On the News: Why Mezzanine Capital Is Growing Scarce

Private lenders are not finding this vehicle as appealing as they once did.

Therese Fitzgerald

If ever there was a need for mezzanine lenders, it’s now. But it’s harder to find one as private lenders grow more cautious, according to a panel of investors at last week’s NYU Schack Capital Markets Conference in New York City.

“The senior needs to come back, to feel comfortable, for the mezzanine to come back,” said Tim Johnson, Global head of BREDS, Blackstone.

Mezzanine financing grew in importance post-GFC after banks tightened their underwriting on larger lenders, leaving borrowers with gaps in their capital stacks to fill. Just how much mezzanine lending was done during the upcycle is hard to gauge since mezzanine loans do not appear in public records, but mezzanine lending helped boost the large number of loans originated during the pre-2022 low-rate period.

And these lenders came out in force last year, raising heaps of capital to stem the shortfalls owners would have when they try to recapitalize or refinance now that rates are higher and fundamentals are weaker, particularly for office space. And, since mezzanine capital is more expensive than senior debt and promises a higher return for investors, the opportunities seemed endless.

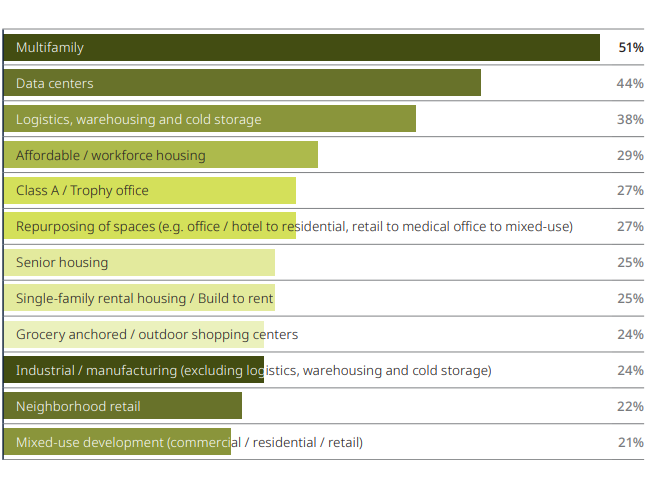

“Only 25 percent of the current market you could refinance as-is,” said Miriam Wheeler, partner, managing director & head of the Global Real Estate Financing Group at Goldman Sachs & Co.

But, lately, there’s been pullback by mezzanine lenders and some consolidation among them as property income and valuations have further eroded and, as Johnson mentioned, senior lenders have grown more skittish following this year’s regional bank collapses and as more loans under-perform. “A lot of the banks are just frozen,” said Andrea Balkan, managing partner and head of Real Estate funds, Brookfield Asset Management.

Trouble in the capital stack

But it’s not just senior lenders who are dealing with defaults. Last month, the Wall Street Journal reported that 62 foreclosure notices were issued by mezzanine and other high risk lenders through October. It was the most in 15 years. That is sure to erode confidence even further among the mezzanine crowd.

Brookfield, Balkan said, is still committed to its core mezzanine lending business but, as overall liquidity has decreased, it has broadened its lens to include rescue capital, recapitalizations, construction lending and CMBS. Today, Balkan’s group may originate a whole loan and then originate a mezzanine loan. Regardless of the opportunity, however, quality is paramount.

“I think mezzanine lenders are ready to step up for an appropriate return on new buildings,” she said, noting the increasing gulf between A/B office buildings. “We’re not going to throw good money after bad,” she added.

Speaking of office, that’s where liquidity is most constrained. The property type is experiencing the same re-ordering that occurred in retail, observed Jesse Hom, managing director & global head of Real Estate Credit and Capital Markets, GIC.

“There is a very clear stratification of asset quality (in retail), and capital support will depend on where you fall,” said Hom. “We see office falling into those tiers and a similar shakeout.”

You must be logged in to post a comment.