Quantum Shift Looms for Office

What will the market look like on the other side of the pandemic?

The typical question about a recovery is how long it will take for a property sector to return to its previous status. In the case of the office market, whatever comes out on the other side of the pandemic hangover will almost certainly be substantially different from prior conditions.

READ ALSO: Economist’s View: Why Cities Will Rise Again

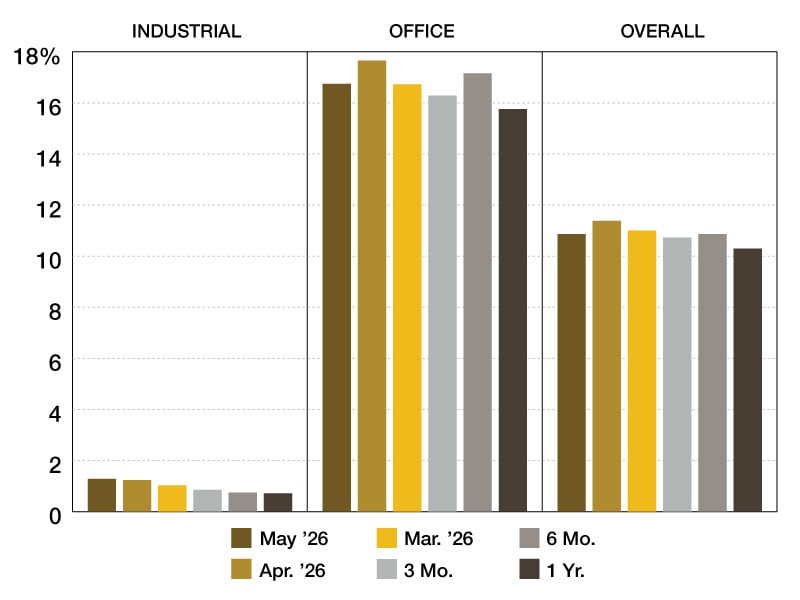

Office properties have taken quite a hit from COVID-19, even though the measurable cost has been obscured by the long-term nature of office leases. As of April, the U.S. office vacancy rate climbed to 15.9 percent, up 280 basis points year-over-year, while sublease space has more than doubled during that time, according to Yardi Matrix.

That bump, however, is just the tip of the spear. Only about a quarter of downtown office workers nationally reported to an office last month, with the percentage closer to 15 percent in New York City and San Francisco, according to security firm Kastle Systems. The growth of work-from-home has made going to an office optional for many firms. The question is not whether office tenants will reduce their footprints, but by how much.

The Centers for Disease Control’s new guidance that fully vaccinated individuals no longer need to wear masks in most indoor situations added another potential twist to the issue of returning to the office. Though that announcement appears to open the door wider, a host of other issues are in play.

Demand for space merely scratches the surface of the considerations facing owners and occupiers. The industry must come to grips with a host of factors, including when workers can safely return; how many people will use offices and how often they need to be there; where offices should be located; how offices interact with lifestyle preferences, such as commuting and walkability; how to re-design space to attract and maintain talent while meeting functional needs; and how to accomplish all this while dealing with mandates to improve energy efficiency and cut greenhouse gas emissions.

The industry is facing a “quantum fundamental shift,” said Jeff Adler, vice president of Yardi Matrix, during a Yardi-sponsored webinar last week. “The sector is at the beginning of a wrenching multi-year rethinking of the nature of work,” he observed. “Everything is in play.”

Where to work?

The percentage of workers reporting to an office is expected to triple to 75 percent by year’s end, said Benjamin Breslau, chief research officer at JLL, speaking last week on a panel at the Urban Land Institute’s virtual spring conference. He predicted work-from-home will double from pre-pandemic levels to 20 percent of workers. Daniel Ismail, a senior analyst at Green Street, said at another ULI panel that the average worker’s weekly time in the office will likely drop from 4.5 days before the pandemic to 3.5 days.

Many companies have found that workers can be productive from home, but to what extent can it be done without impacting corporate culture and collaboration? And to what extent does it affect the ability to retain workers and keep them happy? “Every tenant is asking the same questions about how and when to get back,” Breslau said.

A consensus has formed around the idea that most companies will adopt more flexible arrangements, but what that means for demand depends on the details. In terms of how much space is needed, there is a big difference between giving employees a choice to be fully remote and requiring them to be in an office part-time.

The primary question hanging over the industry is how office utilization will change after the pandemic ends. Decisions are complicated not just by employee preference but by the nature of the job and the industry. Some types of knowledge work (such as programming) can be performed well anywhere, but others benefit significantly from a collaborative environment. “Companies in the same industries will have a wide divergence,” Ismail said.

While a part of the office space decision will be driven by the type of jobs and corporate culture, companies will also have to consider another complex issue—employee preferences. If proximity to an office is no longer as important, how will that change workers’ preference for where they want to live? In the years leading up to the pandemic, the default assumption was that young knowledge workers wanted to live in an urban environment. Job growth over the last 20 years has been concentrated in urban areas, even in secondary and tertiary metros.

However, the pandemic prompted a drop in population in the urban submarkets of gateway metros. Young families moved to suburbs to get more space while others who were suddenly unmoored from the need to commute relocated to different parts of the country. Reducing the cost of housing was the main priority for some, but part of the trend was driven by the closure of entertainment and cultural venues that make cities appealing, particularly to young workers. When those attractions re-open, some former residents will return, but others have left permanently.

Occupants could adjust by shifting offices to the suburbs, moving to less expensive metros, or adopting a hub-and-spoke model with a city headquarters and suburban outposts. Mark Grinis, hospitality and construction leader at EY Global Real Estate, said at the ULI conference that a more distributed workforce is at odds with the need for collaboration. Studies conducted by EY found that secondary locations—the “spokes”—had the worst workplace productivity performance.

As a result, Grinis commented, companies must tailor workspaces to the particulars of their workforces. “If I invest time when I go to the office, I want the best experience out of that,” he said. Often central business district locations “are best able to take advantage of that.”

Lifestyle changes

COVID-19 has prompted many people to think about lifestyle and where they want to be. Many workers were relieved to avoid long commutes, but walkable neighborhoods with access to shopping and other amenities remain popular. Diane Hoskins, co-CEO at Gensler, observed that many workers are choosing smaller cities and inner-ring suburbs, especially in the technology sector.

“There’s a real appetite for reconsidering how cities work,” Hoskins said. “When you look at real estate as an investment in people, you say how do you do it in a way that optimizes … competitiveness to be able to thrive in a global environment.”

One difficulty in picking a location is that few metros are configured to meet conflicting worker preferences. People want more space, but they also want to commute less and be close to shopping and other amenities. That presents challenges to employers looking for optimal locations.

Lifestyle considerations mean that office buildings must be re-thought to meet the new paradigms. For example, workers may demand less density for health reasons. If workers come to the office less frequently, then more collaborative space is likely needed to efficiently use the time they are present.

That means occupants may have to redesign space to add amenities to retain workers or entice them to come to the office. Myriad redesigns and even downsizing, are likely to require costly capital expenditures at a time when asking rents are flat or declining due to declining occupancy and competition from new stock. More than 160 million square feet of space is under construction, according to Yardi Matrix, with a large amount of deliveries expected in New York City; San Francisco; Austin, Texas; Charlotte, N.C.; Boston and other metros.

Yardi’s Adler noted that companies must be purposeful about office design rather than following the traditional model in which employees are in one spot by default. “Companies have to decide, ‘Why are we in the office, what do we want to accomplish?’” he said.

Creating amenity-rich space and leasing flexibility seems suited for growth in coworking, although the coworking industry was hard-hit by the pandemic; the core business model—leasing large blocks of space and re-leasing at higher rates to small tenants—proved unstable when offices were mostly closed. Coworking will increasingly take a new form, one in which office owners partner with service providers to create flex space that is leased short-term and to smaller tenants.

Metamorphosis coming

Transformation of the office market will take several years, as existing leases mature and companies discover what employees want and what kind of space changes prove successful. One thing seems clear: There will be no one-size-fits-all model. Some jobs can be done productively remotely, others require in-person collaboration at least part time. Workspace design solutions will vary widely by employee demographics and the requirements of each job.

However these issues shake out, office occupants will reduce space needs; the only unknown is how much. Some of the reduced demand will be made up by job growth, but that factor will be balanced out by the tremendous influx of new supply. The result will be thinner margins, an increase in distressed debt, and probably lower property values, at least in some markets. Office owners and tenants will have no choice but to take a hard look at how to adapt for the future.

The stakes are high for employers because office space decisions impact human capital. Green Street’s Ismail noted that firms on average spend five to 10 times more on employees than they do on renting space. That means improving worker productivity and reducing turnover have a bigger impact on profitability than reducing the office footprint. “You don’t want to risk dollars to save pennies,” he said.

You must be logged in to post a comment.