CREFC Special Report: Trump Era Mix of Optimism, Uncertainty in CMBS

While industry executives are generally optimistic about the upcoming year, Commercial Real Estate Finance Council speakers revealed that uncertainty remains as the market prepares for a slew of changes brought on by the Trump administration, reports Yardi Matrix Associate Director of Research Paul Fiorilla.

By Paul Fiorilla, Associate Director of Research, Yardi Matrix

A year ago, CMBS market players were debating how much new regulations requiring issuers to “eat their own cooking” would disrupt the industry.

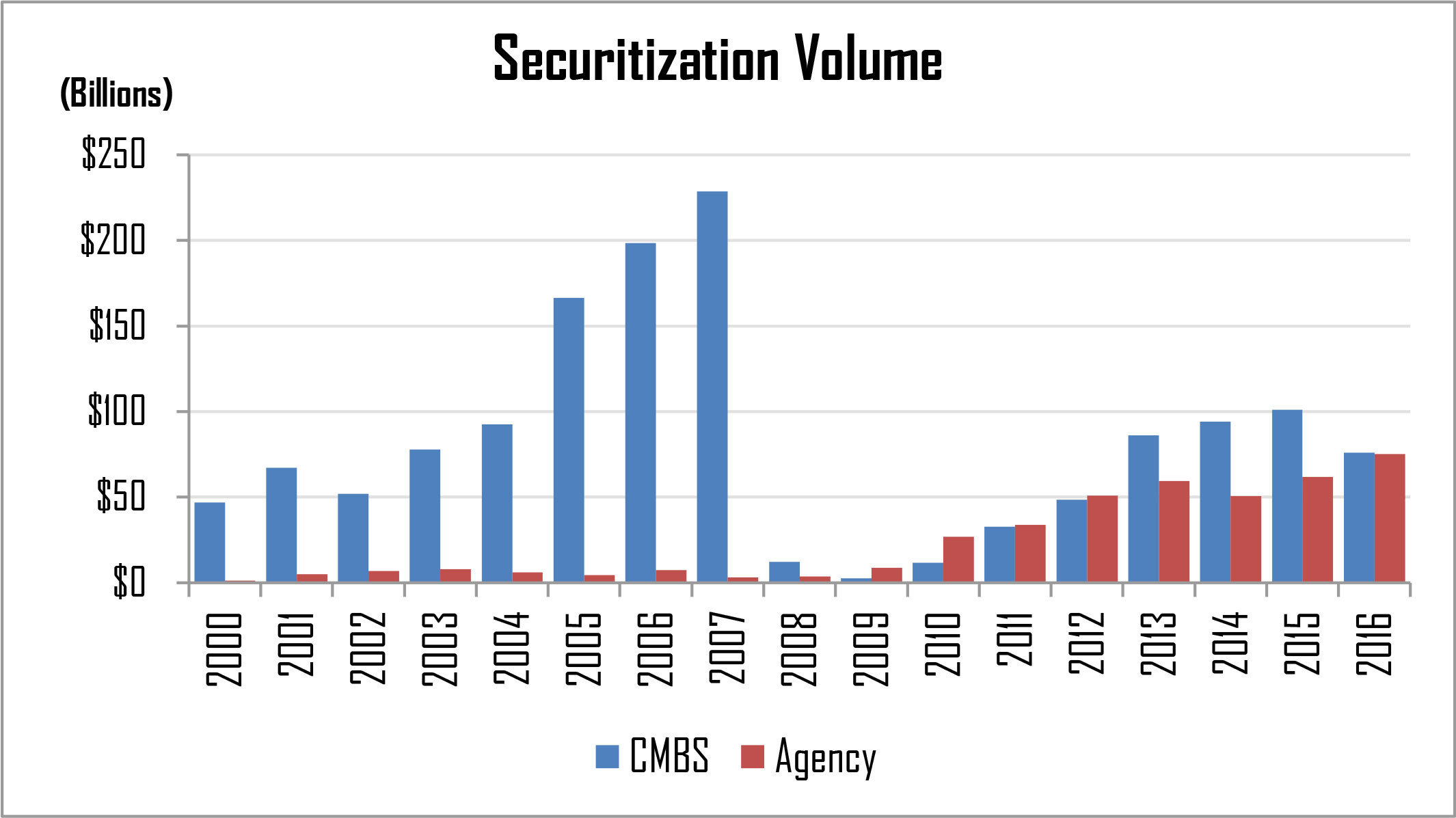

Source: Commercial Mortgage Alert

Although risk retention proved not to be the negative force envisioned, the regulatory environment is still the dominant theme of the commercial mortgage industry as the market prepares for a slew of changes brought on by the Trump administration. While specific policies remain unclear, there is almost certainly going to be not only a rollback of rules affecting lenders but also less stringent enforcement overall.

Industry executives–speaking at last week’s Commercial Real Estate Finance Council annual investors’ conference–are generally optimistic about the upcoming year. The prospect that the Trump administration will reduce the regulatory burden on banks could produce more lending activity, while at the same time economic growth and demand for commercial real estate are expected to be strong. Clouds to the outlook come from uncertainty due to the fact that policy affecting the industry is not expected to be on the front burner and won’t get resolved soon. Plus, there is the worry about the effect of the new president’s style, which one executive referred to as watching “Government Apprentice.”

Risk Retention Rules

Rules that require issuers of securitizations to hold 5 percent of the securities issued–part of the Dodd-Frank Act that was passed in the wake of the last financial crisis–finally went into effect at the end of December. While it turned out not to be the cataclysmic event that had concerned many in the market, a host of questions remain.

One question is how much of Dodd-Frank will be repealed by the GOP-led Congress. Industry players anticipate that any regulatory changes will take months (or possibly a full year), and it’s unclear how much of the law will be rolled back. Another question is what form of risk retention will come to dominate the industry. The basic types of deals are vertical (in which the issuers hold 5 percent of each class), horizontal (in which the junior 5 percent is sold to a third-party “B-piece” buyer) and L-shaped (a combination of the two).

The first deal to be issued in compliance with the law used the vertical structure, and it proved popular with investors. However, it succeeded in part because the issuing banks structured the deal in a way that provided favorable accounting treatment for the retained collateral, and regulators have not yet ruled whether they will allow that treatment. Plus, not every bank wants to or has the resources to retain bonds. Vertical structures are most useful to money-center banks with big balance sheets.

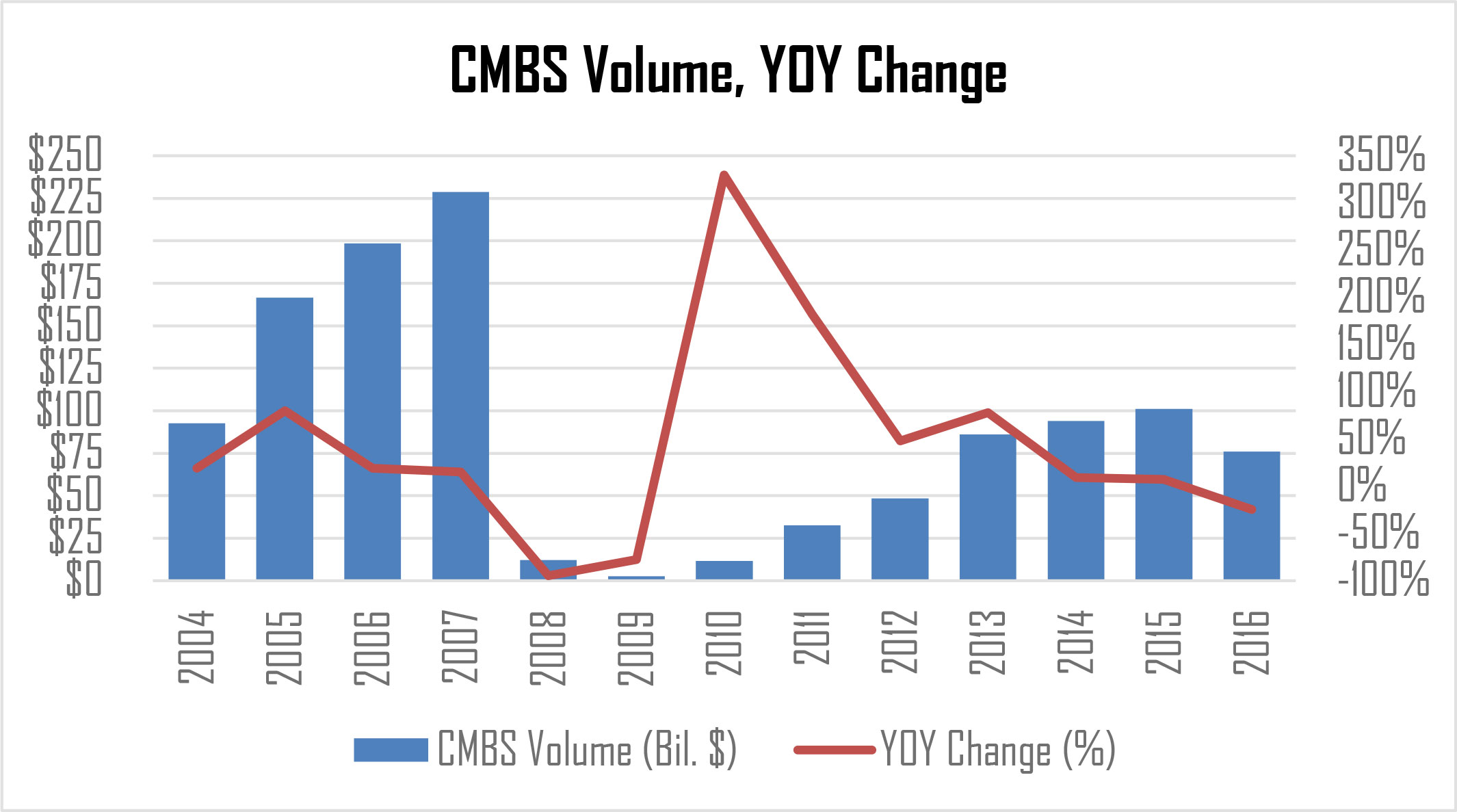

Source: “Commercial Mortgage Alert”

The horizontal structure is similar to the traditional CMBS model in which a B-piece investor buys the most junior classes. However, the B-piece investors bought a smaller chunk of the deals, about 2 to 3 percent, focusing on the lowest-rated bonds that will produce a return in the mid-teens or higher. The number of investors willing to buy the entire 5 percent strip might be limited. The horizontal structure also creates compliance risk for banks. The holders of the 5 percent strip are not allowed to trade it for five years, and it’s not clear how the bank that sells the bonds can enforce such a covenant or what the penalty is for non-compliance.

Over the next few months, issuers are expected to float CMBS with a variety of structures. How those deals perform will determine in which direction the market is likely to go. Some CMBS executives believe that one structure or another will eventually prevail (there is no consensus on which), while others believe there will be a period with a variety of structures that will enable issuers and investors to pick and choose.

One thing that is clear is that the market has largely accepted risk retention, and few remain worried that it will create a major dent in the industry. Even if they don’t approve of mandates, issuers have spent a considerable amount of time and resources to create the structures to comply with the law, and they have found that investors are willing to pay higher prices for compliant deals. “I actually think it will create a more stable market on a long-term basis,” said one investor, speaking on a panel at CREFC. “We’ve seen (risk-retention compliant) deals tighten in pricing, so maybe the overall cost won’t be so high.”

There’s also a thought that risk retention has kept CMBS loan quality high at a time in the cycle when standards might otherwise start to slip. “The market has imposed discipline on itself better than it has in the past. Credit is generally strong,” said one executive at a specialty lending firm. “It’s not like it normally is at the tail end of a cycle, when everything is falling off a cliff.”

Liquidity, Tax Concerns

Liquidity is turning out to be a much larger concern for the overall health of the CMBS market. A rule that is being considered by the Comptroller of the Currency, FDIC and Federal Reserve would set a Net Stable Funding Ratio, which would require large banks to set aside more capital including equity, credit facilities and deposits for holdings such as CMBS.

The upshot is that it would cost banks more to hold structured products on balance sheets—something that has already reduced the amount of trading. The reduction in banks’ “market-making” function has the effect of reducing liquidity in a market at a time when it is needed, as investors are already dealing with so many unknowns.

One of those unknowns is tax laws. While details of tax policy won’t be revealed until the new administration’s cabinet is in place, major changes are expected. Generally speaking, lower rates and more simplified structures are thought to be benefits to business, and by extension, the real estate industry. However, there are rumblings about the possible repeal of tax laws that specifically benefit commercial real estate, including the deductibility of carried interest and the 1031 exchange, which enables investors to defer paying taxes on capital gains if they buy a similar property. Eliminating 1031 exchanges would potentially reduce property sales and associated financings.

Sunset for Enforcement?

Whatever the actual changes are to policies and regulations, there will certainly be a shift in the way regulations are enforced, since people predisposed against restrictions on business will be leading the agencies. Regulations are written very broadly, and it is up to career staff to interpret them. How they do that will depend on the direction in which the agency heads.

Take, for example, the regulations on banks writing High Volatility Commercial Real Estate loans (HVCRE) that have been in effect since 2015. HVCRE requires banks to set aside 50 percent more capital on construction loans than on permanent loans, which has helped to limit the amount of commercial development and has increased the activity of alternative lenders. Market players note, however, that what constitutes a construction loan is not so simple. Does the rule apply only to ground-up construction or also to projects that involve some amount of redevelopment? How career staff at an agency interpret such a rule could have major implications for how the market operates.

“Policy changes may be initiated by Congress and adopted by the political appointees at the agencies, while supervision of the regulations is largely decided by career regulators,” said Christina Zausner, vice president of industry and policy analysis at CREFC.

Change Is Certain; Uncertainty Results

The year has started off with a great deal of optimism in the market. There had been concerns about how much longer the economic recovery could be extended, but the election has alleviated many concerns about growth slowing down. And while there is also optimism about how the easing of the regulatory burden will impact business, there are concerns that the market will be operating in the dark for a time about specifics, not to mention the geopolitical landscape in the Twitter age.

As one executive put it: “Our expectation is that the next four to eight years we’ll see a lot of unexpected events happening repeatedly.”

You must be logged in to post a comment.