Building for the Storm Ahead: Climate Resilience in CRE

As billion-dollar weather events surge, Kip Sowden of RREAF details how insurance costs, tech and site selection are redefining real estate feasibility.

Over the past few years, the U.S. has experienced record-breaking storm activity, with 27 confirmed billion-dollar disasters in 2024, totaling more than $180 billion in damage, according to data from the National Centers for Environmental Information. While the National Oceanic and Atmospheric Administration’s long-term average is nine major events annually, the current five-year trend is 23 per year, with the interval between big disasters shrinking from months to mere weeks.

In the first half of 2025 alone, insured losses totaled $80 billion, preliminary estimates from Swiss Re Institute show, primarily driven by wildfires and severe thunderstorms. These escalating losses are redefining climate resilience in CRE, forcing investors, developers and lenders to rethink how they underwrite risk, select sites and design buildings.

Insurance availability, construction standards and capital stack discipline are now inseparable from resilience planning. This growing alignment has accelerated interest in green building trends across the commercial real estate sector.

For RREAF Holdings, which has a national portfolio spanning multifamily, hospitality, master-planned communities and outdoor resorts, building climate resilience into CRE is not an abstract ESG goal. We sat down with Founder & CEO Kip Sowden to talk about how his company integrates resilience into underwriting, design and portfolio management, and why preparation for the next storm starts long before the first warning.

READ ALSO: Top 5 Risks REITs Face Today

In light of increasingly severe storms across the country, how are you rethinking your development playbook?

Sowden: We are fundamentally rethinking our approach to building and operations. For us, storms are no longer just a ‘what if’ scenario. They’re a ‘when.’ While we are actively developing along the Texas Gulf Coast, we must consider the increased risk of weather-related damage and incorporate that into our underwriting costs. Additionally, we hire top-tier consultants who specialize in the type of development we are pursuing. Their expertise helps us ensure we are adequately prepared for any region-specific weather damage that may occur.

Where is the push for more resilience features coming from?

Sowden: Insurers and lenders are increasingly becoming the driving force behind resilience features. Developers genuinely want to do the right thing, but when debt terms or insurance coverage hinge on these features, they move from optional to essential.

In this context, are there any specific geographies that will be more attractive for resilient development over the next decade?

Sowden: Communities with strong utility infrastructure, elevated coastal assets and inland growth markets will lead the way.

How has insurance availability and cost altered the feasibility of new projects in storm-prone regions? Have you walked away from deals purely because the insurance math didn’t work?

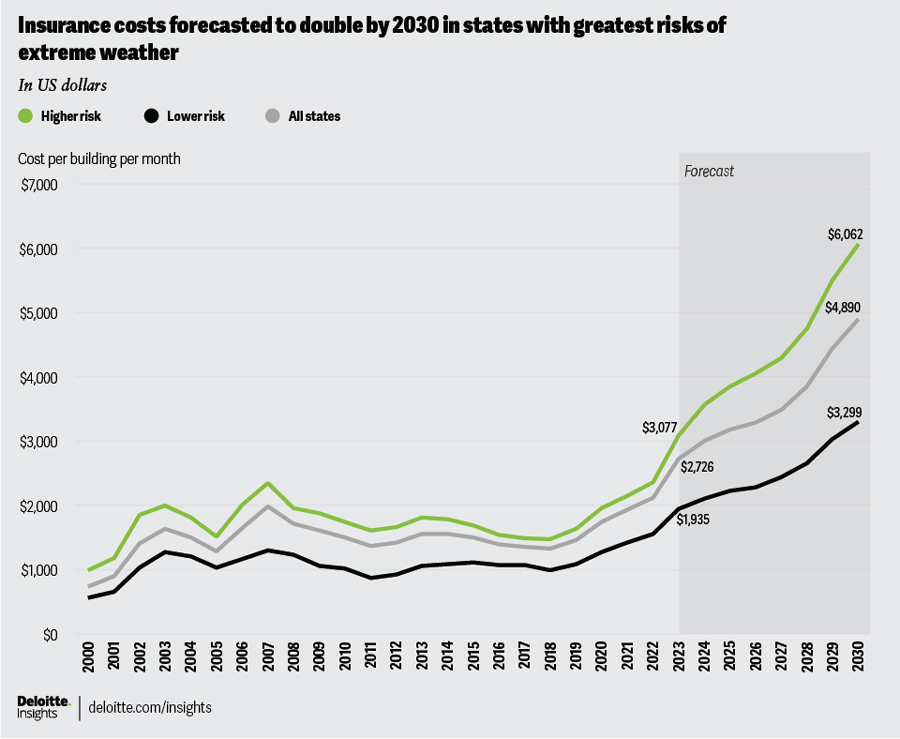

Sowden: Rising premiums have made climate resilience in CRE a measurable financial factor rather than a conceptual ESG issue. It now directly influences underwriting feasibility and market selection. In all our development deals, we will not pursue projects that do not pencil. The Deloitte Center for Financial Services forecasts that the average monthly cost of insurance for a commercial building will rise at a compounded annual growth rate of 8.7 percent, increasing from $2,726 in 2023 to $4,890 by 2030.

As insurance companies raise premiums to keep pace with rising claims, developers now recognize two key line items that require greater precision—insurance and construction costs—and must model elevated risk into every pro forma.

Has the rise in insurance costs already materially changed investor appetite in certain markets? Do you think this will redefine which U.S. regions are investable?

Sowden: Institutional buyers in Tier 1 coastal wind zones remain interested but have adopted a more disciplined approach. A significant shift has occurred in the underwriting process: Insurance costs and growth assumptions are now critical components of every pro forma analysis.

We consolidate all coastal exposures into a single master program, which is strategically timed after reinsurance renewals. We conduct Probable Maximum Loss actuarial studies to determine coverage needs accurately. This strategy helps us manage costs effectively without being over-insured.

While premiums rose sharply after 2017, we are now witnessing a return of capital to the market with rates stabilizing. As a result, there is still strong demand for beachfront properties, but the buyers are increasingly larger and better-capitalized groups that can absorb higher deductibles and self-insured retentions.

How do you model storm risk and resilience costs when underwriting new deals?

Sowden: We consider resilience features as capital-improvement line items, each with a defined ROI horizon. In areas prone to storms, we model for higher reserves and more volatile insurance renewal cycles. We’ve seen greater interest in climate risk from investors, particularly when we are developing projects in areas vulnerable to weather-related damage.

Where are you seeing the biggest wins with predictive maintenance tools in your portfolio?

Sowden: HVAC and water intrusion detection systems provide early alerts that prevent minor issues from escalating into multimillion-dollar losses, particularly after storms.

READ ALSO: A New Climate Agenda for CRE

How do you evaluate emerging technologies before deploying them? Do you pilot on a single asset first, or roll out portfolio-wide?

Sowden: We pilot new technologies before implementing them across our portfolio, often focusing on assets where the technology provides the best return on investment.

How do you train or upskill your operations teams to use these tools effectively?

Sowden: RREAF’s growth from $100 million in assets under management to more than $4.7 billion over 10 years is largely due to our data-first approach. Our team adapts quickly to digital advancements. We prioritize training for all team members and provide various methods to enhance skills. Additionally, we maintain a live standard operating procedure that is updated quarterly to reflect new changes and essential action items.

How long until predictive analytics will become a standard expectation from lenders and investors?

Sowden: In three to five years, it will be standard practice. We are already receiving inquiries from institutions regarding how to monitor operational efficiency.

Do you see sustainability and resiliency as defensive strategies or as value-creation drivers?

Sowden: Both options are important. Risk reduction protects against losses, while resilience drives additional benefits: lower insurance costs, higher tenant retention and often better financing terms.

When you walk properties after a storm event, what’s the first thing you personally look for, beyond the engineering reports?

Sowden: I look at the people—our residents and staff. Are they safe, and what can we do to assist with restoration efforts? Our onsite teams are incredibly selfless when it comes to providing the best care for our residents and guests. During Hurricane Helene in 2024, many of our residents and guests were affected by the storm, but our properties and hotels went above and beyond.

How has your leadership style evolved in response to unexpected crises such as natural disasters?

Sowden: I’ve learned the importance of delegation, and the teams I trust always impress me. After Hurricane Helene, our onsite teams organized relief efforts more swiftly than corporate could have managed. They demonstrated that resilience is as much about culture as it is about physical strength.

Tell us more about what it means to you to be able to leave a legacy of more resilient communities, passing the platform to the next generation.

Sowden: I want to create communities that endure, focusing not only on financial returns but also on the well-being of people. For my team, I hope they embrace the belief that prioritizing the needs of residents is not only the right thing to do but also the smartest long-term business strategy.

You must be logged in to post a comment.