Are You Ready for the Refi Rumble?

Lenders are competing for the best loan prospects.

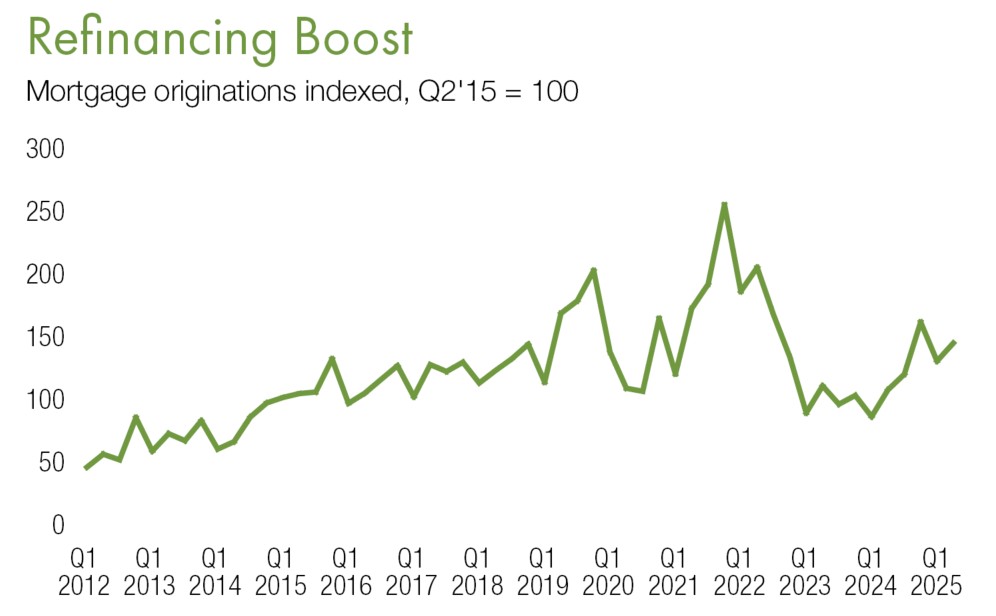

High interest rates continue to suppress CRE acquisition loans, but the constant thrum of maturing mortgages is fueling brisk refinancing activity among lenders and intermediaries.

The good news for borrowers is that capital is growing more plentiful. The number of lenders grew at a double-digit pace in the first half of 2025, according to MSCI Real Assets. Banks led the resurgence with a 25 percent increase in participants, followed by private lenders at 17 percent.

“Multifamily is always kind of a different financing beast because the agencies are so prevalent,” said Daniel Hartnett, senior managing director & leader of the national capital markets practice at Greysteel. “But for all other commercial properties, this is probably the most liquid we’ve seen the debt capital markets since 2021.”

READ ALSO: Banks Rebalance, Refuel, Recycle

One big driver of that liquidity is three years of consecutive record-breaking annuity sales in the U.S., which is filling life insurance company coffers, observed Wally Reid, senior managing director & debt platform leader at JLL. Refinancing dollar volume is 60 percent of JLL’s mortgage origination business so far this year, almost three times the acquisition loan dollar volume.

Annuity sales in the U.S. during the first half of the year totaled $225.8 billion, a year-over-year increase of 4 percent, according to LIMRA, an insurance and financial services trade association. As a result, life insurance companies are joining other lenders in originating more short-term loans.

Borrowers are fine with that. After spending the last three years waiting for a better rate environment—and in some cases extending loans—they can finally smell higher property values ahead. So, most borrowers are seeking three- to five-year loans with flexible prepayment provisions. That should help them sell when the time is right.

“Borrowers aren’t looking to lock in 10-year financing because the general consensus is that interest rates are coming down,” said Josh Darby, vice president & producer for new debt and equity in the Atlanta area for Northmarq. “They’re thinking: ‘I’m not going to sell next year or the year after, but I might in three years, when the market is better.’”

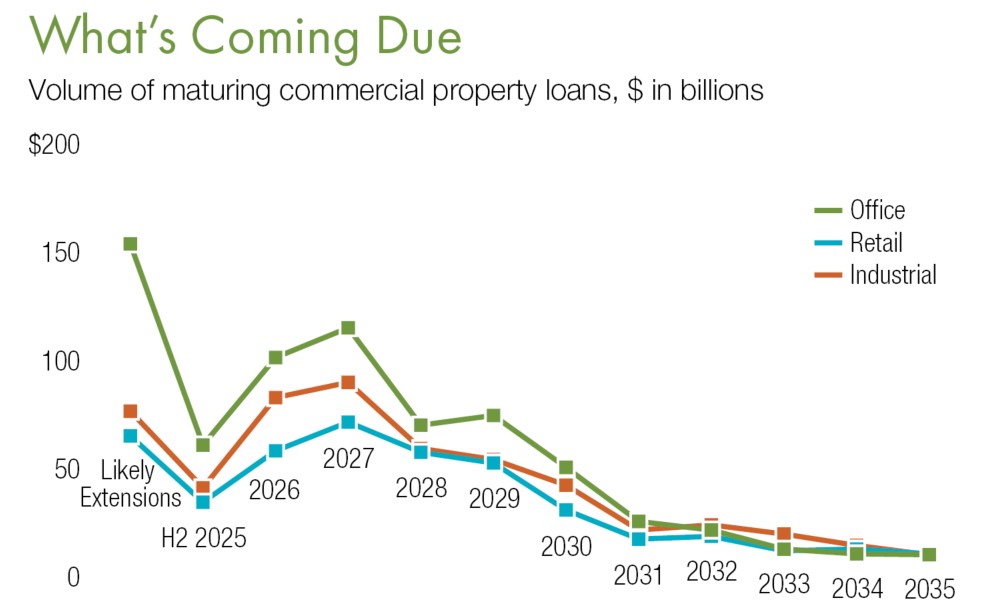

Maturities rising

At the midpoint of 2025, some $129 billion in office, retail and industrial mortgages were scheduled to mature by the end of the year, with office loans accounting for about half of that total, MSCI Real Assets shows. Maturities across the three asset classes are expected to reach about $235 billion next year and $269 billion in 2027, the organization reported. Meanwhile, it estimates that $151 billion in office loans have been extended into 2025 and beyond.

READ ALSO: Why the CRE Transaction Volume Is So Low

Even with overflowing war chests, lender eagerness still depends on typical factors such as location and sponsor. Another important property criterion lenders are considering is the weighted average lease term to project cash-flow, noted Reid. Many industrial and retail properties can deliver the WALT lenders want to see, but a lot of office assets can’t, he continued.

In September, JLL arranged a $130 million refinancing for a 1.1 million-square-foot portfolio of 17 warehouses and other properties in Southern California owned by Sukut Real Properties. An insurance company provided a five-year fixed-rate loan for the assets, which are 98 percent occupied.

“You can definitely link the ability to refinance to WALT in the industrial, retail and office sectors,” Reid reasoned. “You have to have steady cash flow for more than four years to get a good loan.”

Office comeback?

The lender emphasis on WALT has contributed to a bifurcated refinancing environment between Class A assets and just about every other office property, Hartnett said. “Most lenders are still very hesitant about refinancing office unless there’s a very compelling story,” he pointed out. “They’re looking at the loan amount per square foot, the location and sponsor, the WALT and the diversity of the rent roll.”

Lenders underwriting an office building with a debt yield of 9 percent before the pandemic, for example, have likely increased the metric to between 12 and 14 percent to reflect today’s higher risk, added Hartnett. In early October, he was working with a regional bank to refinance an office tower in Uptown Dallas. The project is 85 percent leased, and the sponsor is bringing in a new equity partner.

READ ALSO: Discounted Office Sales Multiply, Pressures Persist

Still, the appetite for office originations continues to improve, and highly occupied, under-$50 million neighborhood buildings that are within walking distance of restaurants and services are seeing exceptional demand from lenders, said Reid. When thinking about the sector more broadly, some owners may have to inject additional equity or boost leasing and commission reserves to secure refinancing. But office appears to be rebounding.

“Tenant improvement costs are stabilizing, rents are going up and leasing is truly happening,” Reid continued. “Companies that put off leasing or just signed for one to three years are now looking for 10- to 15-year leases.”

In Edina, Minn., Cushman & Wakefield closed on an $11.3 million take-out loan earlier this year arranged with a bank to refinance the E, a 108,000-square-foot boutique office property. Over the last 24 months, the E signed 97,000 square feet of new tenants following a $6.8 million renovation, pushing occupancy to 94 percent.

“Certain assets demand a finer look by lenders today, and office specifically is one example,” observed Jeff Altenau, vice chairman of Cushman & Wakefield & leader of its equity, debt and structured finance platform for Chicago and the Midwest. “The sector has gone from seeing next to zero financing alternatives the last few years to a growing number of banks, debt funds and life insurance companies showing interest today.”

Competitive landscape

The influx of fresh credit has ginned up competition, particularly between life insurance companies, regional banks and credit unions, with each pricing debt at less than 200 basis points over the U.S. 5-year Treasury or the SOFR for sound, cash-flowing assets with conservative leverage of around 60 to 65 percent, observers say. At the end of September, the U.S. 5-year bond yield was around 3.6 percent, while SOFR’s clocked in at 4.13 percent.

Walker & Dunlop Investment Partners, which recently closed a $135 million equity fund, is refinancing 81,000 square feet of office and warehouse space and 5.5 acres of outdoor storage in suburban Atlanta, said Brian Cornell, managing director of the fund. Two years ago, it provided $9.7 million in joint venture equity to InLight Real Estate Partners to purchase the vacant property, which resulted in leverage of 45 percent of cost to reflect the risk, he added.

Today, the project is fully leased and a regional bank is providing refinancing at a 65 percent loan-to-value ratio. The interest rate is 180 basis points over SOFR, and the sponsor is purchasing an interest rate cap. “There was a lot of competition for that deal, and the banks were most aggressive,” Cornell noted. “But for stabilized industrial assets in general, there is a tremendous appetite from across the spectrum—life insurance companies, banks and debt funds.”

READ ALSO: CRE Investors Find Bright Spots Amid Headwinds

The health of retail real estate is also bringing back lenders, many of whom may have given up on the sector last decade. And while grocery-anchored assets remained most favored, virtually all types of shopping centers are in demand, including power centers, unanchored strips and trophy malls, observers say.

Even though cap rates have compressed about 50 basis points across all retail sectors, they remain slightly higher than multifamily and industrial, which makes deals easier to refinance, Darby added. He was recently involved in the $8 million refinancing of The Fountain, an 81,674-square-foot community center in Huntsville, Ala. The permanent fixed-rate deal, originated by a life insurance company, was structured to allow for flexible prepayment.

“Admittedly, retail real estate had a tough time for quite a while, but I think the pendulum has swung back,” he said. “When retail properties emerged from COVID-19, capital started realizing the sector was healthier than perceived.”

You must be logged in to post a comment.