A Bit Up, a Bit Down: Manufacturing’s Mixed Bag

Find out how changes in federal government policy and market conditions are impacting the sector.

There was plenty of progress and pullback in U.S. manufacturing investments this year, often driven by changes in federal government policy as well as market conditions, financing and shifting demand, according to Savills Research’s 2025 manufacturing report.

While announcements of new manufacturing projects remain strong, many projects are advancing unevenly with some electric vehicle and clean-energy-related projects being delayed or scrapped as tax credit incentives shift from clean energy to aerospace, defense and grid/energy developments with the change in administration at the federal level.

“The extent and speed at which this transition is happening is noteworthy and reflects both changing policy and markets. This has led to an interesting situation where we see new activity picking up at the same time as ongoing projects are stalling out at historically high levels,” Mark Russo, vice president, industrial research at Savills, told Commercial Property Executive.

The report notes some sectors—like defense and energy—are expanding, while others tied to earlier incentive cycles are slowing or being restructured. Savills noted three sectors—aerospace & defense, grid & energy and digital infrastructure—made up 75 percent of new manufacturing projects in 2025. And nearly half—48.7 percent—of the new manufacturing jobs announced this year were driven by the aerospace and defense sector, reflecting the continued national emphasis on security and advanced production.

READ ALSO: Why Industrial’s Booming on the Southern Border

Savills states another 24.9 percent of recent announcements involved the grid and energy or digital infrastructure verticals, areas linked closely to the growth of artificial intelligence. In particular, manufacturing for the AI future is a growth sector, including everything from servers for data centers to power transformers.

The report cites Tesla’s new Megafactory in Brookshire, Texas, where large-scale “Megapack” batteries for grid energy storage will be produced. Hitachi Energy and Eaton have announced transformer plants to meet surging grid demand and Jabil will be producing datacenter hardware in Rowan County, N.C. They are all examples of how AI’s rapid expansion is impacting industrial investment.

Meanwhile, of the projects announced since 2021 that have stalled or been canceled, 60.2 percent were linked to EV battery and related initiatives due to slowing demand, reduced subsidies and emerging global overcapacity.

However, Russo said some projects pivoted to take advantage of the policy shift in tax credits and he expects to see more of it.

“Ford recently announced it will be converting existing EV battery manufacturing capacity in Kentucky to make battery storage for data centers,” he said. “These sites in most cases have already gone through a vetting process for power, accessibility, workforce, permitting, etc., so if one type of venture doesn’t pan out, they are extremely valuable to convert to support better growing sectors.”

Closer look at jobs, projects

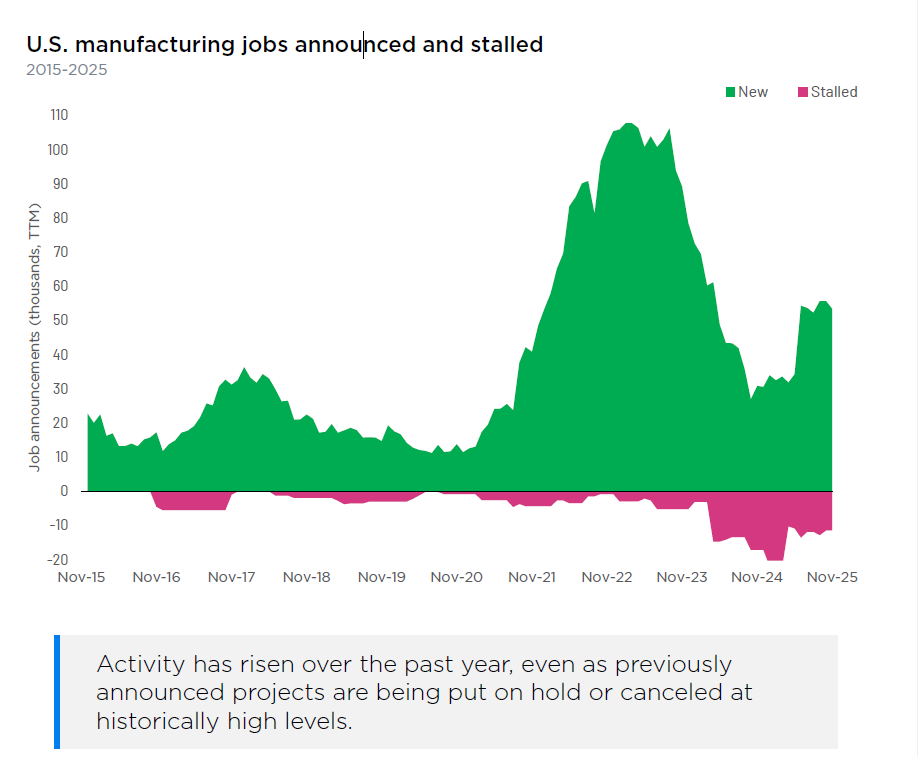

Russo said the main takeaway from this year’s report is that manufacturing is up significantly from last year in terms of new major commitments, but it’s nowhere near the heights seen in 2022. Between November 2024 and November 2025, 53,416 manufacturing jobs have been announced, up from the previous year’s total of 30,853. The announced jobs still trail the five-year average by 15.4 percent and are less than half the peak level seen in 2022. Also concerning is that announcements of stalled projects are 46.8 percent above the five-year average.

But there is good news. Total capital investment from 2025 megaprojects reached $42.2 billion, according to Savills. The firm notes that’s an impressive number but far short of the White House’s tally of investments in the trillions. Savills data includes only projects with a defined location and timeline, not long-term pledges.

“The issue with these trillions of dollars in corporate pledges is that not only are they not concrete in terms of timing, but they tend to mix in operating and supplier spending,” Russo said. “It’s important to look specifically at the earmarked capital investment for new manufacturing plants, as we do at Savills, to have an accurate understanding of momentum.”

Russo added that, as the report points out, a significant portion of even the committed projects do not make it to completion.

Asked about how the Trump administration’s tariff policy was impacting plans to reshore and onshore more manufacturing production, Russo said one problem is the tariff policy continues to be in a state of flux.

“At this point, it can be viewed as a tailwind for some types of manufacturing but ultimately not going to make or break a long-term strategy given the uncertainty around it,” he said.

Russo noted tariffs can be stimulating for manufacturing.

“But it’s complicated because some manufacturing processes rely heavily on imported inputs,” he added.

The report also notes that because the tariff rates have shifted repeatedly throughout the year, the volatility makes long-range planning for new manufacturing sites difficult.

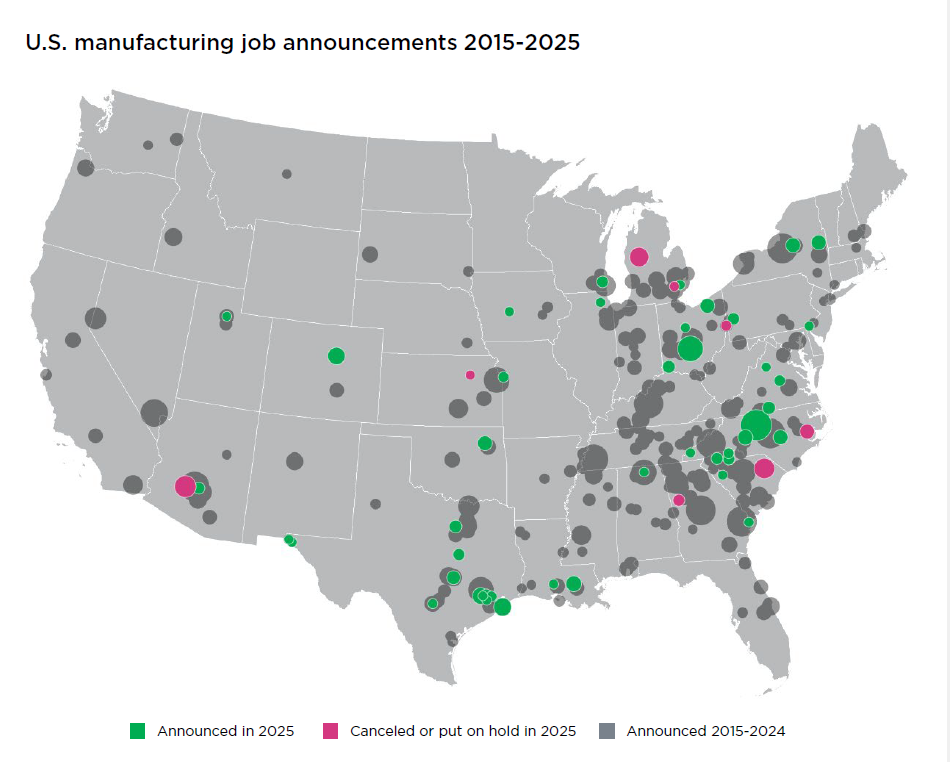

While policies may have shifted with the changes in federal government, manufacturing investments across the U.S. remain primarily in the Sun Belt, Southeast and Mid-South. Savills reports the top five states—Georgia, Texas, North Carolina, Arizona and Tennessee—account for more than half of the manufacturing job announcements since 2021, consistent with broader industrial real estate trends shaping location decisions. The firm notes this pattern is expected to hold even as the sectors driving manufacturing evolve.

You must be logged in to post a comment.