Busy Ports Support Industrial Market Recovery

Despite tariff uncertainty, activity set a new record.

Port activity in North America, especially top U.S. ports on both coasts, remained a prime driver of industrial space demand in 2025 despite volatility induced by tariff uncertainty, according to Savills’ 2026 ports report. The increased activity came at a time of slow but distinct recovery for U.S. industrial markets.

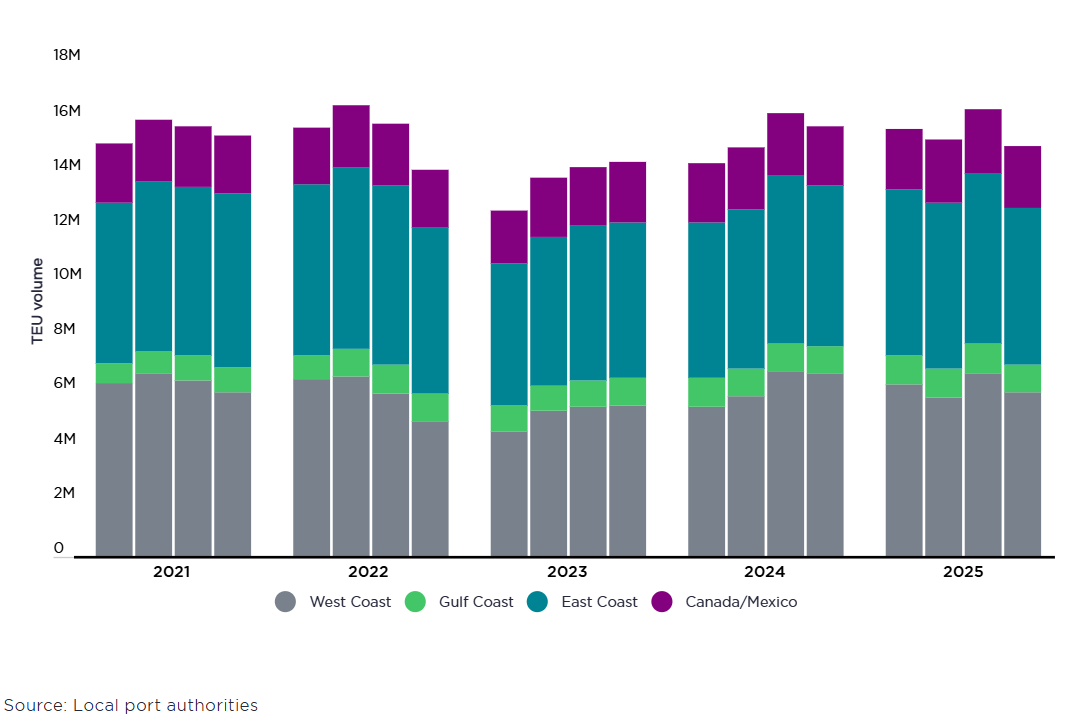

Container volume rose 1.6 percent year-over-year in 2025 to 62.3 million TEUs across the top 15 North American ports, the report noted. TEU (Twenty-foot Equivalent Unit) is a standard measurement of shipping based on the volume of a 20-foot-long intermodal container.

The U.S. industrial market, according to Savills, saw vacancies climb no higher during the fourth quarter of 2025, coming in at 8.2 percent. That stabilization was in the wake of 13 quarters of rising vacancy for the industrial market. Leasing also rebounded during the year compared with 2024 despite—or perhaps because of—unresolved trade policy, since lease expirations forced decisions by tenants.

Container activity and industrial markets

Increased container activity often correlates with positive absorption and relatively low vacancy rates in port-associated industrial markets. The top busiest U.S. container port is Los Angeles, which it has been for 26 years in a row. In 2025, Los Angeles handled 10.2 million TEUs, a slight decline from 2024, yet still a top three all-time year for cargo volumes, Savills reported.

The Port of Long Beach followed a record-breaking 2024 with yet another record-breaking 2025, handling 9.9 million TEUs, a 2.4 percent year-over-year increase, making it the second-busiest container port in the U.S.

At the same time, there were 3 million square feet of positive absorption in the Los Angeles industrial market in 2025, including Long Beach, with the market coming in at 7.1 percent vacant at the end of the year, which is lower—but not greatly lower—than the national industrial vacancy of 8.2 percent, according to Savills data.

Despite L.A.’s exposure to China, with more than 40 percent of its volume tied to China-based ports, policy shifts around tariffs didn’t dampen L.A. port activity last year. Rather, the Port of Los Angeles handled 1 million TEUs in its busiest month (July)—evidence of its volatility—and in the second half of the year, July through December, averaged just over 880,000 TEUs per month. Continued growth for the port is likely, as evidenced by a proposal for a new 200-acre container terminal.

READ ALSO: Top 10 Emerging Industrial Markets

“In step with the port’s continued success has been its investment in the container business, most notably the recently started $365 million Pier G – ITS slip fill redevelopment, which stands to create additional acreage at Terminal G and allow service to the largest cargo vessels,” Savills noted in the report.

On the other coast, Northern New Jersey also turned in container volume growth as well as positive industrial absorption and relatively low vacancy. Savills reported that northern New Jersey (along with New York), building on a strong 2024, handled nearly 9 million TEUs in 2025, which is its third-busiest year on record, despite concerns about tariffs.

The industrial vacancy rate in Northern New Jersey came in at 7.3 percent, also below the national average, and the industrial market absorbed 4.8 million square feet.

“Much like Southern California, higher real estate and labor costs—where northern New Jersey ranks at or near the top nationally—are the cost of doing business for access to the busiest container port on the Eastern Seaboard and the nearly 20 million consumers living in the greater New York metropolitan area,” the report noted.

Container volume outlook for 2026

Container volumes are expected to ease or remain flat in 2026 as front-loading—the practice of trying to get ahead of factors (such as tariffs) that might cause a spike in costs—eases especially for U.S. ports, Savills predicts.

“Port activity this year will probably experience some short-term volatility but perhaps some growth if tariff uncertainties are resolved and supply chains adjust to a new trade policy landscape,” Savills Head of Industrial Services Gregg Healy told Commercial Property Executive. “The lingering question is what impact will potential refunds have on all of this?”

FedEx is already asking for refunds, others will likely follow, Healy says. The Trump administration is trying to make a deal by providing smaller refunds now in exchange for closing them out with speed.

“We’ll see how that plays out,” Healy said. “Also, will there be some drag in the short term as they sort this out? Some countries—the major exporting countries—will see a benefit to the lower tariff rates and may try to adjust manufacturing schedules to take advantage of the lower tariffs before another new policy is enacted.”

Activity at ports will remain an important factor in driving nearby industrial markets, and Savills posits that port-associated industrial markets will probably turn a corner in 2026 toward strength, as vacancy rates peak and fundamentals stabilize.

At the very least, port activity isn’t likely to be as volatile this year as last year, which ought to be beneficial for associated markets. Last year, Long Beach was the most volatile U.S. port, with its volatility index at nearly 19.1 percent. The index is based on trailing three-month standard deviation of loaded import volumes relative to the three-month average. The second most volatile U.S. port was Los Angeles, at 16.9 percent.

You must be logged in to post a comment.