Another Strong Year for CMBS?

Some caveats are challenging the outlook.

Commercial real estate has rediscovered its appetite for capital and, like in 2025, a sizable share of that borrowing is expected to flow through the CMBS market in 2026.

After a prolonged slowdown, the market rebounded sharply last year, signaling renewed confidence from both borrowers and investors. CMBS issuance surged to more than $150 billion in 2025, according to data from the CRE Finance Council, roughly 140 percent higher than 2024 levels. Industry execs see that rebound not as a one-off but as a foundation for further growth in the year ahead.

“This post-Global Financial Crisis high reflects both pent-up demand from borrowers and an insatiable appetite from credit investors seeking yield,” observed Clinton Jenkins, director of debt capital markets research at JLL. “As we turn the calendar to 2026, the CMBS market will continue to be an excellent source of liquidity for borrowers.”

The renewed momentum carries broader implications for CRE. The combination of attractive credit spreads and strong investor demand arrives at a critical moment as the market prepares to navigate roughly $900 billion in scheduled loan maturities in 2026, according to Jenkins. CMBS is likely to play a central role in refinancing activity this year.

Conditions for growth

A range of economic and real estate dynamics are converging in 2026 to support increased CMBS activity and commercial property borrowing more broadly. The most obvious one is the possibility that the Federal Reserve will lower interest rates further this year—perhaps twice. But that isn’t the entire picture. One of the most immediate catalysts is the approaching maturity wall.

“We anticipate strong SASB issuance, driven by the maturity and refinancing of peak-year loans originated in 2021 and 2022, alongside the maturity of 10-year SASB loans from 2016 and 2017,” said James Millon, co-head of capital markets for CBRE.

Further, CBRE projects 20 percent growth in CRE investment sales volume this year, supported by several factors: constructive, neutral leverage at acquisition; roughly $300 billion in net asset value trapped in closed-end vehicles that have exceeded their fund lives and now require exits; and renewed interest from global direct and indirect allocators returning to U.S. real estate. Together, these forces are likely to drive acquisition financing and, in turn, strengthen CMBS issuance volume.

“Significant capital inflows toward multifamily and industrial portfolios, as well as trophy office, data centers and retail will further bolster issuance,” Millon noted. “With base rates declining, borrowers will have the opportunity to refinance floating-rate loans put in place in 2023 and 2024, making CMBS an even more viable option.”

On the investor side, the market continues to offer compelling relative value compared to corporate bonds. While conduit issuance is expected to remain robust, competition from agencies, life companies, banks and debt funds is intensifying. That competitive landscape may influence loan structures.

“We could even see the return of 10-year loans as investors seek duration and show a willingness to concede on credit spreads,” Millon pointed out.

CMBS refi: A mixed picture

Demand for capital across commercial real estate is expected to remain strong in 2026, though the refinancing environment will vary meaningfully by property type and quality. According to recent Newmark research, overall debt demand is already elevated, setting the stage for continued—but more measured—growth in the year ahead.

“With debt volume already near record levels, the expectation is continued growth, though at a slower, more stable rate, while steady cap rates allow buyers and sellers to close bid-ask spreads, pushing up transaction volume,” Newmark notes in its 2026 Market Outlook.

That momentum, however, is uneven. Newmark researchers expect investment transaction volumes to increase for office and retail assets, while remaining stable for multifamily and industrial. On the debt side, volumes are projected to rise for multifamily and office, with industrial and retail holding steady.

Fundamentals for the U.S. office market have turned more positive, the same source shows, which should drive investment deals at a stronger pace than the sector has seen in years. For some office-backed CMBS loans, the improvement in the sector will ease refinancing, especially as (and if) interest rates come down. Class A and trophy properties do especially well in the refinancing game, and in CMBS refinancings.

In November, Rudin, one of New York City’s largest private commercial property owners, obtained an extension on its $425 million CMBS loan backed by 32 Avenue of the Americas, a 27-story, 1.2 million-square-foot tower in Tribeca. The loan will now mature in November 2029, assuming Rudin exercises both one-year extension options.

Also in November, Triple Five Group secured an extension on the $1.39 billion CMBS loan tied to the Mall of America, the 5.6 million-square-foot retail and tourism complex in Minnesota. The mall faced significant disruption during the pandemic and has reworked its CMBS debt before. Under the latest agreement, the loan’s maturity was also extended to 2029.

While these high-profile assets underscore CMBS lenders’ willingness to extend loans, the experience for more typical properties may be less forgiving. Extensions are expected to remain available, though often at higher costs, according to PERE Credit. Sponsors will increasingly be required to contribute additional equity, both to support refinancing and to fund asset-level reinvestment.

The long recovery

The 2020s have been a volatile period for the CMBS market, marked not only by sharp swings in issuance but also uneven delinquency trends across property types. The pandemic disrupted deal volume from pre-2020 highs, which had been driven by demand for capital across a broad range of asset classes. That diversity has since narrowed: Very little new office or mall development is taking place today compared to the years leading up to 2020.

In the immediate post-pandemic period, ultra-low interest rates and strong demand for industrial and multifamily assets fueled a surge in CMBS borrowing. Issuance peaked at $83 billion across 125 deals in the fourth quarter of 2021, a quarterly total that hasn’t been repeated since.

The CMBS market will continue to be an excellent source of liquidity for borrowers.

—Clinton Jenkins, Director of Debt Capital Markets Research, JLL

That momentum reversed quickly as interest rates spiked in 2022. By the first quarter of 2023, CMBS deal volume had fallen to a trough of $16 billion, another level that has yet to recur. Since then, issuance has recovered gradually, supported in part by easing rate conditions. But while deal activity has improved, delinquencies have also moved higher, reflecting lingering economic uncertainty and stress in specific property sectors.

“Property values have stabilized, but loan performance is impacted by shifting property fundamentals, including higher vacancy rates and slower rent growth,” said Reggie Booker, associate vice president of commercial real estate research at the Mortgage Bankers Association. “Delinquency performance remains highly dependent on property type and loan structure.”

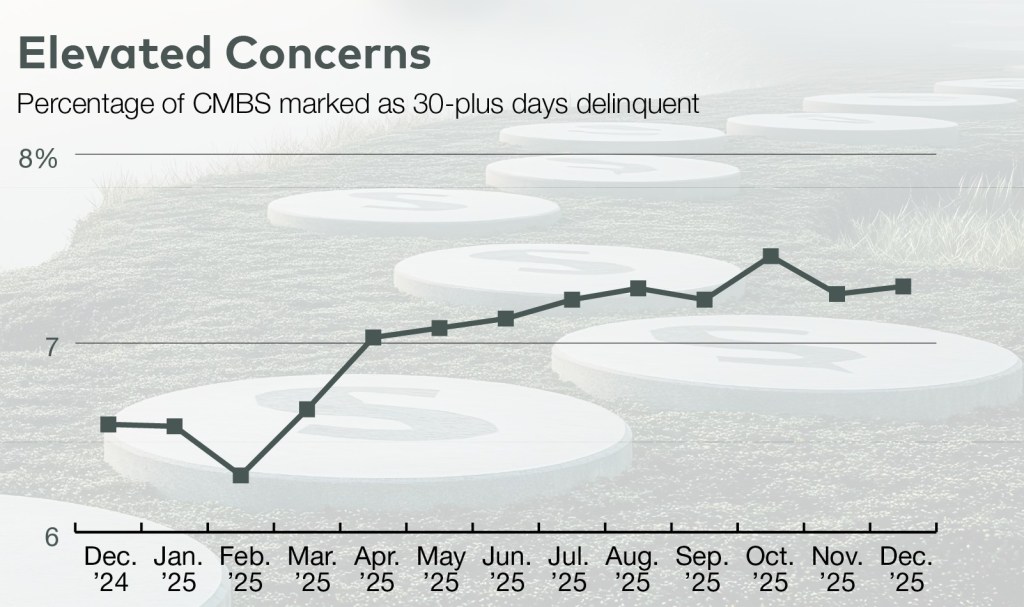

According to Trepp data, CMBS loans that are more than 30 days delinquent or already in REO status edged upward through 2025. Overall delinquencies reached 7.30 percent in December, up from 6.57 percent at the end of 2024. Even so, the rate remained well below the 10.34 percent peak recorded in 2012 following the Great Financial Crisis.

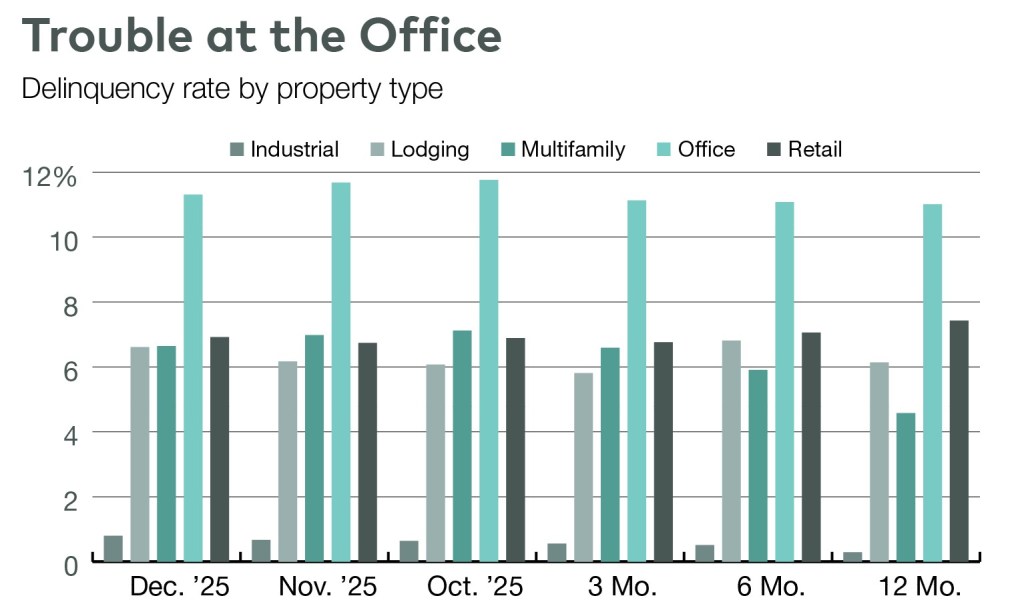

Delinquency trends continue to diverge by property type. In December, three of the five major sectors posted increases. Lodging saw the largest month-over-month jump, rising 44 basis points to 6.61 percent, compared to 6.14 percent a year earlier. Retail delinquencies increased 18 basis points to 6.92 percent, though that figure was 90 basis points below the sector’s peak in March 2025 and down from 7.43 percent in December 2024.

Industrial delinquencies, historically among the lowest given the sector’s strong fundamentals, also edged higher as pockets of overbuilding emerged. The rate increased 13 basis points in December to 0.8 percent, up from a scant 0.29 percent a year earlier.

Delinquency performance remains highly dependent on property type and loan structure.

—Reggie Booker, Associate Vice President of CRE Research, Mortgage Bankers Association

By contrast, office delinquencies recorded the largest monthly decline, falling 37 basis points to 11.31 percent in December, according to Trepp. A year earlier, the figure stood at 11.01 percent. Multifamily delinquencies also continued to trend lower on a month-to-month basis, dropping 34 basis points to 6.64 percent in December. A year ago, multifamily delinquencies were 4.58 percent, with the sector recording the largest year-over-year increase.

Monthly flow data suggests tentative stabilization. In December, newly delinquent CMBS loans totaled just under $2.9 billion, while nearly $3 billion of loans cured over the same period, resulting in a net delinquency decline of approximately $103 million, Trepp reports.

The year ahead is likely to reward disciplined underwriting, proactive asset management and realistic capital planning, making CMBS a central, but selective, source of liquidity as commercial real estate works through the next phase of its recovery.

You must be logged in to post a comment.