CREFC: Financing Demand Expectations Hit Record High

The organization’s new sentiment index points to a market that feels increasingly open for business.

Commercial real estate financing executives are increasingly optimistic for the year ahead, anticipating increased borrowing demand for financing new acquisitions and for refinancing loans as the maturity wall looms.

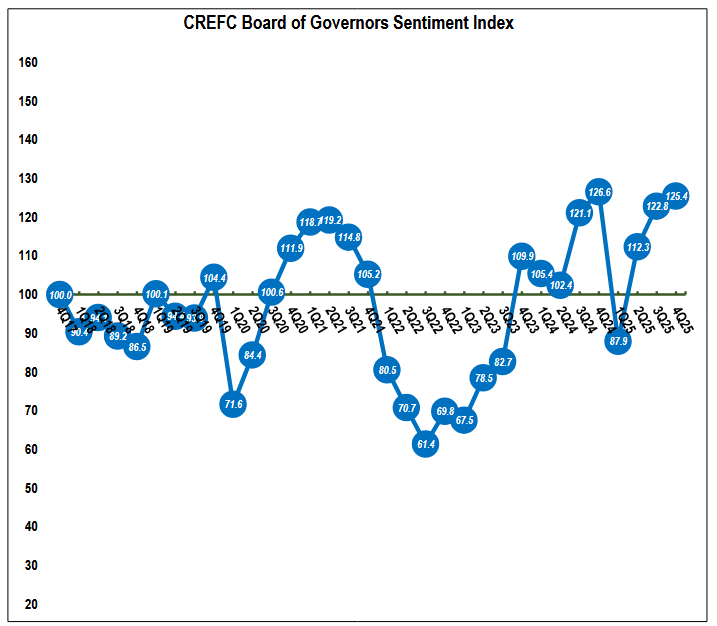

The 2026 optimism was apparent in the CRE Finance Council’s fourth-quarter 2025 Board of Governors Sentiment Index, which marked the third consecutive quarterly increase, signaling that sentiment is consolidating near peak levels.

The index rose 2.1 percent to 125.4 from 122.8 in the third quarter of 2025, approaching the all-time survey high of 126.6 set in the fourth quarter of 2024. Conducted from Jan. 5 through Jan. 9, the survey captured continued optimism anchored by record-high financing demand expectations and the elimination of negative sentiment on both interest rates and overall industry outlook. The survey found a record 97 percent expect increased borrower demand over the next 12 months, up from 95 percent the previous quarter.

The index showed 74 percent hold positive outlooks for overall commercial real estate finance businesses—the highest since the fourth quarter of 2024—with 26 percent neutral and zero negative responses for the first time since the same quarter.

“For the first time in quite some time, the results reflect a market that feels increasingly open for business,” Lisa Pendergast, CREFC president & CEO, told Commercial Property Executive.

Pendergast said key factors driving the upbeat tone come from not only Federal Reserve actions to lower benchmark rates and thus mortgage and capitalization rates, but also from anticipation of record-high financing demand.

Noting that CREFC research shows some $663 billion in commercial and multifamily loans are set to mature this year, Pendergast said both factors “clearly signal a more positive outlook for new financing and the refinancing of mature multifamily commercial real estate assets.”

Regarding the Sentiment Index, she said, “overall activity remains well diversified across CREFC membership on issues such as the economy, federal policy and interest, mortgage and capitalization rates.”

On interest impact, the sentiment rate moderated slightly from the third quarter’s peak but remained strongly positive, with 69 percent expecting favorable impacts from mortgage and cap rates, 31 percent neutral and no negative responses for the second consecutive quarter.

The survey also found 74 percent of respondents expect increased investor demand for commercial real estate and multifamily assets, with no respondents anticipating less transaction activity. On commercial real estate fundamentals, expectations strengthened, with 51 percent anticipating improving fundamentals—including occupancy, rents and property-level net operating income—up from 46 percent in the third quarter. Those who expect deterioration held steady at 14 percent.

“On the securitization front, volumes on the CMBS and CRE CLO fronts are solid, as most anticipate new supply to hold relatively steady around recent highs,” Pendergast told CPE. “It looks like 2026 will follow the trend of 2025, with growing CMBS and CRE CLO issuance rising to net-net.”

READ ALSO: CRE Fundraising on the Rise as Investors Return

While the members are watching activity in Washington, D.C., closely, whether it be with federal regulators or Congress, Pendergast said the index highlighted that 60 percent of the membership now expects positive impacts from federal legislative and regulatory actions. The survey found 34 percent remained neutral while just 6 percent expect adverse effects.

‘Bifurcated landscape’

Pendergast noted that while the data is looking better for this year, uncertainties remain as respondents acknowledge persistent credit stress and a bifurcated landscape for asset performance. She stated members are realistic about what lies ahead, noting in particular that the “maturity wall will be a sorting mechanism, not a rising tide.”

She said access to capital will depend on asset quality, sponsor strength and realistic underwriting. Pendergast added the ‘haves versus the have-nots’ was a running theme through the open-ended responses to the survey and said it “is the defining dynamic heading into 2026.”

For example, the index found only 11 percent anticipate a broad refinancing resurgence, reflecting the view that improving liquidity won’t translate to uniform outcomes. That was particularly true in comments on the estimated $200 billion in private-label CMBS maturing through 2026, including about $140 billion in single-asset, single-borrower CMBS. Sixty percent of respondents expect bifurcated outcomes with institutional-quality assets and strong sponsors refinancing successfully while Class B properties face principal losses.

Asked about other refinancing trends to watch in 2026, Pendergast told CPE, “there is growing confidence in certain asset classes, even selectively in sectors like office, being able to refinance more readily as property cash flows continue to recover and grow.”

However, she noted that challenges remain, even with the improving rate environment.

“Many maturing mortgages have substantially lower mortgage rates than what can be garnered today,” Pendergast said. “Further Fed easing, if it’s in the offing, certainly will help.”

The members also cited underwriting standards as an item to watch in 2026, with 23 percent stating pro forma underwriting that doesn’t reflect in-place cash flows as their primary credit concern. Another 23 percent flagged continued LTV/DSCR drift if competition intensifies.

You must be logged in to post a comment.