How Far Will You Go for Yield?

In the search for higher CRE returns, the appetite for risk is growing.

Are commercial real estate investors willing to move up the risk curve in 2026? As fundamentals have rebounded off the bottom across a number of property sectors, conditions suggest that chasing a little more yield is worth consideration.

Interest rates have ticked down and largely stabilized over the last several months, making value-add plays more feasible in high-demand sectors with flat or declining new supply, such as industrial and retail. Meanwhile, office remains fertile ground for bargain hunters, but more workers in seats more days of the week are recapturing the interest of institutional investors.

“There are a number of factors that have helped the market get to a better place and are facilitating higher-return investing,” said Richard Kleinman, CIO for the Americas at LaSalle Investment Management. “I don’t think we’re going to see an overwhelming tilt toward higher return opportunities, but I think they’re at least gaining favor.”

About two years ago, for example, core investors were focused on buying new industrial assets at below replacement cost amid the higher rate environment, overbuilding and slowing absorption, Kleinman pointed out. But that’s no longer the case as prices for stabilized core properties have returned to above replacement cost.

As a result, interest across the risk spectrum—core, core-plus, value-add and opportunistic—have largely balanced out, a situation helped not only by the decline of the short-term cost of capital but also by the resetting of land prices, he added. Among other industrial deals, JLL Income Property Trust, a nontraded real estate investment trust advised by LaSalle, in September purchased the 985,000-square-foot West Raleigh Distribution Center industrial park in North Carolina for $190 million.

But whatever strategy the firm pursues is ultimately dictated by the goals of the investors in its funds, which cover the risk spectrum. “We try to cast a wide net and find the best risk-adjusted returns across a broad set of markets within a given return profile,” Kleinman said, “whether that’s core, value-add or opportunistic.”

Liquidity-minded

For some opportunistic investors, 2026 could be as fruitful as the past few years, as some property owners continue to struggle in the aftermath of spiking interest rates and declining asset values. Stockdale Capital Partners, a real estate investment firm focused on equity and credit strategies, is focused on turning around distressed or underperforming assets and owns and operates some $4 billion across a handful of property types.

Key to its investment decisions is its hold period of four to six years to buy, fix and sell projects, shared Dan Michaels, a managing partner at the firm. The strategy also requires confidence that investor demand on the back end will support an exit that fulfills its time horizon and return goals. For those reasons, Stockdale has been targeting sectors such as retail and medical office with the underlying conviction that core funds and REITs returning to the market will be buyers.

In February, Stockdale partnered with UBS’ recently launched Unified Global Alternatives real estate investment platform to recapitalize the Shops at Northfield, a 1.1 million-square-foot open-air retail center in Denver. Stockdale acquired the neglected property in 2021 and has signed some 350,000 square feet to new tenants, including Lululemon, Sephora and Nike. It’s also filling former department store boxes with a Wayfair store and Life Time gym, and has secured entitlements for 1,500 multifamily units at the site.

Some of the liquidity challenges in the prior year are easing up, and investors are able to look for bigger investments.

—Jay Johnson, Principal & Leader of Healthcare Real Estate Services, Avison Young

“The retail property stock, particularly lifestyle retail, is old, and there’s a huge opportunity to reposition the centers with today’s brands,” Michaels commented. “It creates higher trip counts and a better result for the surrounding community.”

A dearth of new retail construction over the past several years is only buoying demand for shopping center assets, reported Todd Stender, a managing director with LNL Capital, a provider of structured debt and equity financing to net-lease investors. That’s particularly the case for grocery-anchored centers, where traditional core investors have shown a willingness to pursue core-plus and value-add strategies.

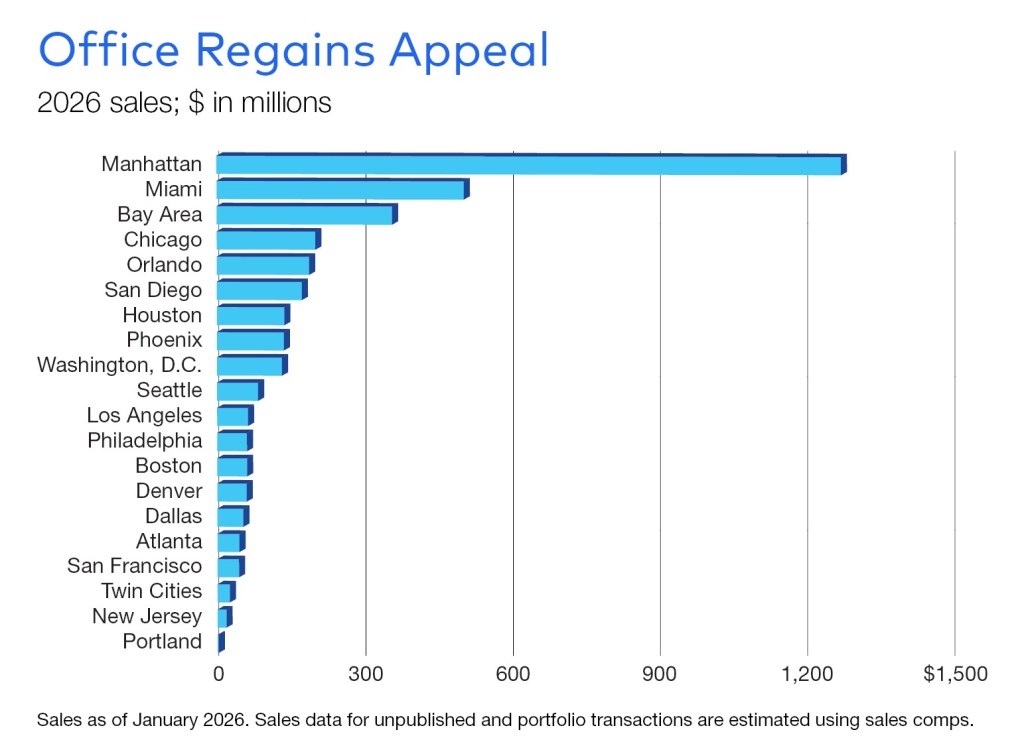

Office extremes

One of the biggest questions in 2026 is how much risk investors are willing to take for office buildings. Prices paid for offices last year ranged from pennies on the dollar in Chicago to premiums over pre-pandemic values in Miami, Dallas and other markets, according to Yardi Matrix. Stockdale has pursued office assets in the past, but the opportunistic investor currently has limited interest in committing equity to the sector today because of shifting buyer demand.

“If we were a family office and could sit on assets for a decade, the past couple of years would have been an interesting time to start making some office bets,” Michaels said. “But that doesn’t work for private equity with shorter time horizons. You have to be cognizant of the asset classes that give you an opportunity to step in, make an impact and then find liquidity.”

While dynamic, the office market recovery remains bifurcated along building quality and submarket lines, according to Patrick Gildea, co-head of office capital markets for CBRE. Capital is seeking out markets with strong fundamentals, which include New York and cities in the Sun Belt, and Gildea is seeing a willingness among investors to go a little beyond their comfort zones.

“Many investors are beginning to expand out on the risk curve, focusing on assets that may be ‘one step down’ in terms of location or quality in anticipation of the market’s continued recovery,” he reported. “The quality and quantity of capital is the highest we’ve seen in five years, with many traditional institutions returning to the sector. That said, these institutional investors are highly selective.”

Like Michaels, Kleinman takes a cautious view of the office market, but for a different reason. He suggested that in some cases, prices have moved too quickly. “What we’ve seen in some markets is that prices are already too firm for us to justify. Investors have shown that they’re willing to pay up in markets like New York, Miami and San Francisco.”

Going big

Meanwhile, investors are showing more interest in medical office buildings, an alternative asset class that is benefiting from health care providers who are refocused on growth and the aging population, observed Jay Johnson, a principal & leader of healthcare real estate services for Avison Young. Many are looking for value-add opportunities and are pursuing portfolios vs. single assets, he added, which is a change from the recent past and is contributing to a price premium.

“Some of the liquidity challenges in the prior year are easing up, and investors are able to look for bigger investments,” Johnson said. “There’s also more fluidity in the market in terms of what’s available today and what’s going to be available moving forward, which is leading to increasing activity, too.”

You must be logged in to post a comment.