How CRE Leaders Should Plan for Climate Disclosure

Despite no federal regulation, markets will likely reward transparency.

When the current administration took office in January, one thing was clear: Fighting climate change would not be a priority.

So, it wasn’t surprising when the Securities and Exchange Commission backed away from its sweeping Biden-era climate disclosure rules that would have required public companies to disclose the greenhouse gas emissions of their assets, along with how vulnerable these assets were to climate-related risk.

But despite the about-face on climate at the Federal level, experts say investors are realizing the benefits of transparency regarding these issues, and the long-term financial soundness of sustainability generally. Meanwhile, a growing number of states are passing their own climate disclosure legislation.

“Free markets really do depend on the free flow of information, so failing to report the data doesn’t make the problem go away,” said Alex Dews, CEO of the Institute for Market Transformation, a nonprofit focused on advancing sustainable buildings. “It just makes it harder to see and makes it more of a future problem, particularly in terms of climate.”

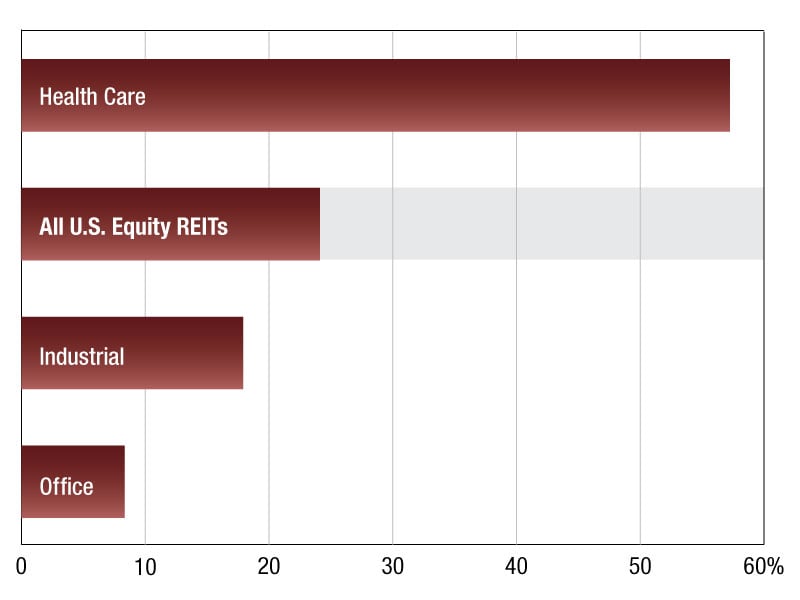

A 2024 survey by Stanford University’s Graduate School of Business and the MSCI Sustainability Institute, for instance, found that 93 percent of investors believe climate issues are likely to affect the performance of assets over the next two to five years.

And moving forward, individual states will follow California’s and Washington state’s lead and pass their own legislation requiring these types of disclosures, making it likely climate-related transparency will remain a part of sustainability efforts and investment due diligence.

What did the rules say?

Adopted in March 2024, the SEC’s policy required public corporations to disclose to investors details about their Scope 1 emissions (referring to direct emissions from company assets) as well as their Scope 2 emissions (indirect emissions from purchased energy). An earlier version included Scope 3 emissions (all the emissions in a company’s value chain).

The SEC policy also mandated disclosure of a firm’s exposure to climate-related risks. These risks could include the impact of higher temperatures on building materials or a site’s susceptibility to flooding, for example.

Supporters of these rules argue that it’s important for companies to be transparent about how the emissions of their assets—along with any financial risks associated with climate change—impact those assets.

“There are lots of different risks out there related to climate that investors, more and more, want to understand before they invest in a company,” noted Elizabeth Beardsley, senior policy counsel at the U.S. Green Building Council.

Free markets really do depend on the free flow of information, so failing to report the data doesn’t make the problem go away.

—Alex Dews, CEO, Institute for Market Transformation

Critics of the SEC’s rules complained that complying with the policies would have been onerous, leading Republican state attorneys general and the U.S. Chamber of Commerce to challenge the guidelines in court, according to the Institute for Business in Global Society at Harvard Business School. The SEC then delayed enforcement of the policy, and, in March of 2025, the agency announced it would not defend the policy in court.

While there had previously been various industry standards and a growing body of local regulations governing climate disclosure, the SEC’s policy aimed to standardize the practice among all public companies, Beardsley said. With the federal policies now gone, a return to the patchwork system of the past is likely.

States (and Europe) take the lead

California, for instance, has two new pieces of legislation that will take effect in the next few years.

The Climate Corporate Data Accountability Act, or SB 253, will require companies with more than $1 billion in revenue to report their greenhouse gas emissions, including Scope 3, which includes downstream emissions caused by suppliers or tenants. The Climate-Related Financial Risk Act, or SB 261, will mandate that firms with more than $500 million in annual revenue report their climate risk.

Notably, California’s laws apply to all businesses—both public and private companies—that meet the criteria and do business in California.

There are lots of different risks out there related to climate that investors, more and more, want to understand before they invest in a company.

—Elizabeth Beardsley, senior policy counsel, U.S. Green Building Council

“Most large companies operate in California, and so for their ease of operations, they will likely use the enormous leverage to push their suppliers and landlords to standardize based on the California rules,” Dews said. “I think the likely outcome is that those rules do become a de facto national standard for real estate.”

New York, Colorado, New Jersey and Illinois have similar bills before their legislatures.

The European Union is also moving forward with similar regulations that will apply to companies with European subsidiaries or those that report high revenues in the EU, according to the Institute for Business in Global Society.

Climate disclosure and CRE

Despite pullback at the Federal level, the focus on climate risk data is expected to intensify as tenants and the capital markets increase their focus on shrinking carbon footprints, building resilience and instilling wellness.

There is evidence demonstrating a link between sustainability and ROI, according to Dews, who pointed to a 2025 Knight Frank survey that found 63 percent of investors globally reported a connection between ESG efforts and stronger returns. And from a user perspective, research from JLL revealed that demand for low-carbon workspaces is set to outstrip supply by 75 percent by 2030, a projected supply shortage of 57 million square feet.

“Whatever might be happening for any moment of time outside in the universe is an interesting point to talk about, but it’s not changing very long-duration decisions,” said Jonathan Flaherty, global head of sustainability for Tishman Speyer, said during a panel discussion at the CRETech conference in New York. “We’re going to make those decisions the way we think is appropriate.”

Tishman Speyer was the development manager for JPMorgan’s new $3 billion, 2.5 million-square-foot headquarters in Manhattan. The Park Avenue property is fully powered by clean energy and boasts net-zero operational emissions and serves a model of net-zero planning for commercial real estate.

“They did what other people said could not be done,” noted fellow panelist Joseph Allen, a Harvard professor who studies how to make buildings healthier and whom JPMorgan Chase consulted for its project. “Now other people are copying them, and it’s also influencing policy and practice way beyond commercial real estate. Now it’s showing that these things can be done.”

When not bound by a Federal or a state mandate, however, investors may still struggle with how much data to disclose to other investors or to tenants. Portfolio-level data, some say, lacks the nuances of what is happening in each market and at each property, and may not reflect mitigation efforts.

Thinking long-term will be the safest option, according to USGBC’s Beardsley, especially in the face of future state regulations. “We do not think it’s time to back off on collecting and understanding climate risk and impact, but rather to dig deeper,” Beardsley said. “It’s really an opportunity to position the business for the future.”

You must be logged in to post a comment.