The Benefits of Interest Rate Caps at a Time Like This

In a rising rate environment, IRCs provide stability to owners and borrowers, says Vishal Hotchandani of Parkview Financial.

Vishal Hotchandani

Over the past year developers have dealt with a rise in construction costs due to inflation, global supply chain disruptions, construction demand, and higher labor costs.

CBRE’s Construction Cost Index forecasts a 14.1 percent year-over-year increase by the end of 2022. Though the Fed’s policies of raising the Fed funds rate and quantitative tightening to wring inflation from the U.S. economy should eventually provide builders some relief, in the short-term it will negatively affect their profitability by increasing financing costs. It’s no wonder that in recent months borrowers who plan to start construction projects have been asking their debt capital sources for fixed-rate loans.

Nearly all private lenders use leverage themselves—in the extreme case, to engineer higher returns to investors and, in the modest case, to manage fund cash flows. Giving a borrower a fixed-rate loan during a time when the lender’s own borrowing cost will increase would negatively impact the lender’s return to its investors. As responsible fiduciaries, fund managers are unlikely to grant fixed-rate loan requests. Thus, those who assume floating-rate loans but seek stability with respect to interest payments should look to the derivatives markets and consider purchasing an interest rate cap (IRC).

In short, an IRC is an insurance policy. In exchange for a single premium payment, the IRC provider promises to pay the additional interest cost when the index, over which the floating-rate loan is based, increases. The key terms to know when dealing with IRCs are notional, term, and strike rate and the cost can be estimated by an online calculator.

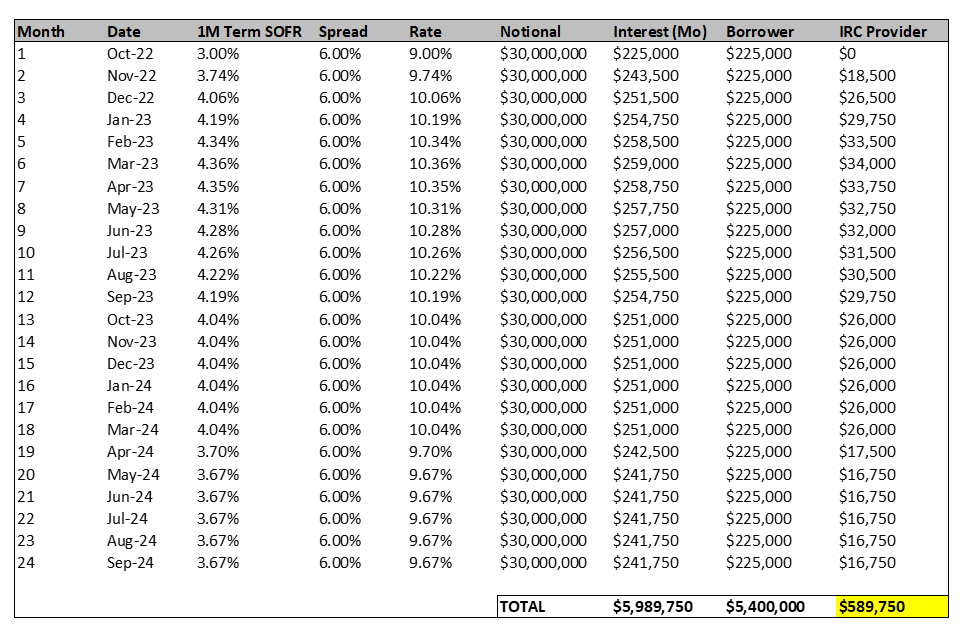

For clarity, consider interest-only financing on the entire loan amount of $30 million (notional) that is due after two years (term) and is offered at a rate of 1M-Term SOFR (1MTS) + 6 percent (spread). Assume also that the IRC strike and 1MTS are both 3 percent at the time of closing. The cost of such an IRC today would be $821,000 (2.74 percent of the notional)3. The table below delineates the projected monthly interest payments to the lender based on the 1MTS forward curve4 and is broken out by amount paid by the borrower and the IRC provider.

In the example below, the borrower will have spent $821K for approximately $590,000 in coverage. That may not seem like a good deal, but different individuals value peace of mind afforded by insurance differently. Additionally, the 1MTS forward curve is not static. Today, it suggests that 1MTS will peak at 4.36 percent in March 2023 but only one month ago it showed the peak to be 3.73 percent in May 2023. As the Fed continues to share its strategy with the market, the curve will surely change. Whether it will change enough, such that the coverage will be greater than the cost, is anyone’s guess. Ultimately, the decision to buy an IRC should be driven by a borrower’s tolerance for interest rate risk.

Vishal Hotchandan is senior loan originator, Parkview Financial.

1 “2022 US Construction Cost Trends”; CBRE; https://www.cbre.com/insights/books/2022-us-construction-cost-trends

2 “What is an Interest Rate Cap?”; Derivative Logic; https://derivativelogic.com/interest-rate-caps

3 “Interest Rate Cap Calculator”; Chatham Financial; https://www.chathamfinancial.com/technology/interest-rate-cap-calculator

4 “Forward Curve”; Pensford; https://www.pensford.com/resources/forward-curve

Notes: (1) Most floating rate, interest-only construction lenders only charge interest on dollars drawn, meaning the overall interest cost of the example loan would be much less. Pricing an IRC for that type of product would also be less but not possible with any of the available online calculators; (2) the IRC provider total is independent of the spread and 6 percent was used for illustrative purposes.

You must be logged in to post a comment.