show a departure from traditional biotechs,” the report noted. A JLL analysis also showed that on a per employee basis, “AI biotechs are leasing roughly one-third less space than a traditional-sector benchmark.”

That drastic drop in space per employee is colliding painfully against some other arresting figures. With biotech leasing slowing “to a glacial pace” earlier this year, JLL reported, the U.S. has 61 million square feet of lab space available for lease—triple the amount just four years ago. Over the same period, demand for lab space has decreased by more than half.

One small potential bright spot might be emerging, however. JLL noted that advanced R&D deals of more than 10,000 square feet with “tough tech/deep tech” companies outnumbered lab deals by 562 to 515 between the start of 2023 and mid-2025. But the report cautions that these occupiers are cost-conscious.

READ ALSO: Life Science Development’s Guarded Prognosis

Overall, JLL said, “The rise of new technologies will drive mass reconsideration of planning of legacy spaces, and automation of lab tasks could shift who does research and where.”

Another factor that might create turmoil in the traditional model of R&D real estate in coming years is the surge in China’s biomedical research, JLL reported. “Chinese biotechs now account for four times the in-licensing deals for U.S. biopharma in 2025 as they did in 2021. Judging by market share, U.S. biotechs have decreased as much as Chinese biotechs have increased in that time frame. Great research, low clinical costs and quicker trials have led biotech’s gaze toward mainland China.”

JLL explained that in-licensing of Chinese intellectual property leads to U.S. biotechs favoring higher proportions of office space, undercutting demand for lab/R&D space.

And as to supply-demand equilibrium in lab space, don’t hold your breath, JLL warned. That would require 30 million square feet being leased or leaving the market, such as by distress or adaptive reuse. Best (and unlikely) case is three years, and a likelier case would be almost seven years, according to the report.

The geography of biotech in 2025

Regarding that “where” issue, the JLL report takes a close look at the major U.S. life sciences clusters, ranking them into several lists based on varied criteria.

Under “Top talent hubs,” Boston ranks #1, given strong growth in life science sector employment, ample research focus and the most life sciences job openings.

“Top startup ecosystem” goes to the Bay Area, for what JLL describes as the highest venture capital deployment across AI/ML, health-care devices and core biopharma sectors, along with having the largest concentration of both established biopharma companies and emerging AI/life science startups.

The title of “Top medtech hub” too is awarded to the Bay Area, based on its leading expansion in the medical technology workforce, highest concentration of relevant clinical trials and dominant VC deployment in health-care devices and medical supplies.

“Top biomanufacturing hub” goes to New Jersey, for the largest concentration of biomanufacturing professionals and its high concentration of CDMO (contract development and manufacturing organization) facilities.

The top spot among “Top AI bio hubs” is the Bay Area, given its leading concentrations of AI/ML companies, AI-enabled life science startups and advanced AI professionals, along with the highest volume of pending AI/ML patents (2022–25) and the leading VC capital deployment in AI-life sciences convergence.

JLL’s 2025 top 10 U.S. life science hubs are Boston at #1, followed by (in order) the Bay Area; San Diego, Calif.; Raleigh-Durham, N.C.; Greater D.C./Baltimore; as well as New Jersey, Los Angeles, Philadelphia, Houston and Seattle.

You must be logged in to post a comment.