CRE’s Dry Powder Is Piling Up. Will Sparks Fly Soon?

Investors are hopeful for a busy 2026.

Fund sponsors amassing dry powder since the pandemic began, only to be stymied by a spike in interest rates and rising redemption requests, are becoming more bullish on the prospect of finally putting their capital to work.

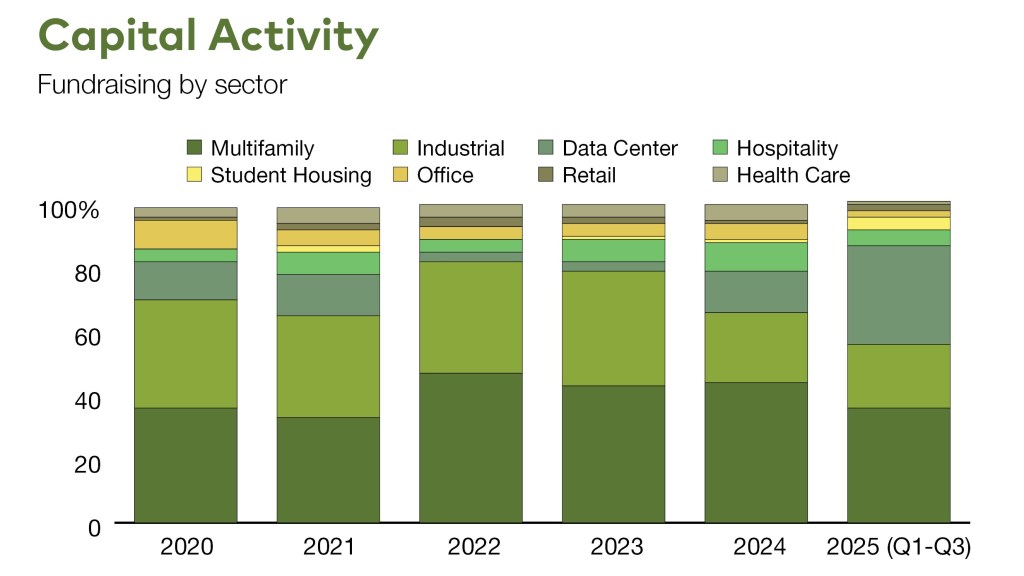

Just as fund sponsors have become more optimistic, so, too, have limited partners. After two years of moribund activity and redemptions, private real estate fund managers enjoyed a rebound in capital inflows in 2025. Globally, $164.4 billion raised through the first three quarters surpassed 2024’s volume, reported PERE. Nearly $115 billion of that total is targeting North America or multiple regions. North American strategies are in the market for about $203.5 billion, more than double the capital targeting Europe, which is the second-largest market.

Roughly $250 billion in private capital for North American properties today is comparable to other cycle bottoms when adjusted for inflation, inventory growth and appreciation, suggested Adrian Ponsen, senior CRE economist & strategist at Cushman & Wakefield. But deploying capital can be a challenge, especially among funds that were seeking to target distress.

READ ALSO: Stars Align for CRE Secondary Funds

“I’m not hearing that a lot of funds are behind in their deployment targets, but there may be some dry powder backing up because distressed opportunities aren’t accumulating much beyond the office sector,” Ponsen added. “But funds with a large amount of assets under management also tend to be more patient.”

A return to core?

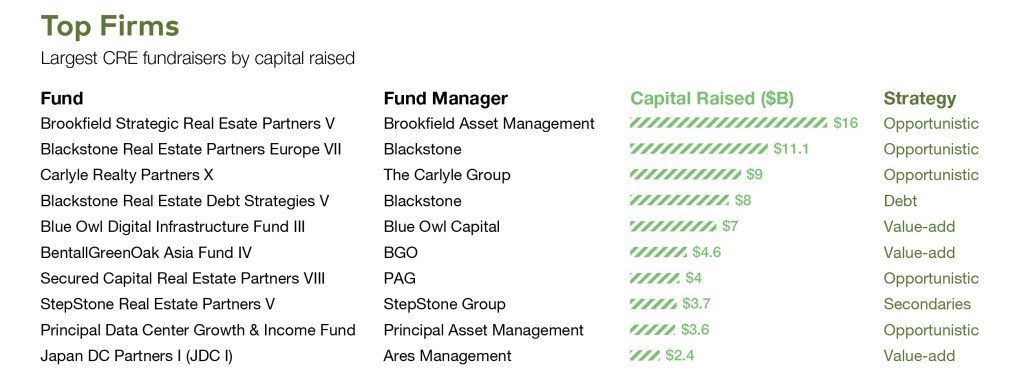

Opportunistic and value-add strategies are driving much of the fundraising activity, PERE reported, accounting for 65 percent of all global capital raised. Among other notable results, Brookfield Asset Management and Carlyle reported record inflows for their latest opportunistic iterations.

Still, interest is percolating for core and core-plus strategies, which have been less popular as of late, reported Heitman Managing Director Brian Pieracci, who oversees the real estate investment firm’s private equity strategies in North America. It’s a trend that’s likely to continue as vehicles such as pension funds begin to move down the risk spectrum to focus on cash flow.

READ ALSO: Brookfield AM Brings Real Estate Fund to $16B

“It’s not huge numbers we’re talking about, but we started to see a shift to core strategies midway through summer,” he commented. “There have definitely been more inbound capital flows and interest than redemptions.”

The reemergence of core investors would further signal the return of a healthy transaction market, noted Tommy Lee, president & co-head of capital markets in the U.S. and Canada at CBRE.

“We’ve already seen core capital in our bidding pools in the third quarter and (then) the fourth, and we expect the sponsors to be far more active in 2026,” said Lee. “Their participation in the market is important because we’re seeing a significant number of opportunistic buyers, who are always looking for a deal. But the cost of core capital allows sellers to transact with buyers looking for fair trade value.”

Capital destinations

The rebound in investment sales is signaling a healing market, as well. Through the first three quarters of 2025, year-over-year sales of retail and industrial assets represented an increase of 21 percent and 16 percent, respectively, according to MSCI Real Assets.

The return-to-work movement’s aftermath, along with improving leasing activity and absorption, has also helped fuel office trades which, through September, increased 24 percent over the prior year, reported MSCI Real Assets. Most deals have been at discounts to replacement cost as the sector still suffers from high vacancies. But that could begin to change in 2026.

“I think you’ll see continued dominance in the industrial and multifamily sectors, but we’ll see elevated sales activity in offices compared to the last two years,” Lee added. “Investors have become more comfortable with office, and the more that comfort grows, the more institutional capital we’ll see in the category.”

READ ALSO: No Credit Bubble Yet: NYU Schack

One of the challenges for investors has been the lack of fundamentally strong property types on the market. A lingering bid-ask spread amid volatile interest rates has also foiled deals, especially for owners of marginal assets that have been able to get loan extensions. But with financing benchmarks such as the 10-year Treasury yield settling around 4 percent, investors are more optimistic about 2026.

“We see a lot of loans coming due in 2026 and 2027, and owners will have to either refinance or sell,” advised Ani Paulson, senior vice president on Northmarq’s commercial investment sales team. “So investors are gearing up to deploy capital over the next two years.”

Flexibility favored

Multitenant flex assets are particularly in demand for about 60 percent of Paulson’s clients, many of whom are rotating out of apartments. The buyers like the small units of such assets: They’re typically easier to lease than big-box warehouses, and tenant improvements tend to cost less than in office and retail, she pointed out.

Retail is also high in demand, with institutional investors continuing to prefer grocery-anchored centers and, increasingly, nonanchored strip properties, Paulson added. But value-oriented investors, such as Midloch Investment Partners, are hunting for retail assets seeing stress, like a lack of capital to fund tenant improvements, shared Andy Sinclair, CEO & principal of the firm.

READ ALSO: CRE Investors Find Bright Spots Amid Headwinds

Midloch still places a larger emphasis on industrial properties, however, which make up about 40 percent of its portfolio, while apartments account for another 40 percent. Yet, given oversupply in some markets, along with economic and lingering tariff uncertainties, the firm has narrowed its industrial parameters.

“Industrial properties either have to be small, multitenant deals with a good, diversified tenant roll and a shorter-term WALT, or NNN assets with staying power,” Sinclair said. “Medium- to large-sized boxes that have three-to-five-year maturities are a little bit in no man’s land.”

Hunting for alternatives

Industrial properties are high on Heitman’s wish list, too, especially those in supply-constrained markets that can be bought below replacement cost, and the investment manager is researching data centers for potential future investments.

But Heitman’s broader strategy includes a heavy dose of alternative assets, particularly medical office and self storage, Pieracci said. Growing institutional investor interest in alternatives has not only coincided with rotations out of momentarily risky or oversupplied categories but also with operational fundamentals that line up with societal and population trends, he noted.

“The demographic story in the U.S. and the proliferation in the ways that people want to see their doctor fits well with the medical office,” Pieracci reasoned. “Alternatives are still a very small component of the institutionalized real estate investment universe, but investors are focused on increasing their exposure.”

You must be logged in to post a comment.