Rising Demand Accelerates Coworking Growth

A variety of factors are behind the expanding flex-office footprint, the latest CommercialEdge report shows.

The shift to hybrid work, coupled with tenants’ flight-to-quality trend and the increasing popularity of short-term leases created an uptick in demand for flexible office space, according to the latest monthly national office market report by CommercialEdge. This has prompted a wide array of commercial real estate players to play their part in the game; Major brokerage firms including CBRE, Cushman & Wakefield and JLL are seizing the opportunity to increase their investment in coworking, while well-versed players such as Spaces, Regus or Industrious are also expanding their footprint.

The shift to hybrid work, coupled with tenants’ flight-to-quality trend and the increasing popularity of short-term leases created an uptick in demand for flexible office space, according to the latest monthly national office market report by CommercialEdge. This has prompted a wide array of commercial real estate players to play their part in the game; Major brokerage firms including CBRE, Cushman & Wakefield and JLL are seizing the opportunity to increase their investment in coworking, while well-versed players such as Spaces, Regus or Industrious are also expanding their footprint.

At the same time, office space owners went autonomous and started to operate their own flexible spaces—through programs such as Boston Properties’ FLEX by BXP or Irvine Co.’s Flex Workspace+—in an effort to improve occupancy rates and cash flow.

READ ALSO: WeWork, Yardi Launch Flex Office Platform

The activity within the office-using sector showed signs of moderation, adding 51,000 new jobs in September. After falling behind Information and Professional and Business services every month since April 2021, the Financial Activities sector was the only segment to record negative growth, losing 8,000 jobs. Of the top 25 markets covered by CommercialEdge, seven of these shed financial activities jobs year-over-year in August, pointing towards further uncertainty in the office sector.

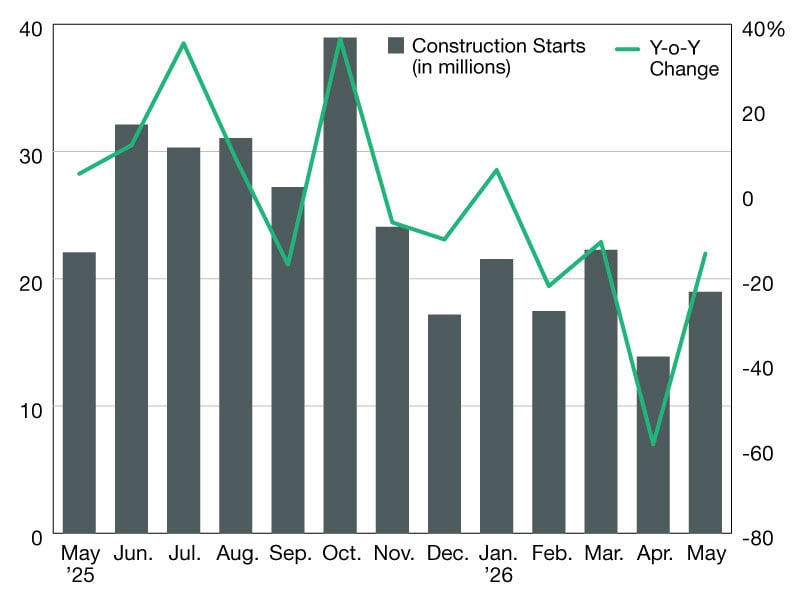

The under-construction pipeline continued to shrink, encapsulating some 139.1 million square feet of office space across the nation at the end of September, accounting for 2.1 percent of total stock, according to the CommercialEdge office report. Year-to-date construction starts amounted to 46.6 million square feet as of September, with the largest declines recorded in gateway markets. While the new supply pipeline will not produce starts at pre-pandemic levels, 2022 will likely match 2021’s 62.2 million square feet in new office groundbreakings.

Vacancy rate holds steady

National average full-service equivalent listing rates averaged $37.67 per square foot at the end of September, decreasing by 240 basis points year-over-year. Meanwhile, the national office vacancy rate stood at 16.6 percent in September, up 180 basis points from the same time last year.

While vacancies spiked in most markets throughout the last year, markets benefitting from relocations of firms and workers-such as Miami (140 basis-point decrease year-over-year) and Charlotte (120 basis points)-outperformed most markets surveyed by CommercialEdge.

encompassing a high concentration of employees in the finance sector—full-service rates recorded a 16.8 percent year-over-year jump. Asking rates had double-digit increases in life science hubs such as Boston (15.2 percent) and San Diego (13.9 percent).

Read the full CommercialEdge office report.

You must be logged in to post a comment.