How Much Are Office REITs Weighing Down the Sector?

CEOs, investors and analysts shared insights about the market and individual companies at Nareit's annual REITweek conference.

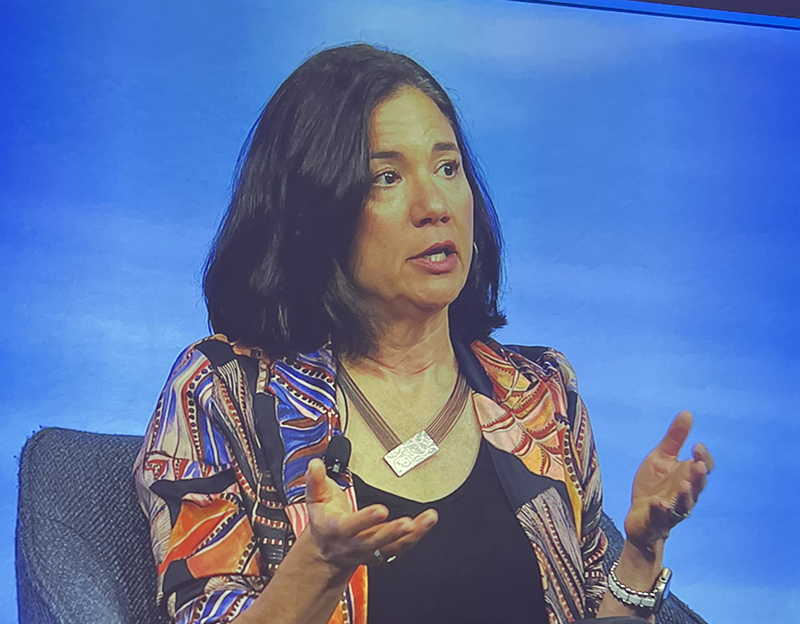

Lisa Kaufman, Head of Global Solutions, LaSalle Investment Management

With REITs currently trading at a steep discount, this would seem like the ideal time for buyers to increase their holdings of these companies. After all, REIT portfolios are representative of the country’s best commercial real estate assets, and these firms are well governed.

However, REITs give analysts and investors a lot of pause right now—thus the low stock prices. This week, for example, Fitch Ratings reduced its 2023 U.S. REIT sector outlook to “deteriorating from neutral,” citing tighter lending conditions, and pressures on valuations and fundamentals due to high interest rates and worsening economic conditions.

Nevertheless, REIT CEOs flocked to New York this week for the chance to promote their companies and the asset class, in general, at Nareit’s REITweek conference.

“REITs provide an attractive buy opportunity,” said Lisa Palmer, Regency Centers Corp. president and CEO and the moderator of the conference’s opening panel. “Public investments adjust before private investments, and that is what we are seeing today.”

Palmer’s panelists did not share her exuberance for several reasons, including the pending recession. Green Street Advisors is predicting declines in GDP growth for the third and fourth quarters—roughly 1/2 percent growth for the third quarter and slightly above zero for the fourth, said Dirk Aulabaugh, global head of advisory.

But two consecutive quarters of low GDP growth is not the most worrisome indicator for Green Street—that condition has existed before without a recession. More concerning, Aulabaugh said, is weakening consumer spending since it “represents two-thirds of the economy.”

“That’s a big factor in determining whether we go into a recession or not,” he added.

LaSalle Investment Management has been putting the assumption of a recession into its REIT cash flow estimates since the third quarter of last year, said Lisa Kaufman, head of global solutions. Kaufman also stressed the impacts of the credit crisis, which is limiting REITs’ access to capital and transactions. Bank lending dropped 20 percent between February and April, according to Fitch. “More importantly, that capital is more expensive,” she said. Office REITs have an “acute” liquidity problem, she added.

Let’s Talk About the Office

Office REITs have a lot of issues, actually. The cost of capital in the face of maturing debt and a scant transaction market are compounded by low utility rates and doubts about the asset class’s long-term future.

So it is not that surprising that office REITs have been trading at a steep discount to NAV. According to S&P, all REITs ended May at a median 23.3 percent discount to their consensus estimates for NAV per share, while office REITs were trading at a 57.7 percent discount. But it is somewhat surprising that , industrial (8.5 percent discount), residential (15.3 percent discount) and shopping center REITs (29.3 percent discount) are also trading down consider their relative strength during the current circumstances. “Those values should not be down,” Kaufman said.

REITs are definitely suffering from “sentiment contagion,” as the market generalizes pessimism about the capital markets and problems with the office market, observed JP Morgan Chase & Co. Managing Director Mark Streeter.

“Office is less than 3 percent of the NAREIT index, but look at the impact,” he said.

REITs have top-quality assets going for them, and they will have better access to capital at better rates when certainty returns to the financial and real estate markets. “REITs are going to come out running,” Streeter said. “We just have to get to the other side.”

Streeter cautioned, however, that while REITs are trading at a big discount to the private market—and, therefore, look attractive—they don’t look as cheap compared to other investments.

Brookings Institution Fellow Tracy Hadden Loh also warned of the serious implications that negative “vibes” can have, not just on commercial real estate, but on cities and the affordable housing crisis.

“I’m super worried about overall uncertainty leading banks to conclude that risk is in the air, and they shouldn’t invest or that they are already over their skis,” she said.

By the way, Loh is bullish on office and cities in general. She believes there will be more “RTO” (return to office) and that cities are recovering from the pandemic at different rates. Cities that shut down early and stayed shut down longer, such as San Francisco, are taking longer to recover, she observed. Cities that shut down for only a short time, such as Atlanta, are bouncing back faster.

So, what’s a REIT to do? Privatizations are currently not a viable option, considering where share prices and property values are, and because such transactions may require debt, Streeter noted. And he is not worried about REIT prices sinking dangerously low. “No one ever stole a REIT,” he said.

We may, however, see public-to-public (or “share-for-share”) mergers because those transactions would involve relative capital vs. actual capital, Streeter added.

You must be logged in to post a comment.