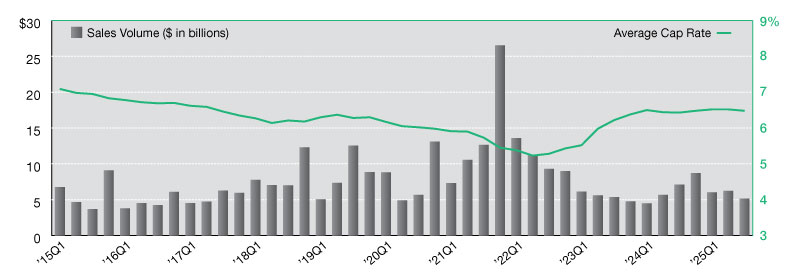

2025 Industrial Net Lease Sales Volume and Cap Rates

Despite the transaction slowdown, industrial remains the most active single-tenant real estate sector.

Industrial remains the most active single-tenant sector, with nearly $5.2 billion in third quarter investment sales. However, volume declined 17.3 percent from the second quarter and 26.3 percent year-over-year. Cap rates compressed slightly by 4 basis points from the second quarter but increased by 9 basis points year-over-year.

READ ALSO: 2026 Special Servicing Rates

The Southwest region led transaction activity in the third quarter, recording $1.3B in volume and accounting for 26.0 percent of the total. The Southeast followed with $1.2B, representing 23.3 percent of overall volume. The Midwest ranked third with $1.0B, or 20.3 percent, while the West recorded $0.9B, representing 17.5 percent. The Northeast contributed $0.4B, or 8.4 percent of total volume, and the Mid-Atlantic region trailed with $0.2B, accounting for 4.5 percent.

Industrial cap rates by region and buyer group

By region, cap rates ranged from a low of 5.64 percent in the West to a high of 7.43 percent in the Midwest. All regions, except the Midwest, recorded a modest decline over the prior quarter. Average cap rates are up 127 basis points from the recent low of 5.21 percent recorded in the second quarter of 2022.

Private buyers accounted for 48 percent of single-tenant industrial acquisitions through the third quarter of 2025, followed by institutional investors at 23 percent. The private share rose by 6 percent from 2024, while institutional investment activity increased by 1 percent over the same period. REIT/Listed acquisitions fell from 11 percent of investment activity in 2024 to 8 percent as of the third quarter of 2025. The share of cross-border investment activity fell to 11 percent of deal volume, down from 20 percent in 2024.

—Posted on March 26, 2026

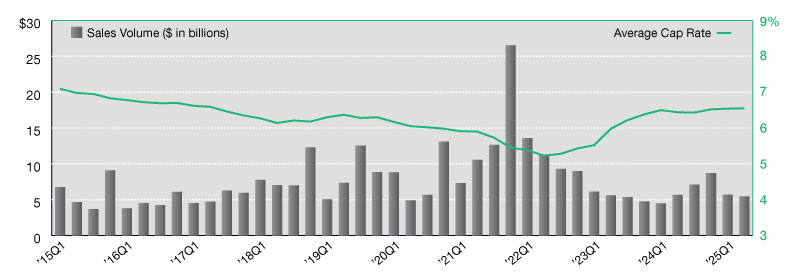

Industrial remains the most active single-tenant sector, with more than $5.4 billion in second-quarter investment sales. However, volume declined 4.4 percent from the first quarter and 6.6 percent year-over-year, reflecting a more cautious investment environment. Despite the slowdown in sales, investor interest in the industrial market remains strong, particularly for mission-critical facilities and assets with established tenants and long-term leases.

READ ALSO: Is Industrial CRE Benefiting From Tariffs and Reshoring?

During second quarter, cap rates rose by a single basis point to 6.55 percent, and the average is now up 11 basis points year-over-year. The modest increase suggests pricing is stabilizing, supported by strong long-term fundamentals and continued tenant demand.

Industrial development trends shift

Development trends are shifting across the industrial sector. New warehouse construction is increasingly concentrated in build-to-suit projects, with EV and battery manufacturing plants at the forefront. These facilities often command premium pricing due to their specialized infrastructure and long-term leases. Cold storage development is also expanding, though rising construction costs and site constraints are slowing delivery timelines and influencing investor expectations.

Industrial outdoor storage continues to gain traction as a niche growth area. Investors are targeting low-coverage sites near ports and major logistics corridors, drawn by their low capex requirements and strategic utility. Competition for IOS properties is intensifying though, which is beginning to impact pricing.

Looking ahead, investors are expected to remain selective, favoring assets with strong tenant credit, long lease terms and strategic locations tied to logistics, manufacturing or food distribution. While the pace of sales has moderated, the sector’s long-term outlook remains positive.

John Tagg is the Research Manager at Northmarq. He is responsible for coordinating the production and distribution of research reports that support the company’s commercial real estate brokerage and investment sales teams across local offices nationwide.

—Posted on October 28, 2025

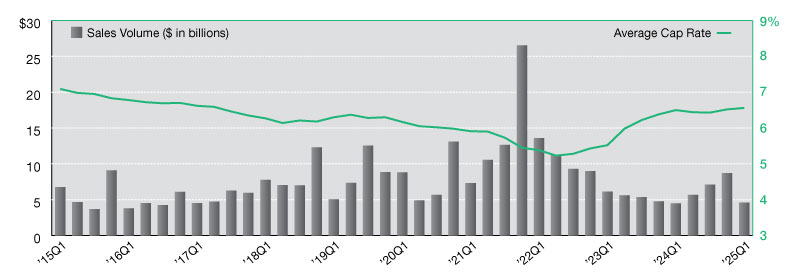

The single-tenant industrial sector experienced mixed dynamics in early 2025. While the market’s resilience amid broader market pressures is illustrated in first-quarter results, it’s clear that the industrial market is not immune. Total sales volume reached $4.6 billion, reflecting a slightly stronger start to the year compared to 2024. However, the market had been gaining momentum as last year came to a close, so the first quarter’s comparatively lackluster performance was disappointing. Despite the quarter’s reduced activity levels, investors continue pursuing industrial assets, and volume is expected to increase in future quarters.

After some fluctuation during mid-2024, industrial cap rates continued their gradual ascent, ending the first quarter of 2025 at an average of 6.56 percent. This marks a 4-basis-point increase from the previous quarter, but only a 6-basis-point rise from the first quarter of 2024. While cap rates remain well below the broader single-tenant net lease market average, elevated borrowing costs and shifting market risks have been driving an upward trend.

READ ALSO: NAIOP Special Report: Will Tariffs Tax CRE’s Industrial Sector?

Private buyers remained the most active participants in the industrial sector, accounting for over half of first quarter 2025’s acquisitions. Institutional investors followed with a market share of 26 percent, continuing to pursue opportunities in prime logistics facilities near key distribution hubs. The sector’s appeal stems from its critical role in supporting e-commerce growth, third-party logistics and inventory management strategies. REITs, however, retreated further from the segment, only representing 4 percent of the buyer pool to start the year.

Despite the quarterly decline in sales, the net lease industrial sector continues to benefit from strong fundamentals and favorable long-term prospects. New supply is limited and vacancy rates remain low in many industrial corridors, supporting rent growth and asset performance.

Looking forward, the market’s performance will hinge on macroeconomic developments and investor confidence in the broader commercial real estate landscape. While short-term challenges persist, the sector’s long-term fundamentals remain one of the strongest within the single-tenant net lease universe.

—Posted on June 30, 2025

Lanie Beck is the Senior Director of Content & Marketing Research at Northmarq. She is responsible for leading the content strategy for the firm and producing research reports in support of the organization’s commercial investment sales division.

You must be logged in to post a comment.