The Inflation Dividend: Testing CRE’s Hedging Capabilities

What history reveals about today's pricing.

For decades, commercial real estate has been widely regarded as a useful inflation hedge—a real asset whose income streams and replacement costs should, in principle, rise with the general price level.

The intuition is straightforward: Higher construction and labor costs ultimately influence replacement values, while market rents reset over time. Unlike fixed-income instruments, whose cash flows are largely fixed and are, therefore, more vulnerable to inflation’s erosion of purchasing power, commercial properties possess the ability, albeit with lags and frictions, to reprice. Yet, as with many long-held investment beliefs, this relationship merits periodic reassessment, particularly in a cycle defined by shifting monetary policy, evolving market structures, and meaningful dispersion across sectors.

LIKE THIS CONTENT? Subscribe to the CPE Capital Markets Newsletter

In this paper, we take a data-driven look at the inflation-hedging characteristics of commercial real estate by examining the long-term relationships among real estate and fixed-income performance, and inflation. Our analysis begins with the macro lens: How have property returns correlated with inflation across cycles, and how does that compare with the challenges faced by fixed income?

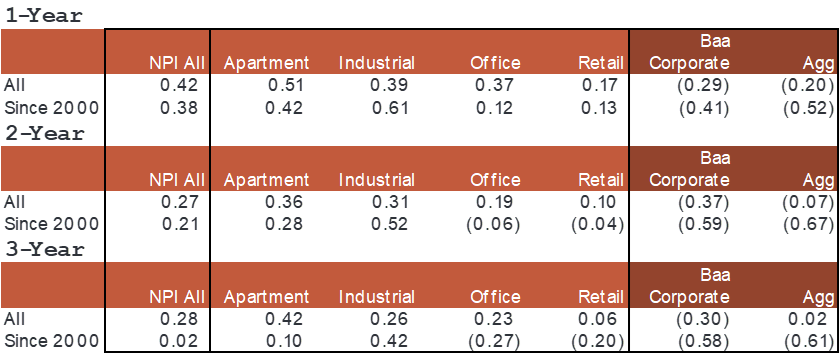

Historically, real estate returns have generally exhibited positive correlation with inflation, whereas fixed income benchmarks have demonstrated negative correlation, as shown in Exhibit 1:

- Apartment returns are more highly correlated in the short-term, with shorter contract rents enabling quicker resetting to keep pace with inflation.

- Office and retail have generally lower correlation, particularly in the post-2000 correlations, as challenges in fundamentals in recent periods have weighed on pricing power in an inflationary environment.

EXHIBIT 1: Correlation of NPI Property & Fixed Income Total Return to Inflation Over Various Periods

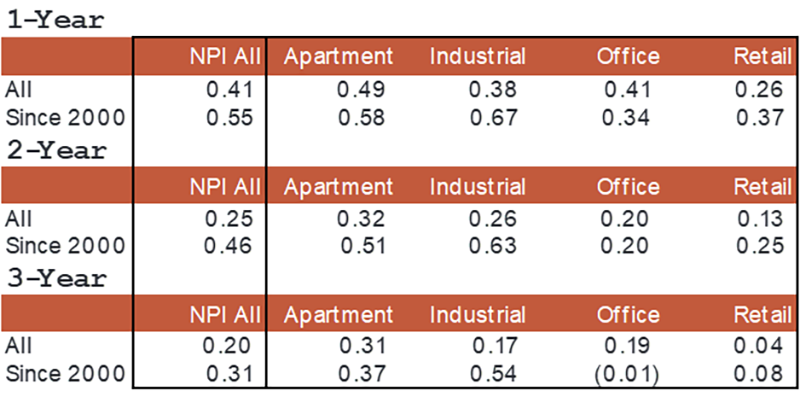

While these correlations offer a helpful starting point, they also pick up a lot of extra noise—from shifting supply-and-demand conditions to broader economic changes, not just the effects of inflation itself. To better isolate inflation’s contribution to performance, we next examine the relative return differential between real estate and fixed income, and how that spread has behaved across varying inflation regimes. By correlating the return gap with inflation itself, we seek to understand whether real estate’s perceived inflation advantage persists once broader market forces are stripped away. As shown in Exhibit 2, this generally does serve to strengthen the historical relationship and support real estate’s inflation-hedging characteristics relative to fixed income.

EXHIBIT 2: Correlation of NPI Return Spread Over Bloomberg Agg Index, vs. Inflation

Implications of current inflation for CRE pricing

Having established how real estate has historically behaved relative to inflation and fixed income, the next logical question is how investors are incorporating these dynamics into today’s pricing. If commercial real estate is viewed as offering a degree of inflation protection that fixed income cannot, then forward-looking valuations should, in theory, reflect that advantage, and be more pronounced when inflation expectations are elevated or more uncertain. This is pertinent today given that expected one-year inflation is 2.74 percent, nearly 1 percent above the average of 1.79 percent in the 15 years leading up to the pandemic in 2020.

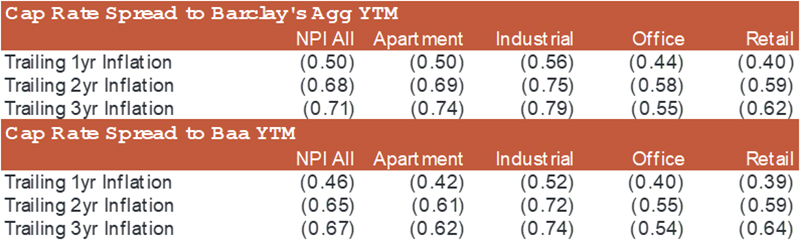

Exhibit 3 shows the correlation of inflation to current cap rate spreads versus both Baa corporates and Bloomberg Agg, and suggests that recent inflation does impact current pricing for investors. The higher recent inflation, the tighter the current real estate cap rate spread to fixed-income yields. Note that while some of this may be attributable to appraisal lag of real estate values in the historical experience, the stronger relationship over longer periods suggests this isn’t the primary driver. Unfortunately, we are unaware of a robust historical measure that would capture the dispersion of potential inflation outcomes, as this would be interesting to test as well.

EXHIBIT 3: Correlation of Inflation to Cap Rate Spreads

Given the evidence that real estate does, in fact, display meaningful inflation-hedging characteristics, and that investors price this into cap rate spreads, the natural question is: With inflation expectations still elevated, how much tighter should we expect cap-rate-to-fixed-income spreads to be today? Are investors accepting narrower real estate risk premiums because they view income growth and replacement-cost inflation as offsetting some of the duration and purchasing-power risks embedded in bonds? One way we attempted to address this question was to run regressions on historical cap rate spreads and both trailing three-year and projected one-year inflation. The results were consistent. While inflation doesn’t fully explain the tightness of today’s real estate cap rate spreads, predicted cap rate spreads incorporating recent and projected inflation do explain a meaningful portion of the tightness, as shown in Exhibit 4. On average, the majority of the difference in current cap rate spread vs. long-term average for Baa Corporate Index, and about a quarter of the divergence for the Bloomberg Agg Index, could be attributed to concerns about inflation moving forward.

EXHIBIT 4: Projected Cap Rate Spreads Based on Regresssion Results

Viewed through this lens, a component of current pricing is recognizing what the data supports: Real estate has, in fact, delivered meaningful protection against inflation over time. In a world where inflation risks remain elevated and tail risks are elevated, it’s understandable that investors would price those characteristics more highly, narrowing cap rate spreads relative to investment-grade bonds.

Mark Fitzgerald is managing director & head of research for Affinius Capital.

You must be logged in to post a comment.