How the Middle East Conflict Is Impacting CRE Investment

Investor sentiment remains positive despite broader geopolitical uncertainty, according to a Marcus & Millichap webinar panel.

Commercial real estate has historically operated through alternating cycles, experiencing both periods of growth and decline over time. However, Marcus & Millichap’s CEO Hessam Nadji describes this cycle as a “rolling disruption” that has persisted since March 2022, driven by rising interest rates, tariffs and other factors playing into broader uncertainty.

The most recent disruption to the cycle is the ongoing Iran conflict, which has contributed to higher oil prices and other geopolitical risks. While the overall outlook on the conflict is unclear, with hopes of a near-term solution, ongoing investment activity in 2026 is helping sustain the commercial real estate market.

Nadji was joined by Moody’s Chief Economist, Mark Zandi, Marcus & Millichap’s Senior Vice President & Chief Intelligence & Analytics Officer John Chang and Sr. Fellow Global Risks at Center for National Interest John Sitilides for the firm’s Middle East Conflict – Implications for U.S. Economy and CRE webcast. The panel emphasized that, despite heightened uncertainty, investor sentiment in the commercial real estate sector remains generally positive, supported by a U.S. economy that is fragile but still holding up.

“When we look forward, 2026 is going to be a year where we look back and say ‘that was a great time to invest,’” Chang said in the webcast. Despite long-term optimism, short-term caution remains.

Short-term economic pressure

Zandi outlined the economic implications of the Middle East conflict and its ripple effects across the global economy. “The economy is growing, but it’s a fragile growth,” he said, noting the growth rate is around 2 to 2.5 percent, below the potential growth for the U.S.

When it comes to the idea of a recession, Zandi is not fully predicting one in the U.S., but there is an elevated risk depending on how long the war continues. At the time of the webcast, he put the probability at about 40 percent, below the 50 percent threshold that typically signals a base-case recession scenario as seen previously, such as the 2008 Great Financial Crisis.

READ ALSO: Should CRE Worry About Private Credit?

Zandi also pointed to oil prices as a key risk indicator, noting that a sustained rise to around $125 per barrel could push not only the U.S., but the global economy into a recession if the conflict continues. At the same time, he highlighted artificial intelligence and technology investment as a key tailwind supporting economic activity.

A key component of that trend comes from the U.S. being the leader in data center development, Zandi said. He believes that this tailwind from AI will keep the economy steady while the short term remains unclear.

“The headwinds from the Iran war, tariffs and broader economic policy will likely bump up against the tailwinds of AI and come to a draw, leaving the Fed essentially on hold,” Zandi said.

Investor activity continues despite uncertainty

Even with the macroeconomic uncertainty outlined by Zandi, Chang said investor sentiment across commercial real estate remains positive. He noted that many investors view the current volatility as short-term and continue to move forward with acquisitions and dispositions, while maintaining a more cautious approach.

There is also capital that needs to be deployed and commercial real estate is emerging as an attractive investment option. “Real estate as a hard asset with inflation resistance becomes a more and more appealing option for investors,” Chang said.

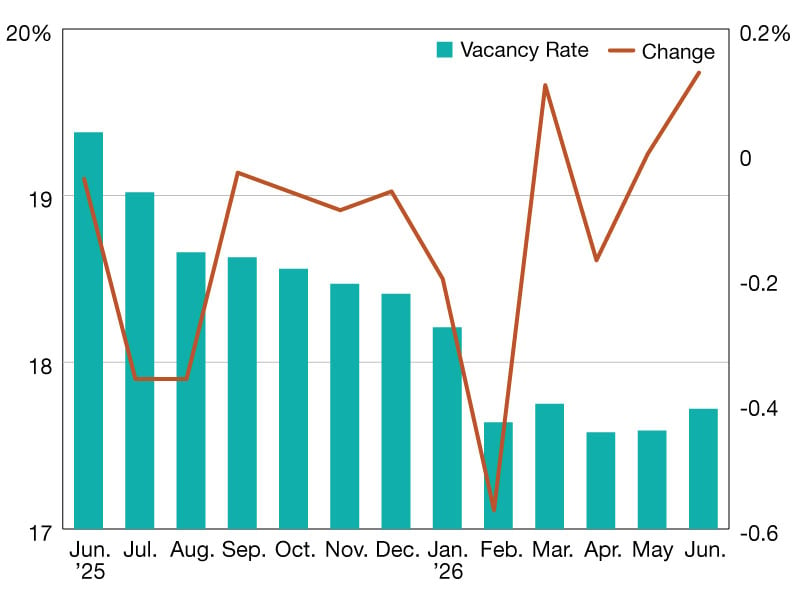

He added that fundamentals across sectors remain relatively stable, particularly vacancy rates, though industrial continues to see higher vacancy due to overbuilding. That activity is continuing despite uncertainty.

“We’re still seeing a lot of investors continuing to drive forward with their purchases and their dispositions,” he said.

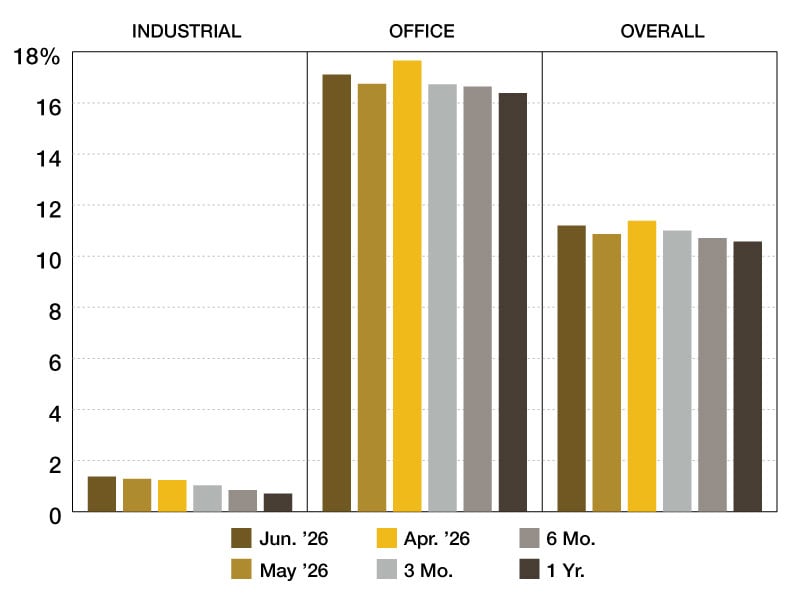

Transaction activity is improving, with volume up 18 percent year-over-year, according to Chang, as capital continues to move into commercial real estate. He noted that cap rates have adjusted over the past several years, rising and now beginning to level off. Class A assets are seeing lower cap rates due to strong demand, while Class B and C properties continue to face higher rates and more pricing pressure.

“I think when we look forward over five to seven years, the assets will continue to outperform,” Chang said.

You must be logged in to post a comment.