Why Life Science Space Faces a Slower 2026

What’s behind the sector’s transition from rapid expansion to disciplined growth.

Good times for life science real estate aren’t over, though momentum is slowing, according to Colliers’ 2026 outlook.

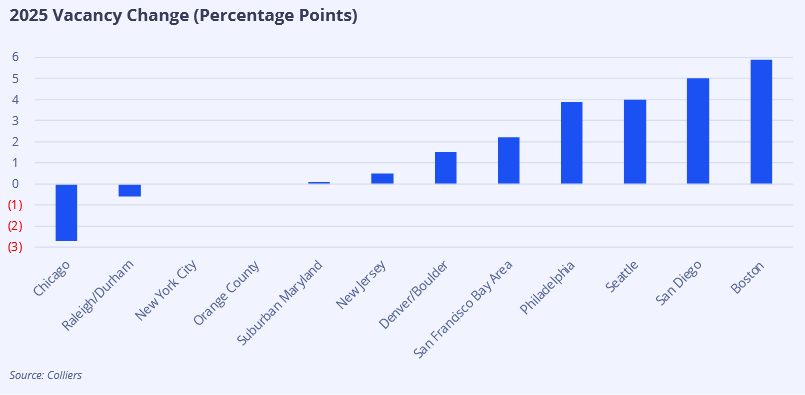

Take perennial life sciences powerhouse Boston for an example. As a result of substantial new construction colliding with a decline in occupied space, the metro now has 16 million square feet of available space, a record high in total availability.

Colliers noted that Boston is one of five tracked metros where vacancy rates now exceed 20 percent. Rising vacancies are putting downward pressure on asking rents, while some owners are targeting non-life science tenants.

Declining rent levels in Boston (and in Philadelphia and other regions too) “are creating favorable conditions for tenants,” the report stated. Nonetheless, strong biotech employment and AI adoption in Boston (and, again, in other regions) are expected to continue to drive demand over the long term.

READ ALSO: What’s Behind the Surge in M&A, Privatization Activity?

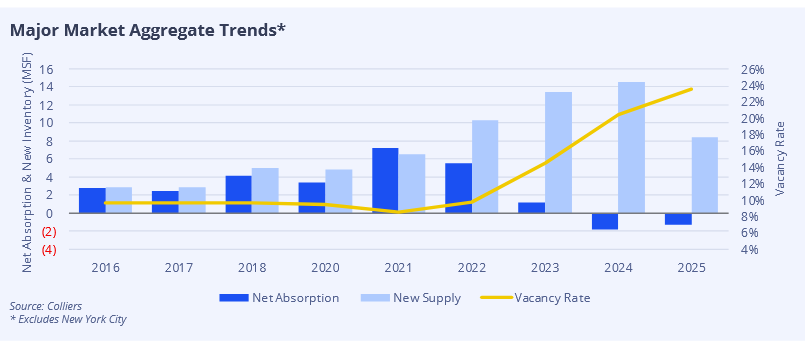

How long a long term? “The unprecedented wave of construction is coming to an end,” is how Colliers puts the situation, adding that given current conditions, achieving market equilibrium in many metros could take several years.

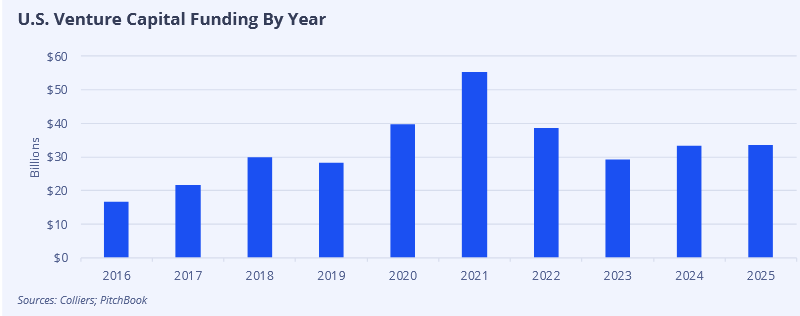

So how did the high-flying biotech sector’s wings get clipped? A wide variety of macroeconomic factors have been constraining tenant demand, Colliers explained, including a weak stock market that postponed IPOs for many companies and reduced access to venture capital funding. Though the latter amounted to $33 billion in 2025, that was about 25 percent below the average at the height of the market, in 2020–2022.

The outlook noted that 2025 was the second consecutive year in which the major market aggregate experienced negative net absorption.

Turning back upward?

However, while 2025 has been disappointing vis-a-vis the early-COVID boom, there are favorable signs.

“The most significant trend in the life science market has been the ramp-up of M&A investment and licensing of emerging treatments in the U.S. and in China by global pharmaceutical companies,” Joe Fetterman, executive VP at Colliers, told Commercial Property Executive. “Second to that has been the significant uptick in demand for U.S.-located CGMP manufacturing facilities by global, domestic and European pharmaceutical companies.”

Macroeconomic bobbles notwithstanding, the outlook tallies some further emerging signs of better news over the course of this year. For one, biotech/life sciences sector hiring is again increasing, though modestly. “Leasing trends across most markets reflect this shift, as net absorption in many tracked cities either held firm or improved from 2024 to 2025,” the report noted. Furthermore, onshoring trends and the rise of blockbuster drugs like GLP-1 could help push demand for GMP manufacturing facilities, as firms respond to policy-related factors such as rising global tariffs, supply chain risks exposed by COVID-19, national security concerns and shifting federal incentives and regulations.

Another factor is that distressed properties that are struggling to land tenants might be picked up by investors looking for opportunities. In addition, as 2026 began, only about 7 million square feet were under construction, much of which is either build-to-suit or at least partially preleased, and speculative starts are very limited in most markets, according to Colliers.

You must be logged in to post a comment.