New-Issue CMBS Spreads to Swaps

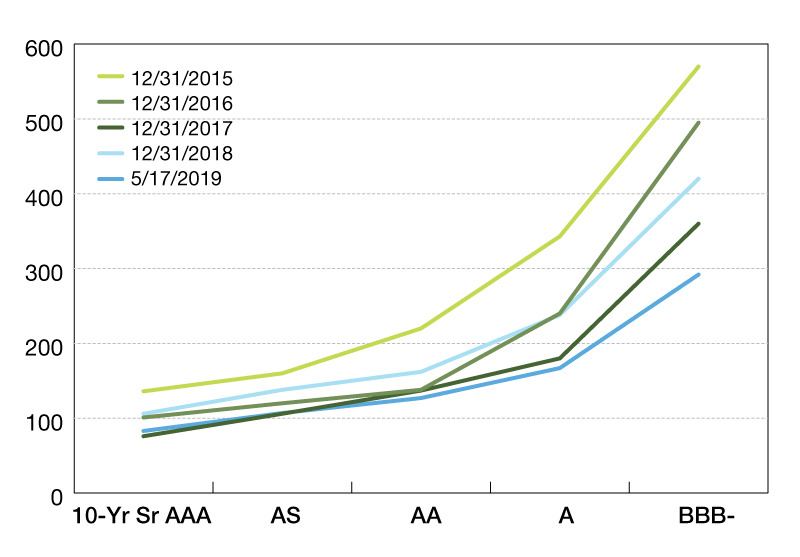

In addition to the credit curve coming down, it has also flattened, with the spread between single‐A and triple‐A CMBS bonds tightening from 207 bps at the end of 2015 to 84 basis points at the end of 2019.

basis points

Source: Mortgage Bankers Association

In a search for yield and a vote of confidence in the assets, investors have pulled commercial mortgage‐ backed securities (CMBS) credit spreads lower in recent years. In CMBS, cash flows from mortgages are pooled and then paid out through a waterfall—with payments going to higher‐rated bonds first and lower rated bonds last. Lower‐rated tranches are the first—and usually only—bonds to experience any losses. In the chart above, the spreads between swap rates and CMBS yields for safer, higher‐rated bonds are on the left, and spreads for more risky, lower‐rated CMBS bonds are on the right.

In recent years, investors have reduced the spreads they demanded to invest in CMBS bonds across this credit curve—with the spread for 10‐year senior AAA bonds falling from 136 basis points (bps) at the end of 2015, to 101 bps at the end of 2016, and 76 bps at the end of 2017. Spreads rose to 106 bps at the end of last year—primarily due to year‐end market volatility—but have since settled back to 83 bps as of last week. In addition to the credit curve coming down, it has also flattened, with the spread between single‐A and triple‐A CMBS bonds tightening from 207 bps at the end of 2015 to 84 basis points at the end of 2019.

Jamie Woodwell is the Mortgage Bankers Association’s vice president of commercial real estate research.

You must be logged in to post a comment.