Why LIBOR to SOFR Transition Is a Test of Trust

Parkview Financial's Bruce Park on how the Secured Overnight Financing Rate should be a more foolproof pricing method.

In 2016, four former Barclays traders were convicted for rigging the London Interbank Offered Rate. Today, the LIBOR is nearing an end, and hopefully, there will be more accountability with the transition to Secured Overnight Financing Rate.

Originally scheduled for December 2021, the full transition from LIBOR to SOFR looks like it will now be completed in June 2023. In the commercial real estate finance world, lenders and borrowers alike now stand to bear the fiduciary responsibilities of this complex transition to a new index that will remove tampering capabilities, as it will be based on actual closings in the prior few days, and, therefore, force the rate to be based on real deals.

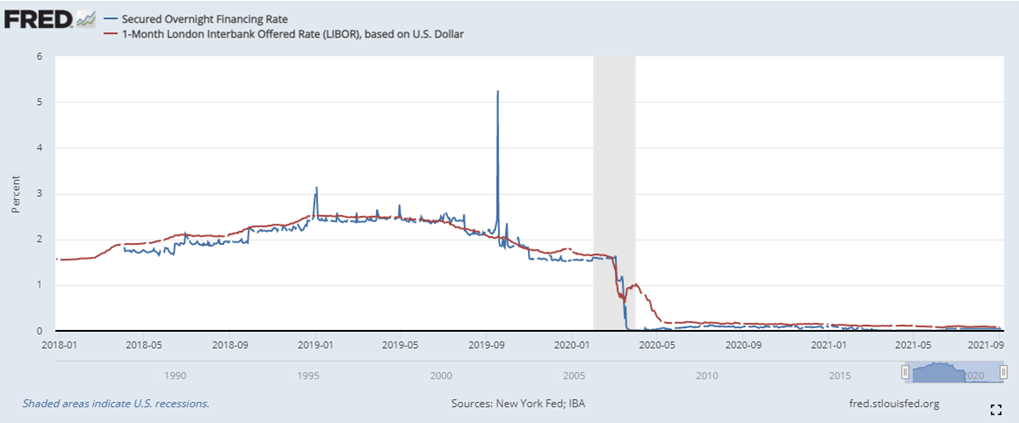

As seen in the graph below, the SOFR rate, which began publishing in April 2018, largely mirrors the one-month LIBOR rate. Since SOFR is calculated based on actual transactions in the U.S. Treasury repurchase market (therefore, meant to eliminate the inaccuracies caused by estimates of self-reported and sometimes manipulated lending rates from select banks), it is meant to provide a more accurate depiction of market conditions. On the flip side, however, since it is based on actual lending transactions, the graph below also shows that the SOFR rate is not as consistent as the LIBOR rate and does fluctuate dramatically when lending transactions tend to be higher, such as towards the end of the month, quarter and year.

Responsibility now falls on commercial real estate market participants to double-check past executed loan documentation as well as new ones, to ensure that fallback language does indeed account for this transition. More specifically, since lenders will have the power to dictate whether the adjusted terms will either remain at the latest recorded LIBOR rate or adopt SOFR or another alternative index, they are responsible for communicating with the borrowers clearly and ahead of time to ensure their borrowing costs are not unfavorably calculated.

On the other hand, since SOFR is usually a lower rate than LIBOR (aside from during high lending transaction periods), borrowers could leverage this knowledge to negotiate for past loan terms to reduce or even completely drop interest rate floors. Whatever the case may be, lenders and borrowers will have to work together honestly to ensure that the transition is fair for all parties involved.

For now, Parkview Financial has followed suit with other major financial institutions and adopted loan documentation to include fallback language that delineates “SOFR or the prevailing index rate at the time” as the benchmark rate to replace LIBOR. A few borrowers have indeed inquired about dropping interest rate floors on past loan agreements and we are working to find solutions that are reasonable and reduce risk exposure for both sides. Although this transition between old and new is unchartered and ambiguous, we look at the past and know for certain that the best practice is to keep borrowers updated and informed in order to ensure a smooth transition to the new SOFR process.

Bruce Park is an underwriting analyst for Parkview Financial.

You must be logged in to post a comment.