Commercial/Multifamily Borrowing Down 49% in Third-Quarter 2023

Commercial and multifamily mortgage loan originations were 49 percent lower in the third quarter of 2023.

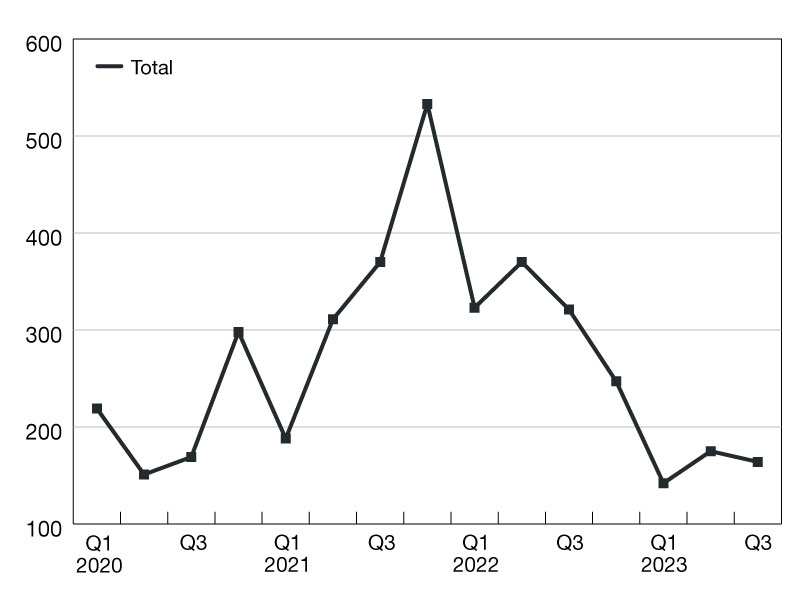

Source: Mortgage Bankers Association

Commercial and multifamily mortgage loan originations were 49 percent lower in the third quarter of 2023 compared to a year ago, and decreased 7 percent from the second quarter of 2023, according to the Mortgage Bankers Association’s (MBA) Quarterly Survey of Commercial/Multifamily Mortgage Bankers Originations, released this month.

Borrowing backed by commercial real estate properties declined again in the third quarter. Borrowing and lending were down for every property type and capital source from one year ago. However, compared to this year’s second quarter, volumes were more stable and some sectors – including industrial properties and life company lenders – showed an uptick in volume.

Year-to-date CRE mortgage borrowing has fallen 44 percent, driven by questions about some properties’ fundamentals, uncertainty about property values, and higher and volatile interest rates. Greater certainty around those conditions is a key prerequisite to breaking the logjam of transaction activity.

Originations decrease 49 percent in third-quarters 2023

Decreases in originations for all major property types led to the overall drop in commercial/multifamily lending volumes when compared to the third quarter of 2022. There was a 76 percent year-over-year decrease in the dollar volume of loans for health care properties, a 52 percent decrease for hotel properties, a 51 percent decrease for retail properties, a 50 percent decrease for multifamily properties, a 49 percent decrease for office loans, and a 35 percent decrease for industrial properties.

Among investor types, the dollar volume of loans originated for depositories decreased by 73 percent year-over-year. There was a 55 percent decrease for investor-driven lenders, a 27 percent decrease in government sponsored enterprises (GSEs – Fannie Mae and Freddie Mac) loans, a 5 percent decrease for commercial mortgage-backed securities (CMBS), and a 4 percent decrease in the dollar volume of life insurance company loans.

You must be logged in to post a comment.