Will Construction Costs Go Up in 2026?

How policy volatility continues to impact development and what that means for commercial real estate decision-makers next year.

Construction spending, which dropped 4.7 percent this year, is expected to increase slightly in 2026. But the projected increase—just 0.4 percent—is a sign that policy volatility, including tariffs, will continue to impact the U.S. market, according to JLL’s latest construction cost forecast.

JLL estimates overall construction spending to rise from $2.045 trillion this year to $2.053 trillion in 2026 and $2.137 trillion in 2027. The report expects non-residential construction spending to remain at about $681 billion for both 2026 and 2027, down from $708 billion this year and $751 billion in 2024. Residential construction spending is expected to increase from $862 billion this year to $879 billion and $938 billion in 2027. Construction spending on civil engineering projects is estimated to go from $475 billion in 2025 to $493 billion next year and $518 billion in 2027.

The forecast, released by JLL Project and Development Services, details how real estate investors and decision-makers can navigate the ongoing pressures and changes to construction economics to take advantage of opportunities.

While much of the construction industry was at a standstill in 2025 due to policy uncertainty, Louis Molinini, JLL’s head of project and development services for the Americas, said there is more clarity as the year winds down that enables strategic positioning for organizations that are ready to move forward with projects that had been put on hold or new developments.

READ ALSO: CRE Lending Momentum Hits Highest Level Since 2018

Molinini said many had taken a wait-and-see approach on 2025 construction projects rather than undertake a solution that could be impacted by a sudden change in trade policy.

“I think now as we’re starting to see some stability in those (tariffs), we can come up with solutions and work with our clients to determine the right path forward. So, you’re seeing more and more clients be willing to start advancing projects,” he told Commercial Property Executive.

“We’ve been working with clients to understand in real time, sourcing of materials by country so that we can understand potential impacts, having multiple suppliers, leveraging our strategic global suppliers and our purchasing power as a firm and that of our clients to drive those decisions and get the best outcome for our clients,” he added.

Material costs to rise

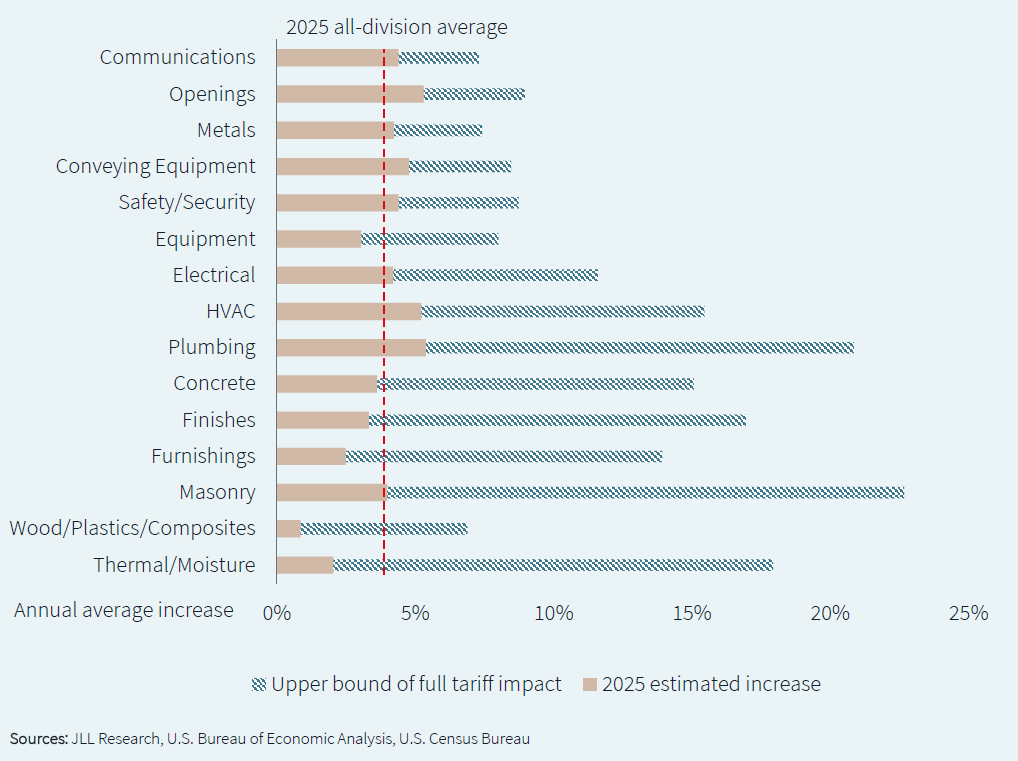

Those strategies will continue to be important in 2026 because material cost pressures are expected to intensify throughout the year ahead. While JLL’s mid-year construction outlook estimated material costs to increase as much as 7 to 12 percent, the overall increase averaged 4.2 percent above 2024 prices. That was mainly due to slower activity and suppliers burning off stockpiled materials, Molinini said. But material cost increases could range from 5 percent to 25 percent depending on the material, with an aggregate increase of about 8 percent based on current policy levels, the report noted.

Costs of materials vary by category, with mechanical and electrical components being the most in demand, particularly by the growth in data center development and other industries like manufacturing, health-care and infrastructure projects that also rely heavily on mechanical and electrical components, Molinini said.

Asked whether suppliers are still absorbing tariff increases, Molinini said it varies.

“Some are being more aggressive than others in terms of absorbing those costs to spur activity and gain market share,” he said.

That’s why JLL recommends proactive management in procurement and design decisions as well as negotiating with multiple suppliers.

“While the market is slow or slower in certain pockets, sectors or industries, you can come at it from a position of negotiating strength to try to minimize the impact to your project,” Molinini said. “Will we get to a point where all of those manufacturers and suppliers pass through everything because they’re so busy and there’s so much activity, they don’t need to incur the cost? That could be a very real outcome. But until the activity is at a point where that’s the case, we won’t really know.”

Regional construction activity

The JLL report notes that policy impact varies across the U.S. with some regions seeing more specific types of construction activity. For example, Molinini said investments in artificial intelligence are driving data center activity and office leasing in Northern California.

“From an office perspective, our technology clients are growing. They’re expanding and they’re hiring. So, we have a number of assignments that are supporting the growth of our technology clients from an office footprint perspective,” he said.

The report also notes creative and adaptive projects are moving forward. For example, JLL states office-to-residential conversions nearly doubled in 2025, “demonstrating how format flexibility and vision enable operators to capitalize on fundamental needs.”

Molinini said the type of office-to-residential work they are seeing is very much region by region and driven largely by the age of the existing building stock and vacancy rates.

“You really have to go city by city to really understand what’s driving the non-residential market in that city,” he said. “It goes back to the broader economic trends in those regions and the industry that’s based there and the outlook for that industry.”

Looking ahead to 2026 and 2027, he said he expects to start to see some advanced manufacturing projects get underway. He noted the pharmaceutical sector has already started picking sites for new U.S. facilities and announcing dates to begin development of more onshore manufacturing.

You must be logged in to post a comment.