What Hyperscaler Growth Means for Data Center REITs

Digital Realty Trust and Equinix are riding an unprecedented demand wave.

AI-driven hyperscaler demand is expected to grow exponentially over the intermediate term, directly benefiting data center REITs through a significant increase in demand. As a result, REIT NOI growth has been strong as companies are able to push pricing for both large hyperscale customers as well as smaller customers.

Additionally, the pace of capital deployment for development has meaningfully ramped across the sector, including through joint ventures, infrastructure funds, project finance and structured finance. Data center REITs have notably increased development spending guidance over the intermediate term.

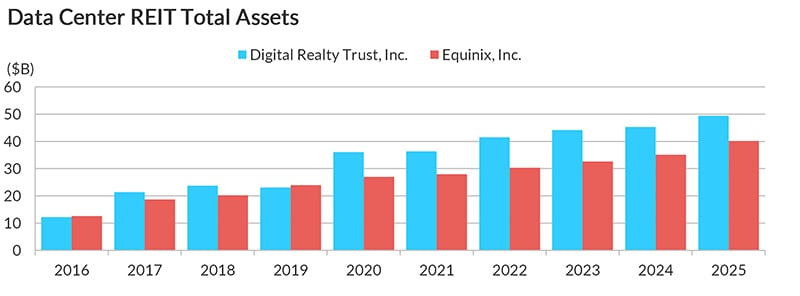

This increased investment is also evident in balance sheet growth: Digital Realty’s total assets rose from about $12 billion in 2016 to roughly $49 billion in 2025, while Equinix’s total assets increased from about $12 billion to approximately $40 billion over the same period, underscoring the sector’s sustained expansion and capital deployment capacity. Leverage remains low for both Equinix (BBB+/Stable) and Digital Realty Trust (BBB/Stable) and both companies have historically been disciplined in their spending and balance sheet management. Strong organic growth also means more retained cash that can be directed towards development.

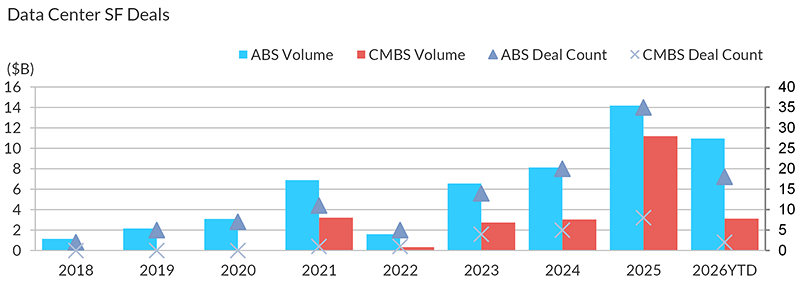

There has been a sharp expansion in structured financing for single-family data center deals across both ABS and CMBS channels, with issuance volumes and deal counts rising materially from minimal levels in 2018 to 2020 to much stronger activity beginning in 2021 and accelerating further in 2023 to 2026 YTD. ABS volume grew from about $1 billion in 2018 to roughly $14 billion in 2025, before remaining elevated at around $11 billion in 2026 YTD, while ABS deal count increased from only a few transactions to about 35 in 2025. CMBS activity also expanded meaningfully, with volume reaching roughly $11 billion in 2025 versus negligible levels earlier in the period, alongside a clear increase in deal count. Overall, data centers have become an increasingly financeable asset class within structured transactions, supported by broader investor acceptance and deeper capital markets execution.

LIKE THIS CONTENT? Subscribe to the CPE Capital Markets Newsletter

In Fitch’s view, these trends significantly improve transaction liquidity for data centers and meaningfully enhance the assessment of unencumbered data centers as a source of alternative liquidity, as owners now appear to have more established and scalable secured financing options through both ABS and CMBS markets.

Over the course of 2025, investment in information processing equipment, software and related AI infrastructure remained exceptionally strong, accounting for a large share of overall growth. AI‑related investment categories contributed roughly 0.9 to 1.0 percentage points to real GDP growth through 1Q25 to 3Q25 (around 40 percent of total growth), with their influence remaining elevated into year‑end as data‑center and cloud spending accelerated. Hyperscalers have signaled more than a trillion dollars of cumulative capex over the next several years.

At the midpoint of current guidance, 2026 spending by the “big four” (Alphabet, Microsoft, Amazon and Meta) alone would approach approximately $700 billion, roughly doubling from 2024 levels and rivaling—or exceeding—cumulative spending over 2020 to 2024, underscoring the unprecedented scale and front‑loading of the AI infrastructure cycle.

However, demand pullback remains a risk in the longer term, particularly as companies figure out how to monetize AI. If enterprise adoption and end-user willingness to pay do not scale as quickly as current infrastructure buildouts imply, capacity additions could begin to outpace realized demand. That could lead to slower leasing velocity, weaker pricing power and a more cautious approach to future data center expansion and financing.

Chris Wimmer is senior director/commercial real estate at Fitch Ratings. Anniruddha Jadhav is associate director.

You must be logged in to post a comment.