2025 Single-Tenant Net Lease Sales Volume & Cap Rates

Top trends impacting the market, according to Northmarq.

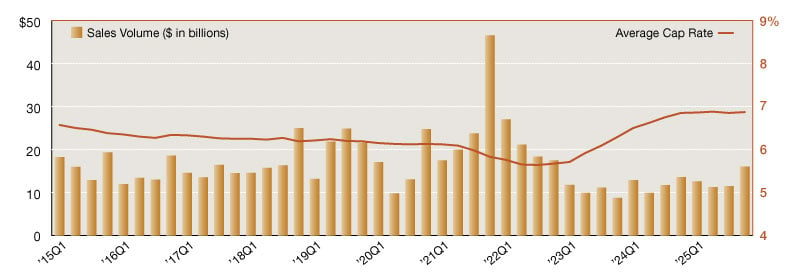

Single-tenant investment sales totaled $16.0 billion in the fourth quarter, lifting full-year volume to $51.4 billion. Activity surged 39.1 percent quarter-over-quarter and increased 12.8 percent year-over-year.

Industrial transactions totaled $8.8 billion in volume, continuing to represent the largest share of activity at 55.2 percent, though down from 61.2 percent one year ago. Office transactions followed at $3.8 billion, or 24.0 percent of total deal volume, up from 18.3 percent last year. Retail transactions accounted for $3.3 billion, or 20.8 percent, a slight improvement from 20.5 percent one year earlier.

LISTEN ALSO: Investment Matters: Institutional Eye

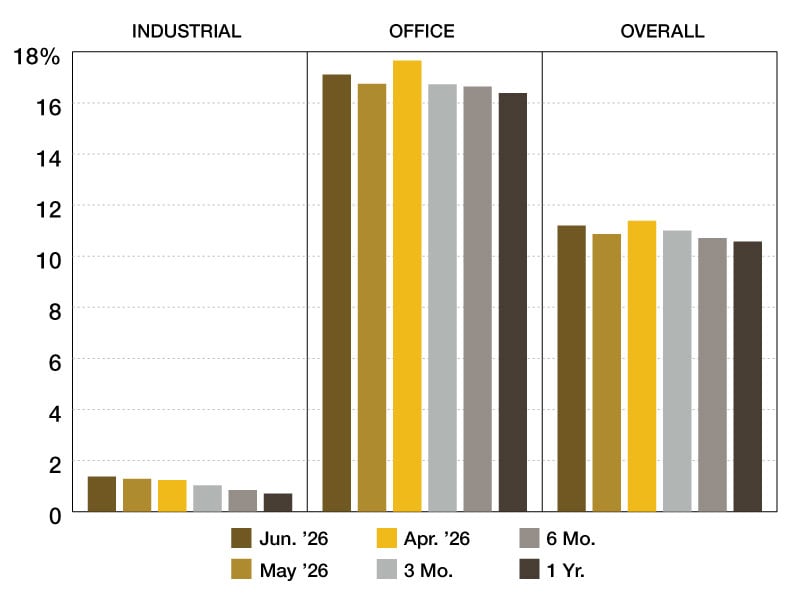

Cap rates inched up 2 basis points from the previous quarter to an average of 6.87 percent, similar to averages throughout 2025. The overall average is now 5 basis points higher than a year ago, with office posting the largest year-over-year increase.

Private buyers accounted for 53 percent of single-tenant acquisition volume through the fourth quarter of 2025, up from 43 percent in 2024, followed by institutional investors at 20 percent, slightly above 17 percent last year. REIT/Listed activity as a share of total transaction volume declined sharply, falling from 17 percent in 2024 to 8 percent in 2025.

—Posted on May 21, 2026

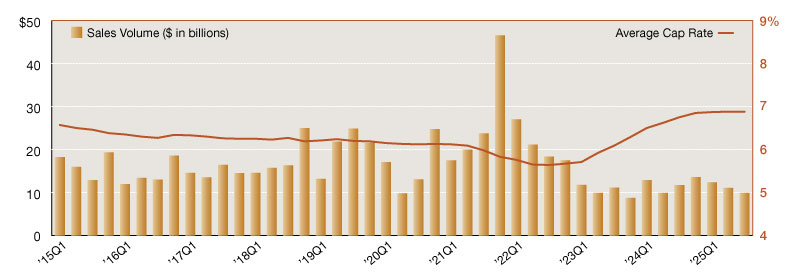

Single-tenant investment sales totaled $9.9 billion in the third quarter, bringing year-to-date volume to $33.3 billion. Activity was down 10.5 percent compared to the previous quarter and by 14.9 percent year-over-year.

Industrial transactions totaled $5.2 billion in volume, continuing to represent the largest share of activity at 52.2 percent, though down from 60.2 percent one year ago. Office transactions followed at $2.5 billion, or 25.6 percent of total deal volume, up from 17.0 percent last year. Retail transactions accounted for $2.2 billion, or 22.3 percent, a slight decline from 22.7 percent one year earlier.

READ ALSO: CREFC: Financing Demand Expectations Hit Record High

Cap rates were flat from the previous quarter at an average of 6.88 percent, a pause after a prolonged, gradual upward trend. The overall average is now 13 basis points higher than a year ago, with retail posting the largest year-over-year increase.

Private buyers accounted for 55 percent of multi-tenant office acquisition volume through the third quarter of 2025, up from 43 percent in 2024, followed by institutional investors at 19 percent, slightly above 17 percent last year. REIT/listed activity as a share of total transaction volume declined sharply, falling from 18 percent in 2024 to 8 percent in 2025.

—Posted on Jan. 28, 2025

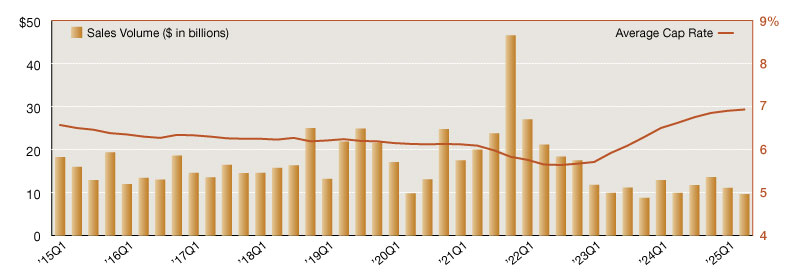

Investment activity in the single-tenant net lease market slowed again in the second quarter, with $9.6 billion in sales volume. This marks the second-lowest quarterly total in more than a decade, down 13 percent from the first quarter and 4.6 percent year-over-year. Industrial remained the most active sector with $5.4 billion in sales volume, followed by retail at $2.2 billion and office at $1.9 billion. Single-tenant net lease retail was the only sector to post a year-over-year increase, up 5.7 percent, despite a steep quarter-over-quarter decline.

READ ALSO: Single-Tenant Retail Is Back in Favor

Cap rates continued their gradual upward trend, rising three basis points to an average of 6.93 percent. We’re now 130 basis points above the market’s low point reported in third-quarter 2022. Over the past year, the overall average has increased 30 basis points, which suggests we are on a slow but steady path toward rate stabilization.

Private investors remained the most active buyer group, accounting for roughly half of all single-tenant transactions year-to-date. Institutional buyers represented 25 percent of buyer activity, up slightly from last year, while REITs have scaled back to 7 percent market share. International investors were less active overall—down to just 5 percent of the buyer pool—but in the first half of 2025, they’ve showed a preference for single-tenant retail assets more so than office or industrial.

Without a meaningful uptick in sales during the second half of the year, the single-tenant market is on pace to fall short of annual totals reported in both 2023 and 2024, which were significantly slower periods compared to the record-setting performance of 2021.

John Tagg is the Research Manager at Northmarq. He is responsible for coordinating the production and distribution of research reports that support the company’s commercial real estate brokerage and investment sales teams across local offices nationwide.

—Posted on September 22, 2025

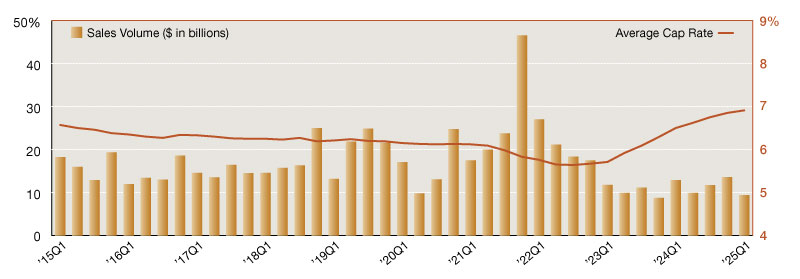

The single-tenant net lease market faced headwinds in first quarter 2025, as transaction activity declined. Total sales volume for the period reached only $9.4 billion, marking a 30 percent contraction from fourth quarter 2024. With one of the weakest starts to a year in recent history, investors continue to exercise caution as they navigate elevated borrowing costs and broader market uncertainty.

Overall single-tenant cap rates edged upward for the tenth consecutive quarter, averaging 6.91 percent at the end of first quarter. This figure represents a modest six-basis point increase from the prior reporting period and a larger 41 basis point rise year-over-year. The steady climb in cap rates reflects the recalibration of asset valuations to align with higher interest rates, which continues to impact investor pricing strategies.

Private investors maintained a dominant position in the net lease sector, comprising 46 percent of all buyers. Institutional investors, now representing 27 percent of the buyer pool, demonstrated a noticeable uptick in activity compared to full-year 2024 levels, especially in the industrial sector. Conversely, REITs reported sharply reduced activity, involved in just 4 percent of the quarter’s acquisitions. Notably, REITs remained completely absent from the single-tenant office segment, underscoring persistent challenges within the sector.

Sector-level trends revealed varied performance. The industrial sector continued to lead in investor demand with $4.6 billion in sales, although this volume was down more than 47 percent from fourth quarter 2024. Retail showed resilience recording $3.05 billion in sales and marking a 9 percent increase quarter-over-quarter despite a 26.7 percent year-over-year decline. Office transactions, on the other hand, fell to $1.8 billion – a staggering 56.2 percent decline from a year ago.

Looking ahead, cap rates are likely to expand further, and evolving buyer profiles will shape activity as investors assess risk-reward dynamics across the net lease landscape, especially as the impact of tariffs, projected interest rate cuts and other market dynamics become clearer.

—Posted on May 30, 2025

You must be logged in to post a comment.