Capital Returns to Work in Industrial and Office

There is no shortage of lenders to meet industrial borrowers’ financing needs while office deals get plenty of interest, too.

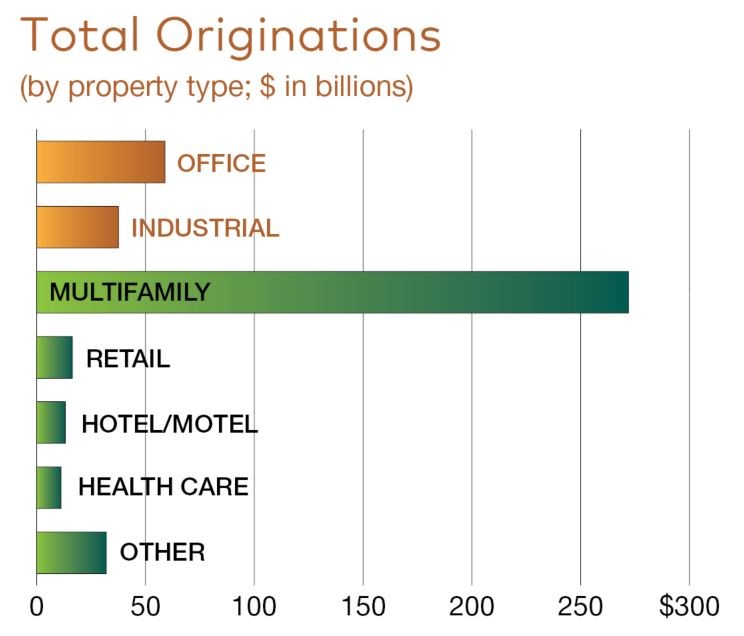

Industrial borrowers seeking financing in 2021 will be met with a full array of options from all lender types—life companies, CMBS, banks and debt funds. The debt markets are flush with capital seeking industrial deals first and foremost, but even some office deals are selectively getting done.

Despite working remotely, CBRE’s Los Angeles Capital Markets office is busier than ever since COVID-19 struck, according to Executive Vice President Val Achtemeier.

That’s largely due to strong borrower demand, and a very “robust” liquidity environment for industrial assets.

“We’re seeing the industrial sector really be a point of strength in the capital markets both in terms of financing and in terms of investment sales,” Achtemeier said. “It just depends what the borrower’s appetite is in terms of loan-to-value and whether they want to go fixed-rate or floating-rate debt.”

Originators report that spreads for both fixed-rate and floating-rate loans also remain very tight with lenders stretching to win highly coveted deals and a consistent deep bench of quality quotes. Even for construction loans, liquidity and pricing has improved dramatically for industrial developments in the last year–for both speculative and preleased projects.

Against the backdrop of LIBOR hovering around 11 to 12 basis points, compelling spreads, and the fact that most floating-rate loans no longer have any sort of a LIBOR floor, many borrowers are opting for floating-rate options that are available in the market.

Hedging costs are quite reasonable, there’s prepayment flexibility and the low index rate enhances cash-on-cash returns, Achtemeier noted.

At the top of the heap, however, are portfolio loans that offer desirable scale and diversification because they tend to get best pricing and strongest depth of quotes, according to Achtemeier.

The industrial sector is a bright spot in the debt market and most lenders are trying to increase their exposure to industrial.

Everybody in the pool

CMBS lenders, many of the banks and life companies, which are traditionally focused on core fixed-rate loans, have been competitive and have a strong appetite for floating-rate industrial mortgages.

The fixed-rate market, according to sources, is also white-hot for industrial borrowers with spreads varying from a low of 100 BPS to about 140 BPS, depending on risk profile and LTV. The pricing is incredibly tight with the 10-year Treasury at 1.58 percent, 10-year money is typically 2.75 percent to 3 percent and 5-year fixed-rate money prices around 2 percent for most deals.

Brian Linnihan, executive director in the Equity, Debt & Structured Finance practice with Cushman & Wakefield’s Atlanta office, says the lower cap rates make it harder to push leverage.

“For the new-built industrial product that’s going for low-fours caps at 60 percent leverage, that’s going to be a pretty tight debt yield going in,” he noted.

Stable, well-leased industrial is generally seeking and getting leverage in the 55 percent to 60 percent range. But capital is also seeking under-leased industrial.

Linnihan’s team, for example, has worked on 30 percent leased industrial with the debt funds, life companies and even banks, though that type of deal has typically fallen in the debt fund category and life companies occasionally. Cash flow and debt service coverage ratios are dictating whether or not banks are interested.

Because industrial is fairly binary, meaning one or two tenants, it’s either fully leased or it’s not. Older industrial properties with shallower bay tenancy, depending on lease-up, are attractive to banks, life companies and debt funds.

Much of the older industrial located in infill locations is being absorbed by industrial users for just-in-time delivery, Achtemeier noted.

Office work

And while every lender wants to be in industrial, they are not shying away from the office sector nor are they requiring the COVID-19 reserves seen in the multifamily sector.

Post-COVID, Cushman & Wakefield’s Atlanta office, which covers the Southeast, has closed or is marketing approximately 24 office deals across product types from Class A to Class B and from refinance to acquisition.

As corporations begin returning to the office, lenders are getting more comfortable with the idea of making office loans.

Despite growing liquidity for office, it has not risen to the pre-COVID-19 watermark, Linnehan said, with the hardest office deals to close involving vacancy or near-term rollover of leases.

On the other hand, office product with a good weighted average lease term, and whether that comes with or without vacancy, is being bid robustly, he said, adding that the pricing on this product is even more robust than before COVID 19.

The Atlanta office, for example, is closing an office deal in suburban Miami across from the airport. It was, Linnehan said, “one of the hottest deals we’ve probably marketed ever.”

The 70 percent leased building was financed by a debt fund with better pricing than before COVID-19.

Lenders, originators find, are not asking for additional pandemic reserves in office or industrial, but they are now asking a couple of new questions upfront. When marketing a deal, the first question a lender asks is what collections were like during COVID-19 and if any tenants requested relief, if relief was granted, and in what form.

The next question is about subleasing. Even so, Linnihan said, regardless of the answer to the pandemic-related questions, lenders have never declined to quote a deal.

New kids on the block

With so much competition among traditional lenders, new entrants into the market are getting creative.

Quick Liquidity is a niche direct balance sheet lender, lending anywhere between $20 million and $30 million annually. Yoni Miller, co-founder of QuickLiquidity, says he focuses on niches to cut out the competition.

One niche area he hopes to do more business in is debtor-in-possession lending in bankruptcies, where a borrower might need rescue capital, money for converting properties, and value-add lease-up.

“We would like to do the more traditional bridge products, but that space is honestly very competitive,” Miller said.

QuickLiquidity closes a loan using its balance sheet and then syndicates typically 80 percent of the loan out to accredited investors, typically high-net-worth individuals, and keeps 20 percent of each deal on its balance sheet. It also takes passive equity as collateral, meaning QuickLiquidity is not on the title but receives a pledge of ownership in a syndication or partnership.

Janover Ventures is a number newcomer that offers a portal matching borrowers with an array of roughly 25 lenders, much like a Rocket Mortgage, except for commercial real estate. The company acted as an online intermediary for almost $200 million, mostly small multifamily loans.

The company mines borrowers for multifamily acquisitions using Google, various websites it own, and dozens of other sites that draw borrowers into its funnel, where they are screened and matched with a lender within three-and-a-half minutes on average. Loans can be small or go as high as $20 million. As markets reopen, Janover hopes to more than double last year’s volume in 2021.

“We’re seeing last-mile industrial and cold storage continuing their strong run, in many cases trading even more attractively (for sellers) than multifamily,” Office remains a challenge,” said founder & CEO Blake Janover. “Single-tenant with long leases in large markets remain un-dinged, but everything else has been pretty well hammered unless you’re in a market that has been at the receiving end of the migration from urban and tax-heavy markets (think NYC to Miami and San Fran to Austin).

You must be logged in to post a comment.