A Better Year for CRE?

Key takeaways from 2025’s investment trends, according to DLA Piper’s annual survey.

As years go, 2025 had more than its share of turmoil, economic or otherwise, including tariff gyrations, geopolitical uncertainty, interest rate concerns and currency fluctuations.

Even so, commercial real estate enjoyed some positive momentum overall, with both transaction volume and commercial real estate lending increasing year-over-year, according to the latest DLA Piper real estate report.

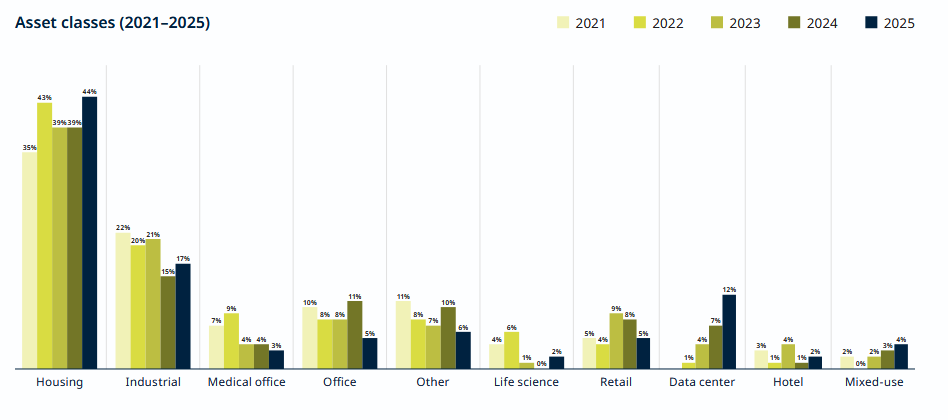

The most favored property type remained residential, just as it did last year, but data center transactions mushroomed as the adoption of AI pushed demand for the property type to new heights, the report found.

Investor interest in industrial assets remained relatively strong as well, while other asset classes were considerably less favored. All together in 2025, investors spent more than $225 billion on multifamily, office, industrial and retail properties, DLA Piper reported.

In preparing the report, the law firm analyzed more than 1,100 purchase and sale agreements and more than 650 property management agreements handled by DLA Piper from 2020 to 2025.

Data centers boom, industrial holds its ground

Among the nonresidential property types, 2025 was a year in which data centers got themselves noticed even more among investors, with investment volume spiking to 12 percent of total investments, up from 7 percent a year earlier—a near doubling. As recently as 2022, the report noted, only 1 percent of all sales were data centers.

As for industrial transaction volume, it edged up from 15 percent to 17 percent year-over-year, with activity concentrated in logistics and self storage, the report found. Bryan Conolly, chair of DLA’s U.S. real estate practice, said that trend was something of a surprise.

“This could reflect increased optimism for that asset class in light of anticipated onshoring and industrialization in the U.S.,” Conolly told Commercial Property Executive.

By contrast, sales of office and retail properties trailed other asset classes in 2025, with year-over-year slides in transaction share. Mixed-use assets were a relative bright spot, increasing by 1 percentage point from 2024, which DLA Piper posits indicated continued demand for integrated, amenity-rich environments.

Multifamily assets accounted for 44 percent of investments, up from 39 percent a year ago.

“Given the housing shortage that exists throughout the U.S., as well as significant barriers to new construction in many markets, it’s not surprising that housing assets accounted for a significant part of our transactional activity last year,” Conolly told CPE.

READ ALSO: Data Center Expansions Push the Sector Into New Territory

What is somewhat surprising, he added, is the significant (4.5 times higher) increase seen in transactions involving mobile/manufactured housing, demonstrating the increasing appetite of institutional investors for alternative asset classes.

Financial contingencies down slightly

The report also covered financial contingencies among the transactions handled by the company, finding a slight decrease in the total percentage of transactions in which financing contingencies were present, down from 10.24 percent in 2024 to 9.69 percent in 2025.

The composition of the contingencies shifted meaningfully within that narrow slice of activity, DLA Piper also noted. Among transactions that the company handled in 2025 that included a financing contingency, there was more of an even balance than in prior years between buyers pursuing new loan originations and buyers proceeding via loan assumptions.

“This perhaps reflects a pragmatic response to rate volatility, existing debt terms and timing considerations,” the report said.

The report also found that the most common survival period for representations and warranties continued to be 270 days, a period common to 35 percent of the transactions DLA Piper handled in 2025. That was actually down from the year before, when 44 percent had that period.

The number-two most popular survival period was 180 days, which had a 29 percent frequency in 2025, up from 27 percent the year before.

Remedies for a seller’s breach of its representations and warranties remained highly deal-size dependent in 2025. Average basket amounts (that is, the minimum amount of aggregate damages that a buyer must incur before it may make a claim) were relatively stable for transactions under $125 million; they moved higher in the $125-million-to-$250-million band; and they moved lower in transactions above $250 million,

Property management fees remained largely stable in 2025 compared with the year before for most asset classes. The most notable shift in property management agreements last year was the greater use of property manager liability caps, the report found.

Inclusion of a liability cap rose from 9.21 percent in 2024 to 15.56 percent in 2025.

“This increase correlated with the rise in industrial transaction volume and was most evident in acquisitions with well-established property management companies,” the report explained. “The move possibly reflects heightened attention to insurability, lender expectations and governance frameworks in operationally intensive assets.”

You must be logged in to post a comment.