Is 2026 the Year for a Steadier Ride?

The past few years have been a roller coaster for CRE. Is relief in sight?

After the roller coaster ride of the past few years, it’s only natural to want a little stability for the commercial real estate market in 2026. Not a slowdown, necessarily. Just fewer loops. Not quite so many sharp turns. At least a clearer view of what’s ahead so you can better prepare for it.

“What is crazy about the last few years is every metric you can think of that we normally use to predict macroeconomic trends or real estate trends has been either dead wrong or so confusing and muddled that it’s impossible to piece out what’s going to happen next,” observed Ryan Krauch, senior managing director at Affinius Capital, during a CPE Voices webinar I moderated about the market to come.

However, the panel, Krauch included, expressed greater optimism for 2026, and they’re not alone. The series of interest rate cuts in the latter part of 2025, improved fundamentals due to industry discipline and continued interest from both lenders and investors have all been contributors to more positive expectations from a growing number of forecasters and longtime industry players. So too has growth in in-demand niches such as data centers and medical office properties.

What’s more, while a focus on opportunistic and value-add deals continues to define the active capital pool, there’s been increased interest in core investments, writer Joe Gose reports this month in “CRE Dry Powder’s Piling Up. Will Sparks Fly Soon?” While still early, that’s a healthy sign for the market since it affords sellers a chance at fair trade value, CBRE U.S. and Canada capital markets co-head Tommy Lee pointed out to him. “We expect the sponsors to be far more active in 2026,” he said.

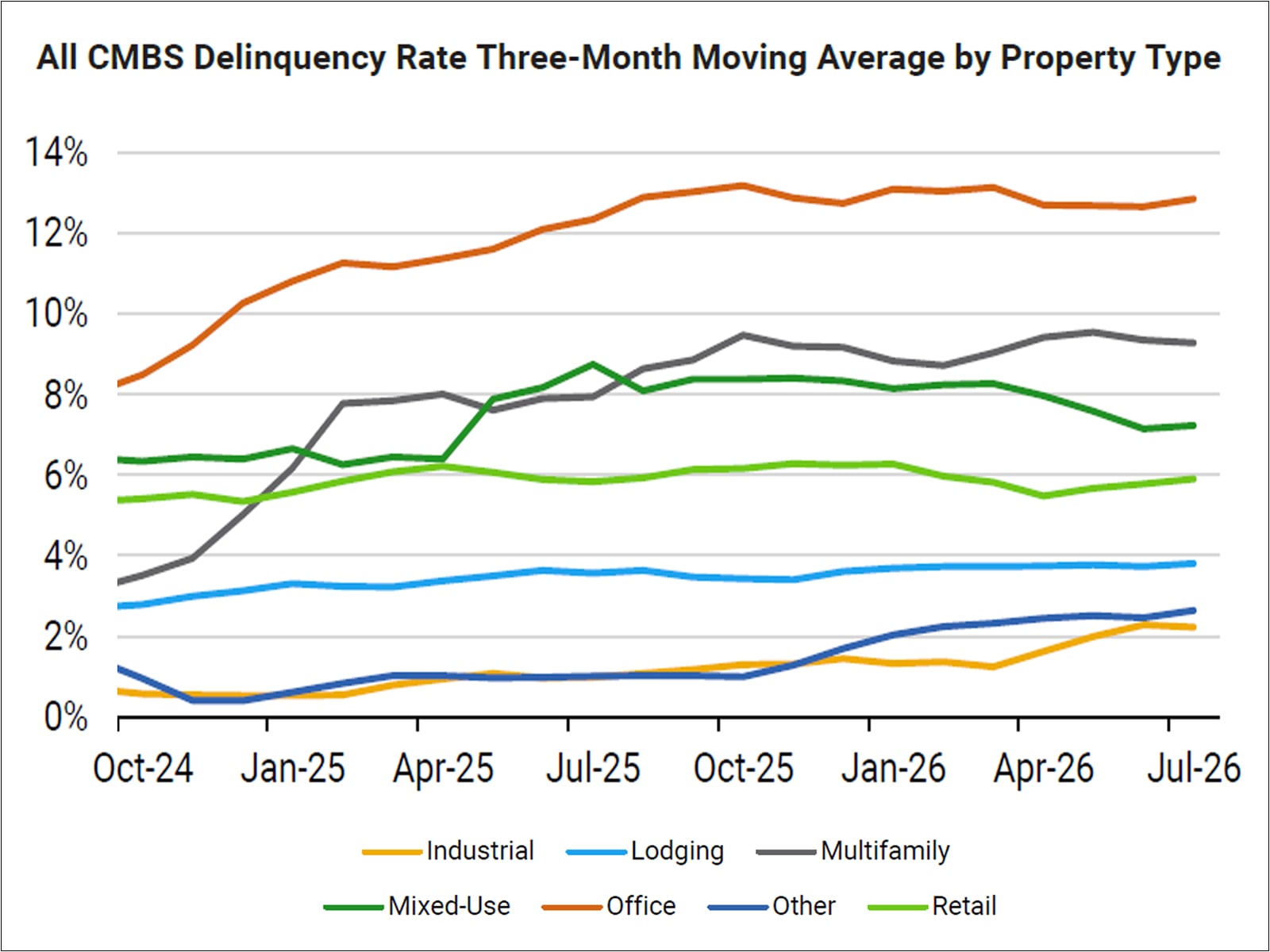

Even the office sector is in a better position than it was. “2025 was a year of adjustment,” Jordan Lang, president of McCourt Partners, told senior associate editor Corina Stef for her 2026 Office Outlook. “After several years of resetting expectations, we began to see the outlines of a more stable market.”

More consistent leasing patterns are making it easier to develop expectations for tenant space needs, improving the accuracy of projection. And conversions for other uses have contributed to inventory reduction to a greater extent than had seemed likely, recreating neighborhoods in the process.

There’s certainly more pain to come for the sector—in the form of discounted sales, teardowns and foreclosures, with a decrease in overall office inventory a necessity for recovery. There are also still plenty of potential challenges for other property types, as well, some of them unpredictable.

The roller coaster still has dips and turns. But it’s becoming easier to see what’s up ahead.

You must be logged in to post a comment.