CRE 2025 Book of Rankings

Reading Between the Spreadsheet Lines

Throughout the year, Commercial Property Executive produces a set of rankings recognizing companies that are strong performers in key areas of the commercial real estate industry. Our rankings are unique in that they’re determined based on a weighted formula incorporating a number of important factors, so it’s no surprise they continue to be among our most disseminated and valued content.

We’ve compiled the past year’s rankings in a format that celebrates performance while also offering a handy, consolidated reference. We’ve also included some never-before-seen charts providing further insight into these sectors’ performance.

A closer look

The past year has been marked by uncertainty in the face of global economic upset. But the strongest companies did transact business where they saw opportunity to make smart decisions.

Securing financing is a critical component for any commercial real estate deal. Considering the economic rollercoaster of the past two years, solid banking relationships have never been more important, and the nature of individual deals matters.

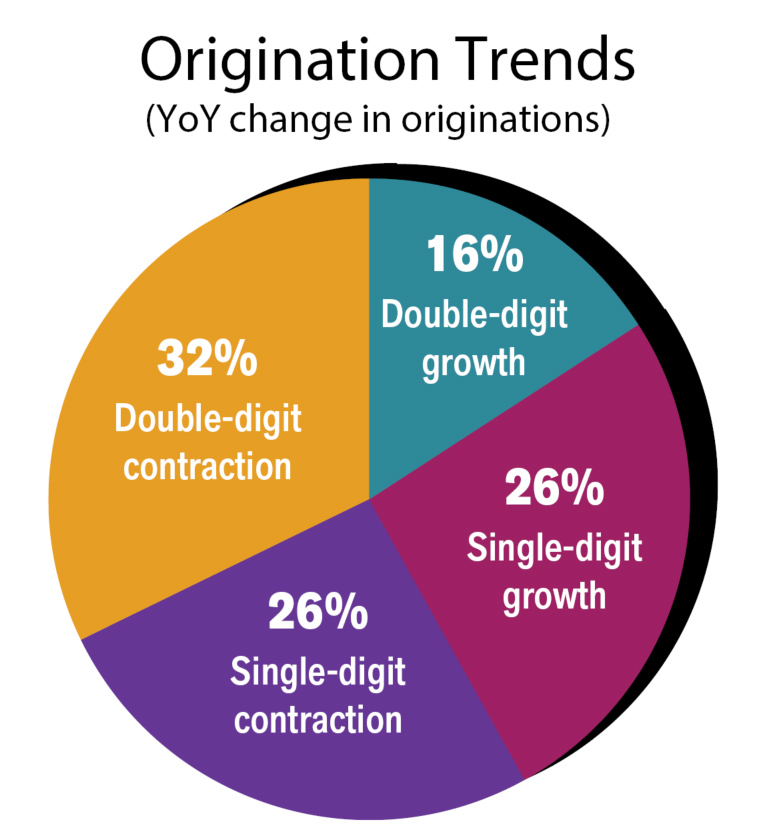

CPE’s 2025 Top Commercial Mortgage Banking and Brokerage Firms experienced mixed growth in originations last year but altogether transacted a relatively significant amount of business. The top 20 industry leaders closed $200 billion in deals during the 12 months ending in September 2024. And both mortgage bankers and brokers grew more optimistic over the course of the year: Nearly half said they expected a rise in origination volume in the coming year, although to varying degrees. Some are even aiming for significant increases.

While recent turbulence has made markets more uncertain, confidence among financial players grew as we approached year-end 2024 and moved into early 2025. CREFC’s sentiment index, for example, reached an all-time peak with its fourth-quarter reading. Other, similar gauges showed a doubling in optimism in early 2025.

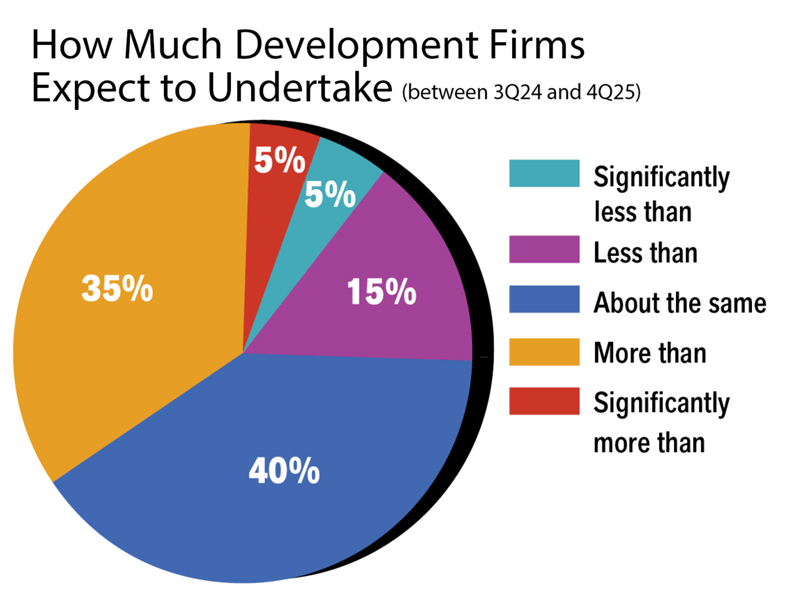

CPE’s 2024 Top Commercial Real Estate Developers list reflects similar optimism. Most of the top 20 companies expressed plans to sustain their current level of construction activity, with some even upping their output. Office, once a darling of the industry, is now the focus of redevelopment. Several states have launched initiatives to incentivize office conversions. Often, affordable housing is the expected outcome, although office-to-lab conversions are also gaining traction, especially in metros where life sciences and biotech rule.

Portfolios, as well, saw a bump last year. The top 30 companies in our 2024 Top Commercial Real Estate Owners ranking had a combined footprint of 2.3 billion square feet, which marked a significant rise from the 1.5 billion square feet one year prior. If nothing else, it at least reflects an acceleration in consolidation. This ranking is one of CPE’s longest running and reflects the growth of the industry. In October 2011, Simon Property Group led the Most Powerful Owners list with a 262 million-square-foot footprint. The latest leader, CBRE Investment Management, sported a whopping 701 million square feet.

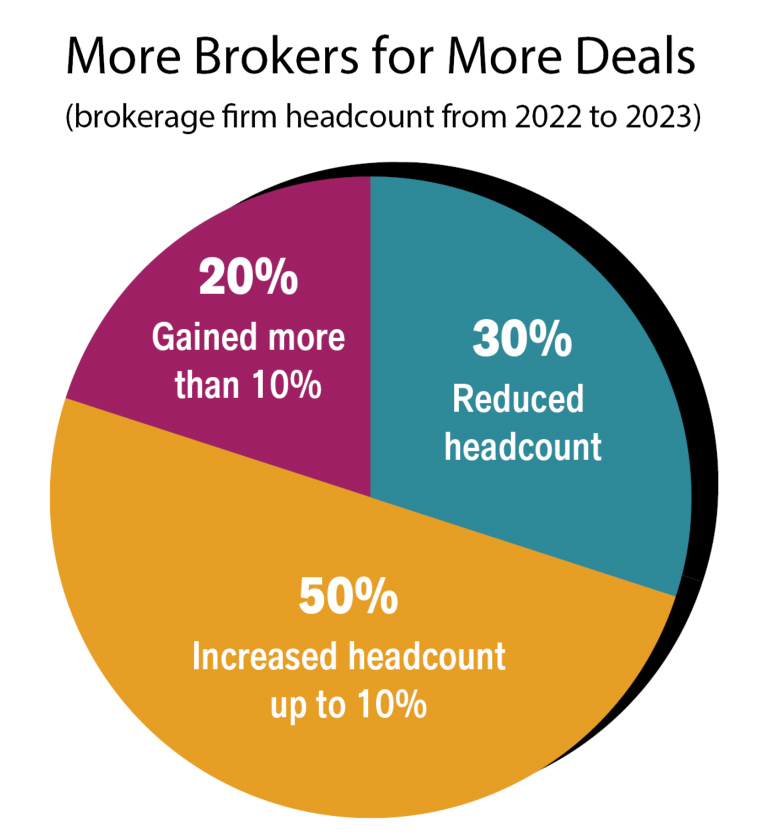

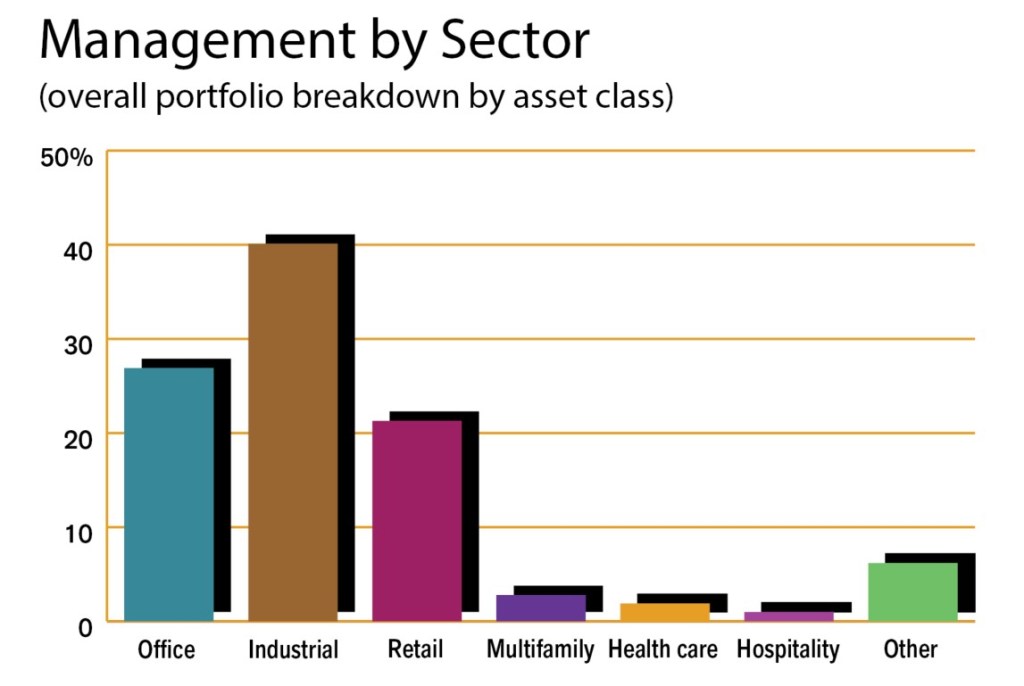

Our latest Top Commercial Property Management ranking showed both growth and consolidation, at a time when operations are critical to business performance. Sixty percent of the firms making the list expanded their portfolios. And the majority were diversified across property types, with only a few focused on a single sector. In addition, their portfolios tended to be well dispersed across the country.

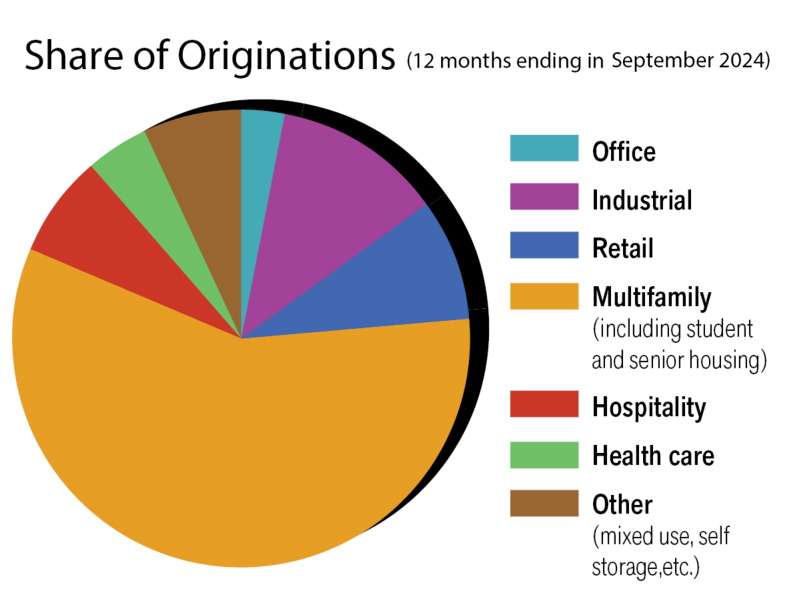

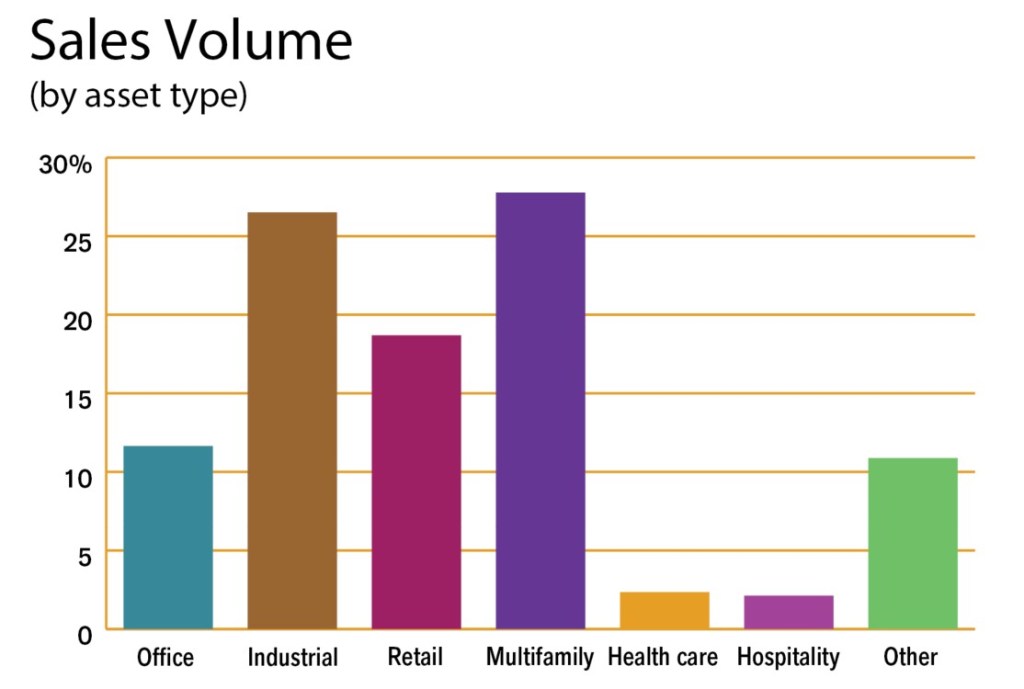

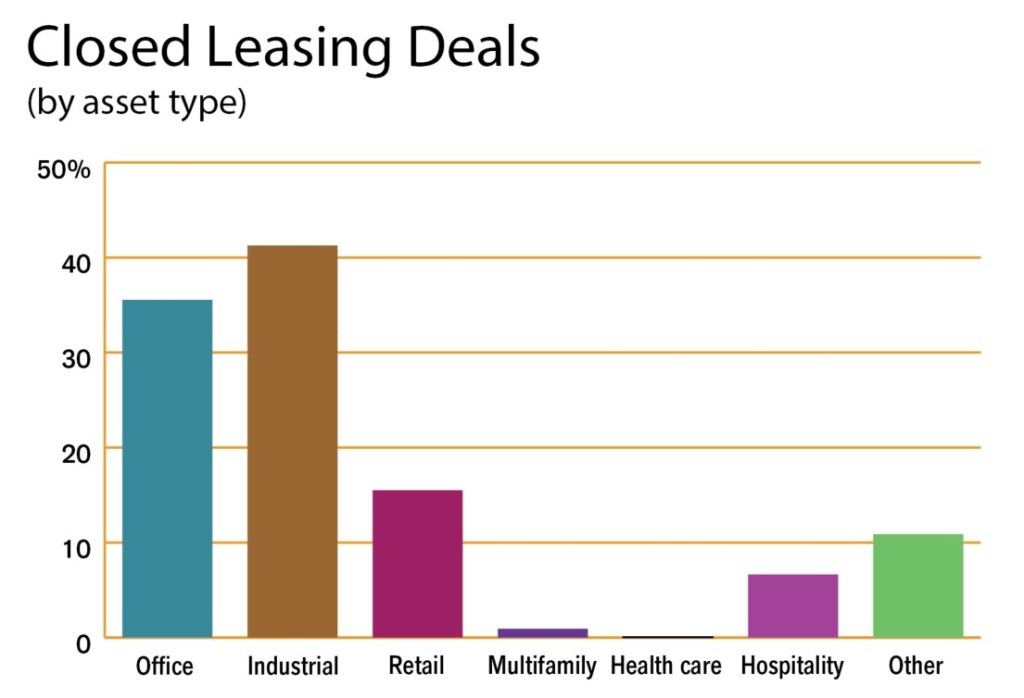

Finally, the 2024 Top CRE Brokerage Firms ranking celebrated top companies working in a rocky—or at least trickier-than-usual—environment, be it sales or leases. This ranking also revealed that the multifamily and industrial sectors continue to be experiencing their moment in the spotlight, despite what many would call a ”normalization.“ For example, more than three-quarters of the total sales volume arranged by the likes of Stream Realty Partners and Voit Real Estate Services—both in the top 20 for sales and leases combined—involved the industrial sector.

The big picture

These rankings highlight key parts of the roughly $22 trillion behemoth of an engine that is U.S. commercial real estate. CRE was the country’s fourth-largest asset type as of mid-2024, behind only equities, residential real estate and Treasury securities, according to the Federal Reserve. These companies are a big part of what keeps it solid.

As the industry continues to evolve, CPE strives to grow alongside it. In 2025, we’re not only bringing back the Leading Real Estate Law Firms but also launching a new ranking of Top Architects and Designers. Here’s to another interesting year!

About Our Methodology

All rankings relied on self-reported data from participating companies. Our rankings are calculated using a weighted formula based on a variety of factors relevant to the specified business area. They represent what we feel is a logical balance between firm growth and market share, as well as sector diversity or specialization. Ranking factors are not limited to the ones presented. All growth is determined based on a two-year window.

The 2025 CPE Top 20 Commercial Mortgage Banking and Brokerage Firms ranking incorporated total origination volume, coverage offered, growth in transaction volume and loan positioning, among other variables. Data reflects the time period between Oct. 1, 2023, and Sept. 30, 2024, and includes all originations, both as an intermediary and as a direct lender.

The Top Commercial Real Estate Developers ranking was based on factors including current and future plans, market value of projects completed and under construction as of midyear 2024, portfolio size, and geographic and property diversification.

The Top Commercial Property Owners ranking drew on considerations including total square footage owned, owned portfolio value, historic performance across a number of variables, and a focused or diversified participation in property sectors as of the second quarter of 2024.

The Top Commercial Property Management Firms of 2024 utilized total square footage and number of properties under management, occupancy, diversification or focus, and other variables from 2021 to 2023. Data incorporated both owner-operated properties and third-party management.

The Top Commercial Brokerage Firms formula evaluated both leasing and investment sales performance based on dollar value and square footage, along with number of brokers and offices, geographic and property sector diversification or focus, and other elements. The time period under consideration spanned fiscal year 2023 and the two years preceding it.

Debt Leaders Weather Challenging Conditions

Toward the end of 2024, loan originations started to find their footing. The volume increased 44 percent quarter-over-quarter in Q3 and was up 59 percent year-over-year, according to the Mortgage Bankers Association.

After a sluggish start, borrowing and lending activity gained speed moving into the second half of last year. In the third quarter of 2024, overall loan originations increased 44 percent compared to the second quarter and were up 59 percent year-over-year, according to a report by the Mortgage Bankers Association. Of course, lending volume varied by property type. Loans for health-care properties increased a whopping 510 percent, hospitality assets 99 percent, retail properties 82 percent, industrial assets 57 percent and multifamily 56 percent. Originations for the office sector, on the other hand, contracted 3 percent.

Meanwhile, more than half of the companies on CPE’s 2025 Top Commercial Mortgage Banking and Brokerage Firms ranking recorded negative growth in loan originations compared to the previous year, with an average drop of 11 percent. However, the other firms on the list saw growth averaging 25.7 percent. HREC Investment Advisors, which focuses solely on hospitality lending, reported the largest gains, with originations up 85.6 percent.

Newmark secured the No. 1 position this year due to a combination of factors. The firm provided loans totaling more than $48.4 billion during the 12 months ending in September 2024.

Newmark also increased its originations volume by an impressive 79.6 percent year-over-year during a turbulent time. CBRE, in second place, and Walker & Dunlop, in third place, provided a total of $61.4 billion in loans as direct lenders and intermediaries.

* Includes all originations, both as an intermediary and a direct lender, between 10/01/2023 and 09/30/2024. Note: Though we make every effort to include all major commercial lenders, several notable firms (among them JLL, Bank of America, KeyBank and ACORE Capital) did not participate this year.

FINANCING TYPES: D=Debt, E=Equity, H=Hybrid, X=Other

PROPERTY SECTORS: O=Office, I=Industrial, R=Retail, M=Multifamily, Ho=Hospitality, He=Health Care, X=Other

New Projects Persist Despite Uncertainty

Between 2021 and 2023, nearly 229 million square feet of office space came online across the U.S., according to CommercialEdge data. As of November 2024, there were 78.8 million square feet in completions, while 97 million feet were underway.

In the industrial space, 1.6 billion square feet were delivered throughout the U.S. between 2021 and 2023, versus nearly 426 million square feet in completions as of the end of November 2024, noticeably lower than the peaks of the previous years. More than 364 million square feet were under construction nationwide at that time, however, pointing to ongoing demand despite a slowdown in new starts.

The 20 companies on this list delivered a total of 226.5 million square feet of commercial real estate space over the same three-year period, with the total market value estimated at more than $65 billion. These developers also had a combined under-construction pipeline encompassing 136.5 million square feet as of June 2024.

Among the 20 firms, 80 percent indicated that they plan to maintain or increase their construction activity over the following six quarters. However, not all companies shared this optimistic outlook, with one firm even expecting a significant decrease. This mixed outlook highlights the varying risk appetite among today’s commercial real estate developers.

Trammell Crow Co. outpaced all developers by delivering twice as much commercial real estate space as any other firm from 2021 to 2023. As of June 2024, the company at the top of our ranking had a significant volume of space under construction. Its projects were mainly industrial but also included office, health care, retail, hospitality and other sectors.

Hines followed with 31.8 million square feet in completions between 2021 and 2023, and an under-construction pipeline of mostly industrial and office space totaling 19.2 million square feet. Tishman Speyer rounded out the top three, having delivered 16.8 million square feet, with an additional 11.4 million square feet underway.

*As of June 30, 2024. Note: Though we make every effort to include all major commercial developers, several notable firms (among them SL Green, Bridge Industrial and Prologis) did not participate this year.

KEY: O=Office, I=Industrial, R=Retail, H=Hospitality, He=Health Care, X=Other

Change Is a Constant for CRE Owners

The commercial real estate landscape continues to evolve due to several key factors, including increased demand for flexible workspaces and heightened attention to ESG. E-commerce remains a major force driving the industrial sector, and technology is being used to improve efficiency for logistics properties.

Finally, adaptive reuse projects are revitalizing urban areas by transforming underutilized properties into mixed-use developments.

By adapting to and staying ahead of these trends, commercial real estate owners can better position themselves to thrive in a competitive landscape.

Most firms in CPE’s 2024 Top Commercial Property Owners ranking have diversified their assets across different property types—from office properties to data centers—to reduce risk. Only five of the top 30 owners had portfolios focused on a single property type. Industrial real estate continues to be a hot sector, with 18 companies on our list owning assets in this category. Most owners also have properties in various regions across the U.S., and 11 have holdings in other countries.

Once again, CBRE Investment Management secured the top spot among commercial owners, with a diverse portfolio valued at nearly $109 billion and exceeding 701 million square feet as of the second quarter of 2024. Clarion Partners (296.7 million square feet valued at $108.9 billion) and AEW Capital Management (212 million square feet valued at $63.4 billion) rounded out the top three.

Note: Though we make every effort to include all major commercial real estate owners, several notable firms (among them Prologis, Blackstone and SL Green) did not participate this year.

KEY: O=Office, I=Industrial, R=Retail, H=Health Care, Ho=Hospitality, X=Other

Agents of Change in Turbulent Times

From making office spaces worth the commute to streamlining the experiential retail environment, commercial property management firms continue to adapt to shifting economic conditions and tenant needs.

In addition to employing traditional management best practices, managers are embracing new technologies, including artificial intelligence, to increase efficiencies, minimize disruptions and save costs.

As in previous years, the CPE Top Commercial Property Management Firms ranking includes third-party providers and owner-operators. Collectively, these companies managed more than 20.1 billion square feet of income-producing properties in 2023.

CBRE maintained the top position with a global portfolio encompassing 7.3 billion square feet under management. The firm’s portfolio is primarily industrial space, followed by office, retail, health care, hospitality, data centers and multifamily.

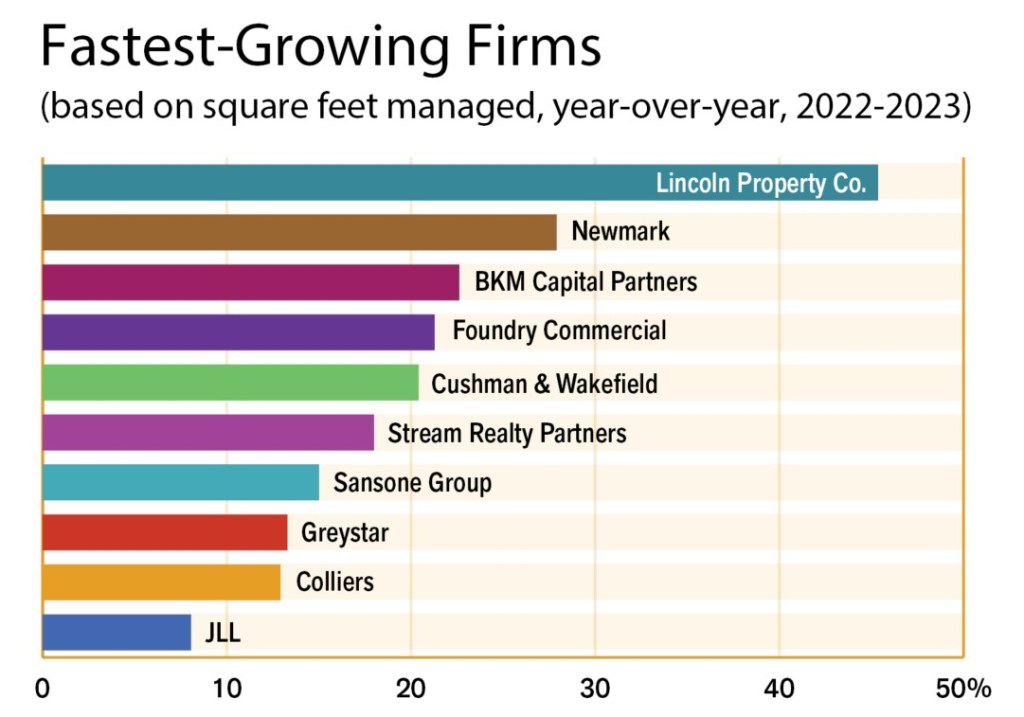

Cushman & Wakefield and Colliers secured the second and third positions, managing portfolios of more than 6.1 billion and nearly 2.6 billion square feet, respectively. Lincoln Property Co. expanded the fastest between 2021 and 2023. Other companies with notable growth include Newmark, BKM Capital Partners, Foundry Commercial and Cushman & Wakefield.

Overall, 60 percent of the commercial property management firms on the list increased their portfolios compared to the previous year. Additionally, 76.7 percent expanded compared to their 2021 figures. Most firms on the list manage a variety of asset types. The highest concentration is in industrial properties, followed by office and retail.

Note: Though we make every effort to include all major property management companies, several notable firms (among them Avison Young, SVN International and Prologis) did not participate this year.

KEY: O=Office, I=Industrial, R=Retail, M=Multifamily, H=Health Care, Ho=Hospitality, X=Other

Uncertainty Influences Deal-Making

For CRE, the past five years have been marked by constant adjustment.

The pace of investment started slowing in 2023, particularly compared to the exceptional growth of the previous two years. Leasing volume, however, showed variation across real estate sectors.

After interest rates went up, the high cost of capital dampened sales. Office sales totaled $33.8 billion in 2023, a significant drop from 2022’s $86.6 billion, according to CommercialEdge data. Meanwhile, the national office vacancy rate increased 180 basis points, closing that year at 18.3 percent.

The industrial sector saw a shift from a remarkable 2021 and 2022, but it still performed reasonably well in 2023. Rent growth continued, with national in-place rents averaging $7.70 per square foot at the end of that year, marking a 7.4 percent increase. The national industrial vacancy rate stood at 4.6 percent. Sales totaled $52.1 billion.

CPE compiled a list of the brokerage companies facilitating the majority of sales and leases during this rollercoaster of a year. The top 20 firms accounted for $449.7 billion in investment sales, for instance. The figure marked a significant drop compared to 2022 and was also a far cry from 2021’s $855.7 billion. Multifamily drew the most attention, closely followed by industrial, retail, office, health care and hospitality.

CBRE retained its well-established first position. The firm completed a striking $153.7 billion in investment sales in 2023, accounting for 34 percent of all investment activity. CBRE also closed lease transactions totaling $131.6 billion. Cushman & Wakefield and Colliers rounded out the top three. Cushman handled $53.7 billion in transactions and leased more than 775 million square feet, valued at $73.8 billion. Meanwhile, Colliers arranged $54.3 billion in sales and brokered leases for more than 780 million square feet, with a value of $47.7 billion.

Note: The following noteworthy firms did not submit responses: JLL, Eastdil Secured and Avison Young.

KEY: O=Office, I=Industrial, R=Retail, M=Multifamily, H=Health Care, Ho=Hospitality, X=Other

Download the pdf “CRE 2025 Book of Rankings“

You must be logged in to post a comment.