Medical Property Investments Rising in Popularity

By Toby Scrivner, Stan Johnson Co.

While medical properties represent an appealing investment option for many, including net lease property buyers, underwriting these assets appropriately requires a somewhat different approach than what is used for the traditional triple-net building.

By Toby Scrivner, Director, Stan Johnson Co.

Medical office buildings and other health care-related properties have been growing in popularity with many investors, and for good reason. Housing what is already one of the largest growth segments of our nation’s economy, tenant demand in medical real estate space is only going to grow for decades to come as the baby boom generations ages, not to mention the 30 million or so previously uninsured Americans who are expected to access the health care system due to recent healthcare reform legislation.

But while medical properties represent an appealing investment option for many, including net lease property buyers, underwriting these assets appropriately requires a somewhat different approach than what is used for the traditional triple-net building.

Too Narrow a Focus?

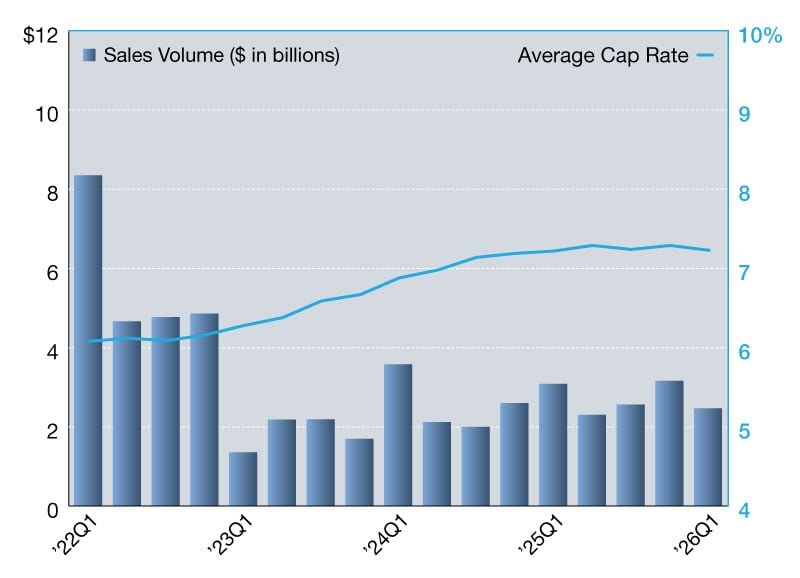

In the past 12 months alone, Stan Johnson Co,’s healthcare property market experts have brokered 20 healthcare real estate transactions totaling more than $153 million, involving a variety of healthcare facilities around the country and buyers ranging from the individual to the institutional. Our experience has shown that often the biggest challenge most net lease investors have when analyzing healthcare assets is that they are too narrowly focused on the price per square foot and what the prospective replacement use or tenant might be.

We believe that is a mistake. The price per square foot, while in many cases it may seem unusually high relative to standard office or retail properties, is due to the very high grade of finish-out these properties inherently have (for a building with a surgery center, for example, final construction costs of more than $400 per square foot are not uncommon). While construction costs have actually decreased over the past 18 months, costs will inevitably increase over time. As reimbursements for services are reduced, profit margins for hospitals and physicians will be strained, thereby making the higher cost of occupancy associated with new construction a significant hurdle to the construction of new facilities in the future. It is easy to imagine how the replacement cost of a medical property could indeed be quite high, much higher than current acquisition prices. And in terms of replacement or alternative use, given the growing demand for these properties, another medical tenant would be the logical new user.

Characteristics of Success

So what makes a good medical investment property? One primary characteristic is a successful practice group that has an operational history—making it not only a stable tenant, but also a prime candidate for acquisition by a hospital—or an entity that already has ties to or an affiliation with their local hospital. It is also helpful to look at the average age of the physicians in the practice. Is it an older group that is in need of bringing in new blood? If the practice group is not actively recruiting new physicians, then there is a greater likelihood that as the physicians retire, the practice will not see the same level of success that it has in the past, and therefore not continue to be a viable tenant in the future.

In terms of evaluating creditworthiness, one key metric to focus on is how successful a practice has been in relation to what they’re generating from an earnings before interest, taxes, depreciation and amortization (EBITDA) standpoint, and how that relates to their cost of occupancy. The higher the EBITDA relative to their cost of occupancy, of course, the better. For an ambulatory surgery center, for example, we would typically look for in excess of four times rent coverage; for a rehab hospital or an long-term acute care property, we would look for an EBITDA to rent coverage of three times from a seasoned operator.

If the tenant is a hospital, or a hospital system is guaranteeing the lease on a facility, then the creditworthiness of that particular hospital system naturally comes into play as well, not just in terms of acquisition price but also in terms of the cost of and ease of securing debt financing. When evaluating a hospital leased property, look at the amount of revenue the hospital is generating, but also pay attention to other financial indicators, the number of Days’ Cash on Hand, Operating Margin, and the ratio of assets to liabilities. Understand the tenant’s market share relative to their competition. By understanding these dynamics an investor is able to better gauge the long-term viability of the real estate.

Location, Location, Location

As in all real estate, location is key for medical properties, too. For example, the more proximate a medical office building is to the hospital campus, the lower the cap rate it will command (sometimes as much as a 100 basis point differential in the cap rate). If an asset is on a hospital campus, the investor essentially has a moat protecting the investment, and it is considered especially prime real estate if there is no additional land around the hospital to be newly developed. With an on-campus property, even if you were to lose one particular doctor group, the likelihood is extremely high that either the hospital itself or another practice group will want to lease that space because of its proximity to the hospital.

The age of the facility—both the building itself but also the equipment and finish out inside—is likewise an important factor. Technology changes very rapidly in the health care sector, a fact that doesn’t apply so much to clinical space as it does to facilities like operating and procedure rooms. With an older facility you do have to pay attention to the possibility of functional obsolescence. This reinforces the critical aspect of being on a hospital campus, as well. A freestanding building built in the 1980s with no affiliation to a hospital, for example, could easily be considered functionally obsolete and thus the cost of building a new facility justified; but if the facility is on a hospital campus the land is likely irreplaceable, and thus the cost of updating the finish-out is in fact justifiable.

In addition to appropriate real estate and tenant underwriting, at Stan Johnson Co., we believe when considering a medical property investment it is also wise to understand some of the basic trends taking place in our healthcare industry. The days of the solo practitioner physician are virtually gone; instead, young physicians today either seek to align themselves with a large and established practice group or become employees of hospitals. Meanwhile, the current environment for healthcare providers is one of increasing mergers and acquisitions activity—it doesn’t take a long search of recent headlines to find numerous examples of larger healthcare systems buying smaller, one- or two-hospital systems, as well as of hospitals buying large physician practice groups.

This climate of M&A activity is expected to continue for the foreseeable future as hospital systems seek to establish increased market share, and it will prove to be a very positive development for real estate owners. As hospitals acquire physician practices, for instance, landlords often see an enhancement to the tenant credit by virtue of the hospital taking over the practice’s lease obligations. In addition, where practice groups own their real estate, an increase in sale-leaseback activity is expected as the hospital systems seek to fund a portion of the cost of their new acquisition. This activity will likely increase the number of properties available in the investment market and boost the credit profile of the typical tenants in these buildings as well— both of which are encouraging developments considering the growing demand from investors of all stripes for these assets.

You must be logged in to post a comment.