CREFC: Rate Volatility Remains Top of Mind for Executives

The group's latest survey shows finance leaders settling into a more cautious outlook, even as borrowing costs continue to weigh on activity.

Commercial real estate finance executives continue to express concerns over interest rate and cap rate uncertainty and their impact on CRE lending and investment for the second half of 2026, according to the CRE Finance Council.

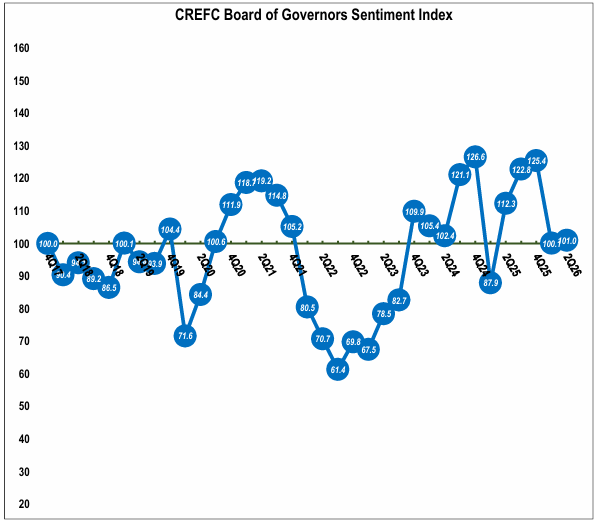

The concerns came through in both the core and topical questions asked by CREFC in its Second-Quarter 2026 Board of Governors Sentiment Index survey results.

Interest rates remained the most negative core question for the second consecutive quarter. A majority, 53 percent, expect a negative impact from elevated mortgage and cap rates, while 37 percent are neutral and 11 percent expect a positive impact.

Asked which rate-related factor will most constrain CRE lending and investment in the second half of the year, respondents split almost evenly between rate volatility and uncertainty about the path (47 percent) and rates staying higher for longer (45 percent).

READ ALSO: Reading the Rate Map

When combined, that means 92 percent of the respondents chose either the level or the volatility of rates as the binding constraint on activity in the second half of this year.

“CREFC’s Board of Governors clearly believe that the rate environment is unlikely to change for the better, barring any unforeseen issues that may cause a significant downturn in the economy and thus the increased likelihood of Fed easing,” Lisa Pendergast, president and CEO of CREFC, told Commercial Property Executive.

Pendergast referred to the $875 billion in CRE loans set to mature in 2026 and noted that the current rate environment suggests it will be challenging to refinance those loans given the elevated benchmark and mortgage rates.

“Think of loans maturing with a 4 percent coupon going to 6 percent or higher,” she said, adding the elevated volume of maturing loans continues through 2027 and 2028 at $652 billion and $591 billion respectively.

Sentiment improves, but members still cautious

Overall, the sentiment index rose 0.9 percent to 101.0 from 100.1 in the first-quarter survey. That’s near the survey’s fourth-quarter 2017 baseline of 100.0 after the prior quarter’s 20.2 percent decline.

The survey was conducted from June 25 through July 6 and captured a market stabilizing after the geopolitical shock, including the war in Iran and rising oil and gas prices, that drove the first quarter’s decline.

But CREFC noted that results were mixed and seemed to reflect a cautious mode rather than conviction. Neutral was the most common answer on seven of the nine core questions, which asked about economic outlook, federal policy, interest rate impact, CRE fundamentals, transaction activity, financing demand, market liquidity, CMBS/CRE CLO outlook and overall industry sentiment.

Pendergast said the results show members have moved to the middle after the first quarter’s shock, reflecting a market that is disciplined.

“Demand for financing remains net positive, liquidity is steady, and the questions our members are focused on—capital rules, underwriting standards and how bank capital reaches the market—are the right ones for this stage of the cycle,” she said.

Closer look at core questions

A majority of the respondents (58 percent), said they expect the U.S. economy to perform the same over the next 12 months, while 24 percent expect worse and 18 percent expect improvement.

Thirty-seven percent of respondents expect improving fundamentals such as NOI, occupancy and rents, while 53 percent expect no change. Eleven percent expect deterioration, compared to 22 percent in the first quarter.

Borrower demand cooled the most out of the nine core questions, with 45 percent expecting more demand, down from 71 percent in the first-quarter survey. Forty-two percent expect no change and 13 percent less demand.

Asked if investor demand for CRE and multifamily assets would change in the next 12 months compared to last year, 42 percent responded they expect more demand, down from 61 percent the previous quarter. Forty-seven percent said they expect no change and 11 percent responded they expect less demand.

READ ALSO: Finding the Exit Ramp in a Stalled Market

Market liquidity expectations stabilized after the first quarter’s caution. The survey showed a large majority of 71 percent expect no change, while 24 percent expect improved liquidity, up from 20 percent in the previous quarter. Just 5 percent expect worse conditions, down from 23 percent in the first-quarter index.

When asked about CMBS and CRE CLO demand and spreads and their impact on CRE finance-related businesses over the next 12 months, responses firmed, with 37 percent expecting a positive impact. That’s up from 33 percent in the first quarter. Half are neutral and 13 percent expect a negative impact, down from 18 percent in the first quarter survey.

Sixty-eight percent of respondents have a neutral outlook for the overall CRE finance industry for the next 12 months, with 24 percent taking a positive outlook and just 8 percent registering a negative outlook, down from 22 percent in the first quarter.

Following federal actions and impacts

The ninth core question asked how federal legislative and regulatory actions will impact the industry over the next 12 months. Nearly half expect a neutral impact, while the remainder are split equally between positive and negative at 26 percent each.

Pendergast told CPE that CREFC and its government relations team “are very much focused on more blocking and tackling issues as they relate to both housing and more general CRE issues, such as the continued conversions of office to multifamily.”

She called the bipartisan 21st Century ROAD to Housing Act, which officially became law on July 11, “a solid step in the right direction” to increase housing supply, assist with financing and reduce barriers to development.

Asked whether the upcoming midterm elections in November might impact legislative issues impacting the industry, Pendergast conceded there may be a slowdown in progress on still open issues on the legislative front.

“Regulators will continue to be busy with regulatory implementation,” she said. “Think Basel III Endgame, heightened regulatory oversight of bank CRE exposures, the implementation of the Current Expected Credit Loss accounting with banks focusing on reserves, loss estimates, certain assets and watch-listed loans.”

You must be logged in to post a comment.