Bankruptcy Court and Distressed CRE Opportunity

Adam H. Friedman of Olshan Frome Wolosky LLP on the rules, pitfalls and benefits of the Chapter 11 process.

Adam H. Friedman

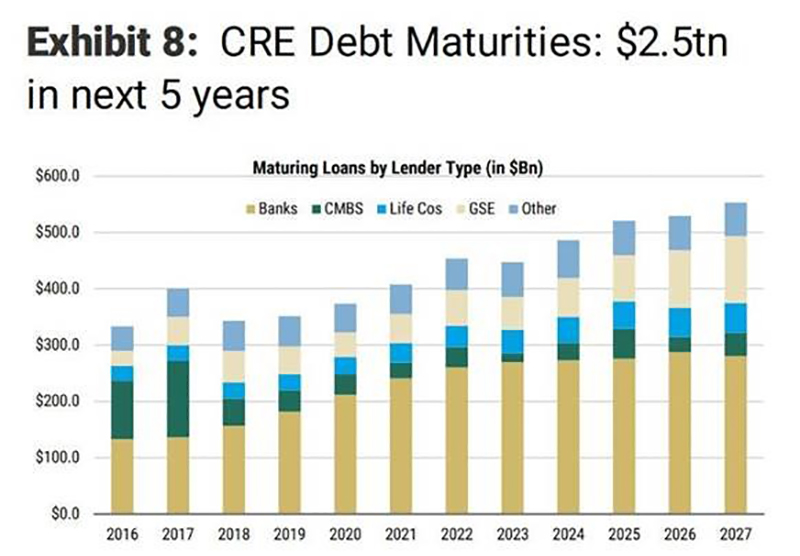

The commercial real estate industry faces unique challenges: rising interest rates, inflation and similar macroeconomic stresses not experienced for over a decade, combined with the never-before-seen structural impacts of the post-COVID “work-from-home” dynamics. These factors, coupled with a wave of CRE loan maturities estimated at $2.5 trillion over the next five years, lead many to speculate that there will be unique opportunities for investors and lenders looking to capitalize on distressed real estate situations.

To be sure, the steady wave of CRE loan maturities will be accompanied by a steady wave of restructuring and distressed investing and lending opportunities. In this environment, it is safe to assume Chapter 11 bankruptcies will be required to restructure distressed real estate projects, and distressed opportunities will abound.

With this in mind, below are some high-level considerations of the tools and benefits the Bankruptcy Code offers owners, investors and lenders facing distressed real estate situations.

Bankruptcy Sales and Reorganization Plans

It is not uncommon for borrowers facing a foreclosure sale to file for relief under the United States Bankruptcy Code. With broad protections, including the imposition of the automatic stay, which halts lawsuits and foreclosure sales, debtors in Chapter 11 bankruptcy are given “breathing room” to restructure their debts or sell assets. During this “breathing room,” investors have an opportunity to provide a solution to struggling owners or existing lenders—both of whom may be looking for a buyer, a replacement lender, or similar rescue capital.

Bankruptcy Code section 363(f) allows for the sale of property “free and clear” of liens, claims and encumbrances. Known as a “363 sale”—to induce a party to become a “stalking horse” buyer, which is typically subject to higher and better bids, the Bankruptcy Code allows for bid protections such as break-up fees, expense reimbursements and agreed-upon bid procedures. For underwater assets, or those with adverse claims or judgments against them, the 363 sale allows for a “cleansing” sale process—and for the buyer to acquire the title “free and clear” of liabilities unless those liabilities are specifically assumed. Importantly, at a 363 sale, the lender with a valid mortgage is typically allowed to “credit bid” its mortgage. Distressed investors often look to acquire the mortgage, typically at a discount, to allow the investor to credit bid the full amount of the mortgage—or, as occurs from time to time, allow another buyer to overbid, thus leading the debt purchaser to achieve a positive return on its debt purchase. Of course, there are also potential risks for the mortgage debt purchaser, including the situation where a debtor does not conduct an auction sale but instead elects to file a plan of reorganization that could, among other things, seek to “term out” or “cram down” the loan, as explained below.

Unlike bankruptcy section 363 sales, which are often completed in 30 to 60 days (depending on the type of asset and how long it was marketed for), debtors may also use the tools of Chapter 11 for a variety of different restructuring transactions under a Chapter 11 plan, including sales, rights offerings, debt for equity swaps and exit re-financings. Some of these tools include the ability, under certain circumstances, to file a plan of reorganization that seeks to “cram down” the lender and force terms upon it, over its objection, including extending the loan (even one that has matured), reducing the restructured loan amount to the value of the property, and/or paying the loan out over time at market rates of interest. Such plans of reorganization are often contested and can lead to protracted litigation. It is often advisable for the distressed investor to engage in negotiations with the debtor on a consensual Chapter 11 plan—one that is done on mutually agreeable terms and can be effectuated efficiently and consensually, either in a so-called “pre-packed” or “pre-arranged” Chapter 11 case.

Source: Trepp, Morgan Stanley

Other provisions

In addition to the “cleansing” nature of a bankruptcy transaction, the Bankruptcy Code also allows for special exemptions from applicable tax and securities law to assist debtors in achieving a successful Chapter 11 plan of reorganization. For example, certain transactions done under a plan of reorganization may be exempt from transfer taxes and mortgage recording taxes under Bankruptcy Code section 1146. For larger real estate debtors, there could be significant tax efficiencies and savings to consummating a transaction under a Chapter 11 plan or reorganization. The Bankruptcy Code also has an exemption, found in section 1145, from registration requirements under Section 5 of the Securities Act of 1933—as well as state law equivalents, when securities are issued to creditors in exchange for a claim against the debtor, under a plan of reorganization. Public companies (such as REITs) filing reorganization plans featuring debt for equity swaps, rights offerings, or similar transactions have used the securities exemptions successfully to attract capital and maximize value.

Simply said, Chapter 11 offers a very good opportunity for the distressed investor. Understanding the rules, pitfalls and benefits of the Chapter 11 process is essential for success.

Adam H. Friedman is a partner at Olshan Frome Wolosky LLP. He may be reached at AFriedman@olshanlaw.com.

This publication is issued by Olshan Frome Wolosky LLP for informational purposes only and does not constitute legal advice or establish an attorney-client relationship. In some juridictions, this publication may be considered attorney advertising.

You must be logged in to post a comment.