Maturing Medical Office Market Turns Institutional

JLL's Mindy Berman on the solid fundamentals these properties can offer investors.

Investors are increasingly viewing outpatient medical properties as more than just an alternative to core real estate sectors. Any investor looking to enter a new market can benefit from observing how the medical office market played out during a pandemic. MOB occupancy, rental rates and rent collections remained stable and steady.

Tenant are financially robust, typically speaking, with many investment grade-rated health systems and major multi-specialty and high-value specialty physician practices.

Despite COVID-19 threats, health care providers emphasized and doubled down on outpatient locations to deliver care during the pandemic to offer safe environments and adapted the real estate environment to overcome operational challenges.

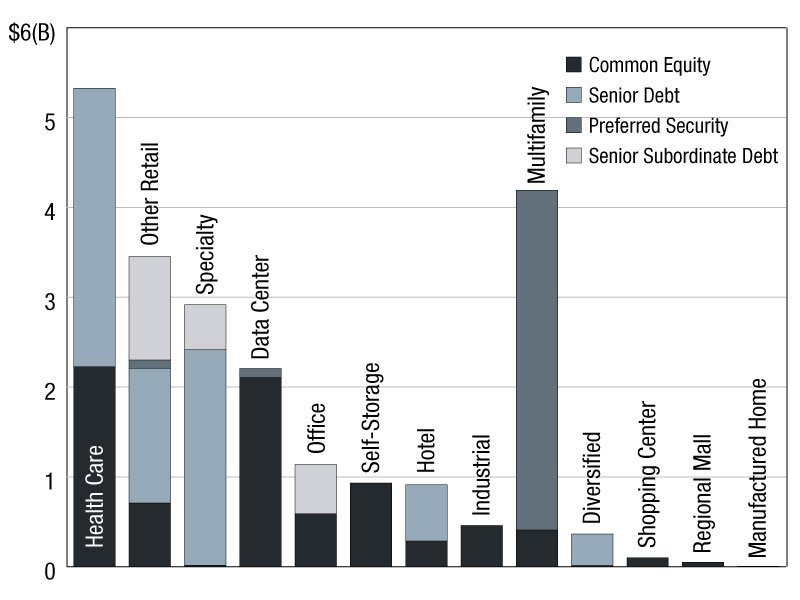

The U.S. MOB market, consisting of 1.5 billion square feet in 36,500 properties, is valued at $460 billion. Unlike other commercial property classes, 63 percent are owned by health care providers, suggesting just how much potential annual liquidity could arise as health systems and providers monetize assets or develop new locations, and new investors come into the mix.

Transaction volume in MOBs increased significantly between 2018 and 2020 vs. 2012 to 2014, with an increase of 71 percent, totaling a whopping $34.7 billion, which makes MOB among the largest alternatives asset class.

Investment management and private equity’s share of acquisitions in the MOB market grew by 30 percent between 2015 and 2020, and private equity and investment managers’ share of the MOB marketplace is set to increase further. As a first-generation business, medical office investment was dominated first by enterprising developers and specialist health-care REITs. As medical office became better understood, select investment managers and private equity joined the party. Now, as medical office becomes more institutional with a proliferation of experienced operators, the sector is attracting direct and indirect investment by a broad swath of private capital, domestic and foreign pension funds, sovereign wealth funds and the like. All of which leads to a more liquid asset class suited to participation by institutional investors.

An indication as to how the MOB sector stands to evolve can be seen by looking at the transformation of the multi-housing sector, which experienced a similar process of institutionalization in the 1990s and early 2000s. This evolution catalyzed the strong performance of the sector over the succeeding 20 years to today’s exceptional explosion of investments and investor returns. From 2000 to 2005, annual transactions volume of U.S. multi-housing units averaged 3.6 percent of inventory, increasing to 6.3 percent from 2010-2020. The medical office sector is positioned to undergo a similar transformation, with average turnover between 2010 and 2020 averaging 1.5 percent and expected to trend upwards from here, aided by greater investor share of ownership of existing inventory over time.

Institutions Take Notice

Institutional investors are increasingly drawn to the defensive nature of MOB based on the current asset performance. These characteristics include the aforementioned investable scale; the secular demand tailwinds benefiting the sector as a whole; the sector’s geographic diversification given that MOB assets are highly distributed around the country, in primary, secondary and tertiary markets; the overall level of market transparency in terms of asset and portfolio performance; and lastly, the deep bench of best-in-class operators in the space.

MOBs can provide investors with the following characteristics: A durable income stream, working in tandem with strong credit tenants, an attractive long-term investment proposition across all geographies, and a broad scope of opportunity to scale up, suited to investors with an appetite for growth

Some of the forces the forces representing secular demand tailwinds within health care and MOBs include:

- The utilization of healthcare services is set to increase dramatically between now and 2060.

- The aging population (65 years and older) consumes 80 percent of healthcare expenditures and is nearly doubling in size through 2050.

- GDP and annual health-care expenditure are set to increase in tandem. National health expenditure is forecast to increase from 18.5 percent ($2.5 trillion) in 2021 to 19.9 percent ($5.8 trillion) in 2027.

- There is a shift towards outpatient healthcare, rising from 1,825 visits per 1,000 population in 1999 to 2,400 per 1,000 population in 2018, and continuing to grow due to technological development, patient preferences and safety issues

- Occupancy rates have been consistently stable at 92 percent throughout the period between 2011-2021, with constrained construction pipeline and virtually no speculative development.

The growing demand for health care services is as certain as the rainfall in Seattle. Innovation is driving availability of procedures in outpatient settings, supported by payors and reimbursement pressures. Surgical operations are becoming less invasive and efficient, with contemporary anesthesia procedures introducing less risk. A continued shift towards outpatient services will drive provider demand and consumer preference for more outpatient facilities.

You must be logged in to post a comment.