What Bid Intensity Says About US CRE

Closed transactions are a lagging indicator for accurate pricing.

In commercial real estate, transaction volume often grabs the headlines. But it is typically a lagging indicator. By the time deals close and are recorded, investors may have already adjusted their strategies and pricing expectations likely have changed.

Therefore, bid behavior offers a clearer and earlier read on where liquidity and confidence are rising across U.S. commercial real estate. JLL’s Global Bid Intensity Index aggregates thousands of bids across major markets to show how investors are behaving in real time—well before transaction counts fully reflect their decisions.

The Index rose to 98.5 in October 2025, signaling improving liquidity conditions and an increasingly competitive landscape, even as overall transaction volumes remain below previous peak levels.

For private investors—especially those targeting transactions under $25 million—these signals matter. Bidding activity is not only recovering faster in this segment. It is also showing where confidence is strongest, where risk is being priced precisely and where execution has become a key differentiator.

LIKE THIS CONTENT? Subscribe to the CPE Capital Markets Newsletter

Bid intensity reveals confidence, not speculation

What differentiates today’s market is not just rising activity, but how clearly bid behavior is separating confidence from uncertainty. The heaviest bidding is concentrating around assets with multiple acceptable outcomes, while properties dependent on a single execution path are seeing wider spreads in pricing and participation.

The contrast is easiest to see through underwriting outcomes. A steady income–producing multifamily asset that is 95 percent leased, with staggered expirations and modest mark-to-market potential, offers several viable paths forward. Rents can grow or flatten, and the income still supports value. These assets attract higher bid counts and tighter pricing because buyers broadly agree on risk and durability.

By comparison, assets with binary outcomes draw a very different response. A shopping center that is 95 percent leased, but has 50 percent of its net operating income rolling within the next 12 to 18 months, may hinge on a single tenant decision. If that tenant renews, value stabilizes. If it vacates, income falls and capital requirements rise. That uncertainty results in fewer bidders and wider pricing dispersion. The same pattern applies to capital-intensive office-to-residential conversions.

Across sectors, bid intensity reflects this distinction. Living and multi-housing shows the strongest bidding dynamics, supported by housing shortages in many U.S. markets and deep pools of private capital seeking predictable cash flow. Industrial and logistics bidding has become more competitive as trade policy uncertainty eased. Office bidding has improved from late-2023 lows, but remains highly selective.

The takeaway is straightforward. Tighter bid fields signal confidence in outcomes. Wider dispersion reflects execution risk. Bid data makes that difference visible well before it appears in closed-sale statistics.

Why sub-$25M deals remain the most competitive

Private capital continues to lead the market’s recovery, particularly in transactions below $25 million. These deals attract broader buyer pools than larger institutional trades, resulting in higher bid counts and more competitive pricing.

Private investors tend to be more flexible in how they deploy capital and structure deals. Financing availability also remains more robust at the lower end of the market, where lenders are more comfortable spreading risk across a larger number of smaller loans.

The result is tighter pricing bands and greater liquidity in sub-$25 million deals relative to larger assets, where underwriting remains more conservative. In many cases, private capital is moving first, establishing price discovery that institutional capital may follow later.

For sellers, this depth of demand is shifting priorities. The highest headline price is not always the winning bid. Certainty of execution—including clean contracts, limited contingencies and flexible closing timelines—has become a critical differentiator.

How bid signals lead transaction volumes

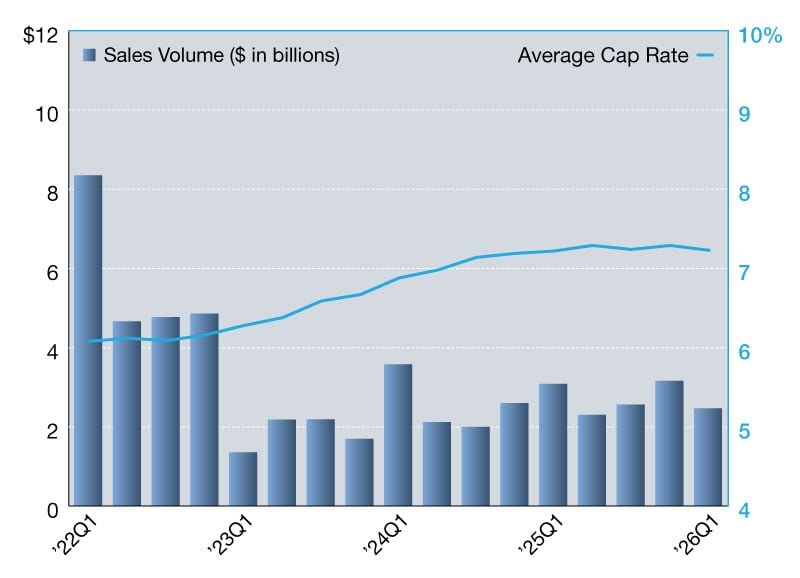

Bid behavior typically improves well before transaction volume recovers, often by 90 to 150 days. Liquidity begins to form as buyer and seller expectations move closer together—well before that alignment is reflected in closed deals.

Rising bid counts, narrowing bid-to-ask spreads and tighter pricing dispersion indicate that investor confidence is returning, even as some negotiations remain anchored to prior-cycle pricing.

For disciplined investors, this timing advantage matters. Rather than waiting for transaction volume to confirm a market turn, bid data allows investors to gauge momentum earlier and price risk more precisely.

What bid trends suggest

Bid behavior is telling a clear story in U.S. commercial real estate. Confidence is returning first to assets with durable income and predictable cash flows. Private capital, particularly in sub-$25M transactions, is leading that shift.

The Global Bid Intensity Index reinforces a simple insight: Investor conviction forms before closed volumes rise. Investors who focus on bid signals are better positioned to act early, price risk accurately and compete effectively as the investment cycle continues to reset.

In today’s market, disciplined underwriting and execution certainty remain essential. Understanding how capital is bidding provides the forward-looking perspective investors need to move with confidence rather than react after the fact. That perspective is increasingly valuable as markets normalize unevenly and investors seek clarity amid shifting conditions today.

David Gaines is managing director & private capital group leader at JLL Capital Markets.

You must be logged in to post a comment.