MOBs Stand Strong as Traditional Office Struggles

Confidence in the sector held firm in 2025, as developers and investors pursued fewer yet bigger private capital deals.

A remarkable difference between the traditional office and medical office sectors and a trend toward fewer but individually larger private equity deals in the health-care sector are two of the key elements in the new U.S. medical outpatient insights report from Avison Young for the second half of 2025.

And for a broader context, the report also discusses a significant trend in medical role salaries.

As to that first point, AY noted that although the borrowing environment and construction costs have been difficult to surmount, ongoing tenant demand has driven medical outpatient developers to continue bringing space to the market.

READ ALSO: What’s in CBRE’s Forecast for 2026

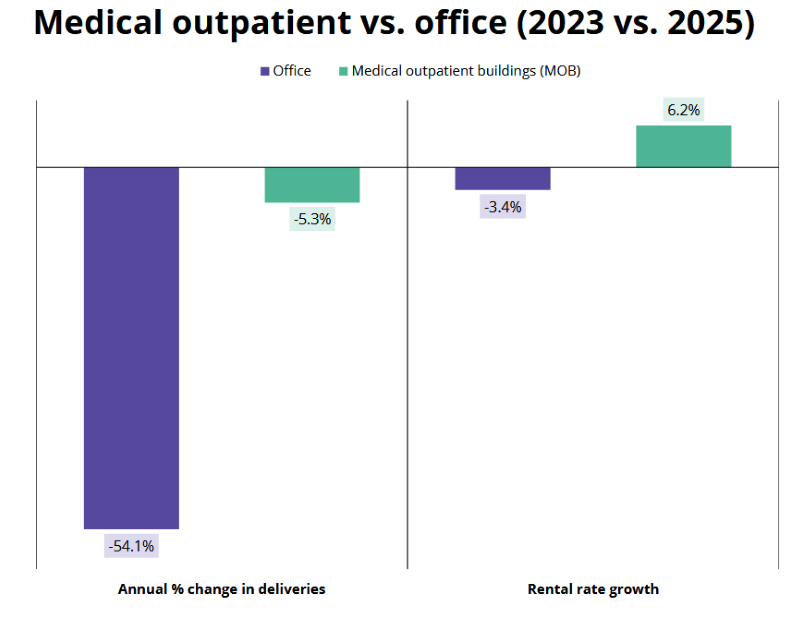

Specifically, while both the mainstream office and medical office sectors saw declines in deliveries in 2025, office deliveries plummeted by 54.1 percent, but medical outpatient deliveries declined only marginally, by 5.3 percent.

In parallel with that, office rents decreased, but medical outpatient rents posted solid growth. Further, AY reported that as of the fourth quarter of 2025, U.S. office occupancy was at 80.3 percent, while medical outpatient building occupancy was at 92.3 percent due to strong tenant demand.

On a geographic basis, MOB markets vary wildly. Among 50 markets tabulated in the report, New York City tops the inventory rankings, at about 77.3 million square feet; New Orleans is the smallest, at 4.3 million. Miami led deliveries in the second half of the year, with 471,000 square feet; 13 markets added no new space.

Memphis was the most active metro for MOB space under development, at 1.2 million square feet. Only three markets had no space in the pipeline: Birmingham, Ala., Providence, R.I., and Hartford, Conn.

MOB capital markets trends

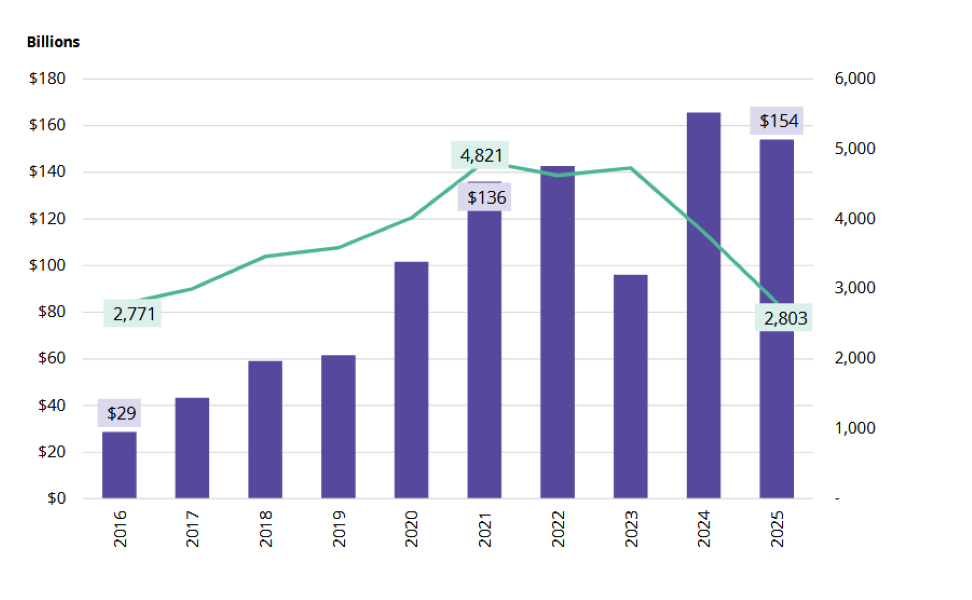

U.S. private equity health-care deal value in 2025 totaled $154 billion, according to the report. While private equity spending on medical assets has reached new highs in total volume, the number of deals has fallen, pointing to a growing preference for bigger-ticket transactions.

Although funding declined by 7 percent from 2024, 2025 nonetheless ranked as “the second-highest year for total health-care funding raised since 2016, even as deal count dropped to its lowest level in that same period.” This trend highlights a more disciplined approach, with investors prioritizing targeted partnerships and focused growth strategies over broad-based expansion.

Looking ahead, Jay Johnson Principal & Executive Managing Director, Healthcare Real Estate Services Leader, wrote that “investor demand for medical outpatient buildings is poised to accelerate in 2026, with capital flowing increasingly into the sector and transaction activity gaining momentum.” He added that medical real estate investors are showing renewed appetite for multi-asset portfolios over single-asset deals, with early signs of a pricing premium returning for portfolio offerings.

Despite rapid technological innovation and major shifts across the health-care sector, medical outpatient facilities continue to demonstrate robust resilience, according to Derek Jacobs, U.S. health-care lead of market intelligence at Avison Young.

He added that as we move into 2026, investors continue to favor medical office buildings for their reliable, long-term stability, reinforcing broader trends in commercial real estate. Demand for healthcare services keeps climbing, and providers depend on strategically located outpatient facilities to accommodate growing patient volumes. For investors, that dynamic supports steady performance and reinforces MOBs as one of the most resilient asset classes in commercial real estate.

Finally, the Avison Young report highlighted a 49 percent increase in medical role salaries: “Despite substantial changes in care methods, including those incorporating new technologies, medical hiring has continued to rise, and salaries have increased alongside it. Staffing in the medical sector is challenging in many markets, and providers remain willing to pay more for talent.”

You must be logged in to post a comment.