Demand Stays Hot for Medical Outpatient Buildings

But pricing challenges and policy risks remain for investors, according to a new JLL report.

In some ways medical outpatient buildings are a golden child in the commercial real estate sector, with an aging U.S. demographic supporting demand, while at the same time limited recent development is fueling growth in occupancy rates and rents, according to a new JLL medical outpatient building outlook for 2026.

Also, health-care systems and private medical groups are consolidating and thus are looking for quality MOBs. But the sector isn’t completely without headwinds, especially in the form of policy changes that will put pressure on health-care systems. Namely, near-term policy changes to Medicaid eligibility and ACA subsidies present a risk to hospital margins, since an increase in uninsured patients will strain revenue, the report noted.

More demand for MOBs

The prime underlying demand drivers for medical outpatient space in the coming years will be an aging U.S. population, but also an increasing focus on health and wellness among younger people.

“Even as declines in insurance coverage will cause some patients to forgo care, and population growth is uncertain due to changing immigration policies, the outpatient health-care sector is still projected to see volumes growing significantly faster than inpatient care,” the report explained.

Outpatient visits are forecast to increase over the next five years by 227.4 million, much of which will be driven by population change, demographic shift and the increasing prevalence of disease in the population, according to JLL’s research. The loss of insurance will have an impact on the total number of visits, but a relatively minor one, with an estimated 14.9 million fewer outpatients as a result.

More total outpatient visits won’t simply translate to more MOB utilization, though the net impact will be positive on outpatient facility fundamentals. JLL health-care clients reported in a 2025 survey that they are prioritizing reducing operating costs, optimizing space utilization and achieving organizational efficiency. In short, the industry will be pushing for portfolio optimization, which will mean outpatient expansion, but in a methodical way, not a gold rush.

READ ALSO: MOBs Stand Strong as Traditional Office Struggles

Specialties driven by aging demographics, such as physical therapy and rehabilitation, orthopedic surgery and endocrinology “offer a long runway for expansion,” the report noted. However, health-care staffing shortages could limit growth even where patient demand exists.

Annual rent growth for MOBs is down from its inflation-driven peak in 2023, but it remains healthy at 3.3 percent as of the fourth quarter of 2025. More aggressive escalations, with 3 percent annual bumps or CPI-tied provisions, are becoming increasingly common in lease deals, the report said. Rental growth is nothing new for MOBs, with the sector consistently outperforming the overall office sector since 2022.

Supply isn’t matching demand

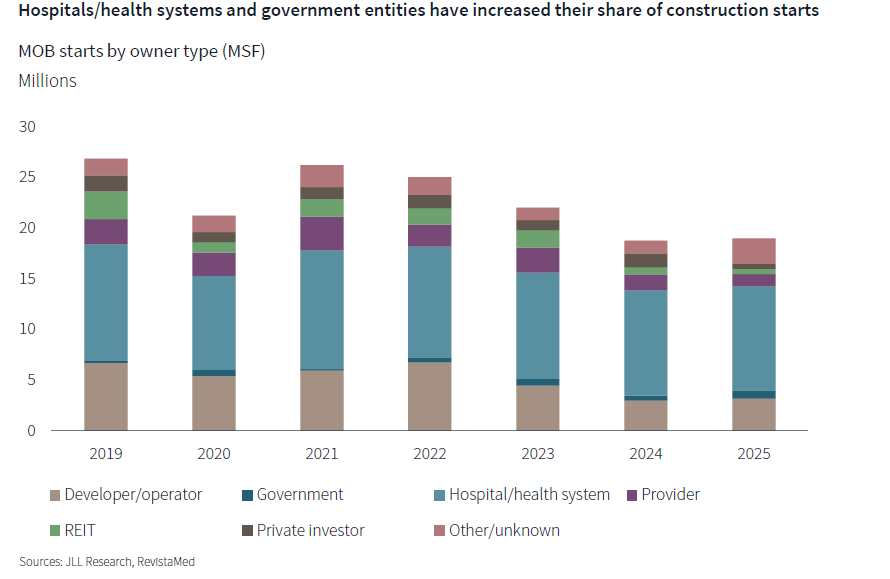

New starts for medical outpatient buildings declined to a trough of 15.7 million square feet, or 1 percent of inventory in the fourth quarter of 2024, according to JLL data. In 2025, starts began to pick up, but only marginally. In the fourth quarter of 2025, starts totaled 17.8 million square feet, or 1.1 percent of inventory, reflecting broader medical office building trends.

Developer-led starts are half of what they were in 2019, with rising costs—land and construction—making spec outpatient development difficult to pencil, despite the big picture of higher demand, the report said. Overall, starts are down 29.3 percent from 2019. Hospital and health system starts—the sector’s build-to-suit equivalent—are down just 11 percent and are unlikely to shift meaningfully in the near term.

“With continuing elevated costs and uncertain macroeconomic conditions, speculative construction will be very limited, and health systems will continue to anchor new construction, leaving limited available space for non-affiliated groups,” the report predicts.

Those outpatient buildings that are being built are increasingly complex, incorporating imaging, surgery centers, labs and physician offices in the same facility, JLL noted. Cancer-care facilities are seeing a major expansion: in 2025, over 1.3 million square feet of hospital-owned cancer treatment centers were delivered, and over 6.5 million square feet of cancer-care facilities are planned or under construction for the next few years, of which 92 percent is hospital-system owned.

Investment is strong, but dealing with uncertainties

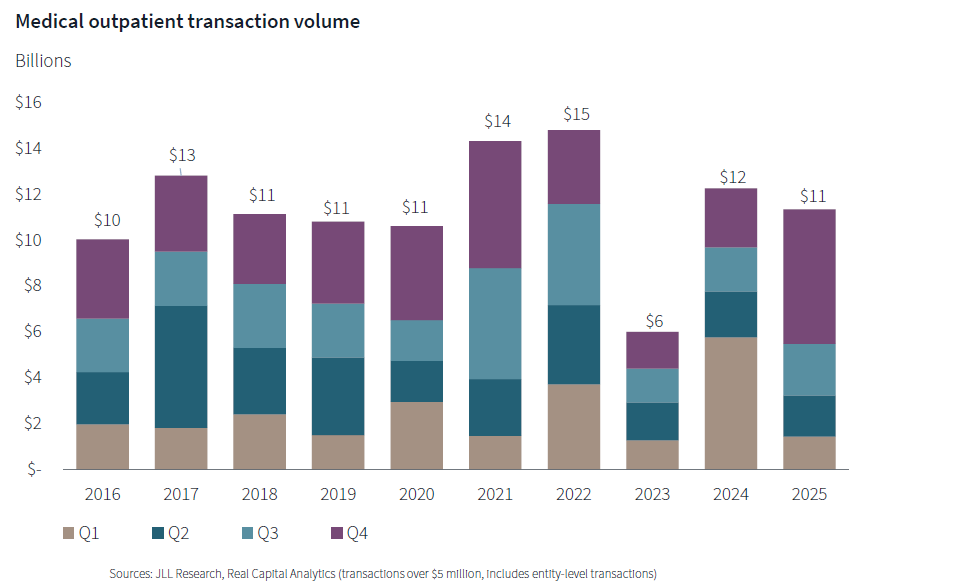

Strong fundamentals attracted investors to the sector in 2025, with an investment total of about $11.3 billion, a small step down from 2024’s total of $12.3 billion, but an improvement over 2023, when MOB investors did only $6 billion in deals. The 2025 total isn’t as high as the immediate post-pandemic year of 2022, when low interest rates encouraged investors to put $15 billion in the sector, JLL reported.

Still, there is some uncertainty associated with investing in the sector. For institutional investors, which took a much larger share of MOB purchases in 2025 than any other time in the last decade, dry powder investment is concentrated in core plus/value-add/opportunistic buckets, thus making pricing challenging for any product that doesn’t fit in one of those categories.

The current relatively low-interest-rate environment keeps deals coming, but it has also increased investor competition and narrowed bid-ask spreads, despite ongoing geopolitical uncertainty, the report noted.

Not all MOB assets are equally important to investors. Properties that offer specialty services, such as ambulatory surgical centers or facilities with advanced imaging tech, will continue to command premium prices. JLL predicts a “competitive, robust pricing environment for medical outpatient real estate in 2026.”

You must be logged in to post a comment.