Industrial Report: Policy Shifts Boost Reshoring, Vacancies Rise

New tax incentives are supporting onshore investment amid cooling rent growth and rising vacancies, according to Yardi Matrix data.

Federal policy is giving the industrial sector a new tailwind as growth moderates. The recently passed One Big Beautiful Bill Act restores one hundred percent bonus depreciation and immediate expensing for domestic research, measures expected to encourage more onshore investment and facility upgrades. At the same time, weaker incentives for some green-energy projects have led manufacturers to reassess expansion plans.

Even so, reshoring momentum remains strong as companies prioritize reliable supply chains and regional networks. Market fundamentals point to a sector returning to balance: rent growth has cooled from record highs, vacancy has inched up and tenants now hold greater bargaining power than in recent years.

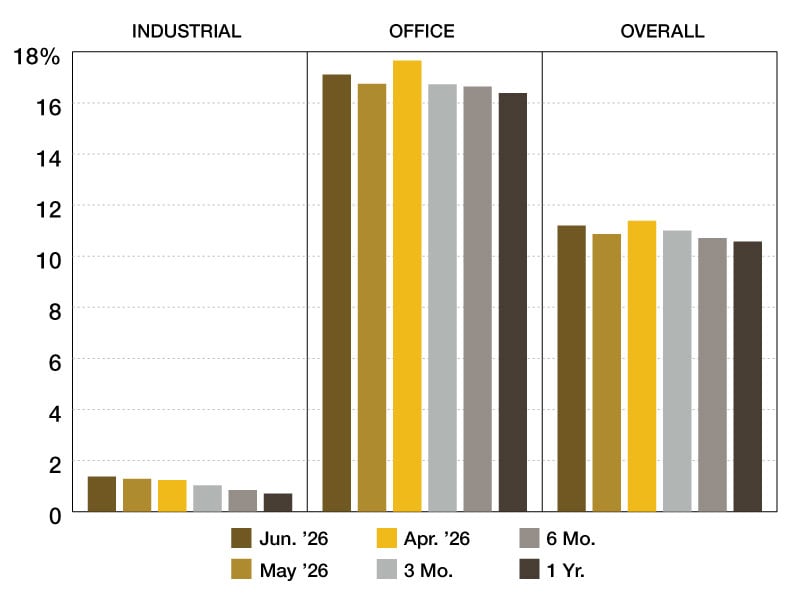

Rent growth cools as tenants gain leverage

National in-place industrial rents averaged $8.72 per square foot in September, according to Yardi Matrix data. Market leadership has rotated from the busiest gateway ports toward second-tier ports and inland hubs tied to population growth. Philadelphia led annual in-place gains at 8.7 percent, followed by Atlanta and Miami at 8.5 percent each. The Inland Empire at 7.6 percent and New Jersey at 7.4 percent also posted solid increases, though well below the double-digit pace of recent years.

The national vacancy rate reached 9.5 percent—up 250 basis points in the past year—as the industrial sector works through more than 2.7 billion square feet delivered since the start of the decade. The gap between new-lease rates and in-place rents narrowed to $1.28 per square foot, with a national new-lease average around $10.00, down from the $2.20 gap seen a year earlier—clear evidence that negotiating power has shifted toward tenants.

READ ALSO: How AI-Powered Tech Is Reshaping Industrial Real Estate

Development eases while capital trickles back

Development activity is slowing as the industrial pipeline adjusts to softer demand. Nationwide, 340.5 million square feet of space is under construction, representing 1.7 percent of existing inventory, Yardi Matrix data shows. Year-to-date completions reached 219.4 million square feet, while new starts totaled 186.1 million square feet. The largest pipelines are concentrated in Dallas–Fort Worth (56.3 million), Phoenix (33.7 million) and the Inland Empire (27.5 million), where developers continue to focus on large distribution centers and build-to-suit projects.

The industrial sales volume totaled $52.5 billion year-to-date through September, at an average price of $142 per square foot. Following three rate cuts late in 2024 that lowered borrowing costs by a full percentage point, last year’s sales volume ended 15 percent higher than in 2023. Activity so far in 2025 is slightly ahead of the same period last year, putting the market on pace for its strongest year since 2022. Atlanta stands out, with pricing up 31.3 percent to $140 per square foot, underscoring continued investor confidence in its multimodal logistics network and proximity to the Port of Savannah.

Read the full report.

You must be logged in to post a comment.