2025 Office Net Lease Sales Volume and Cap Rates

How the sector is faring, according to the most recent data.

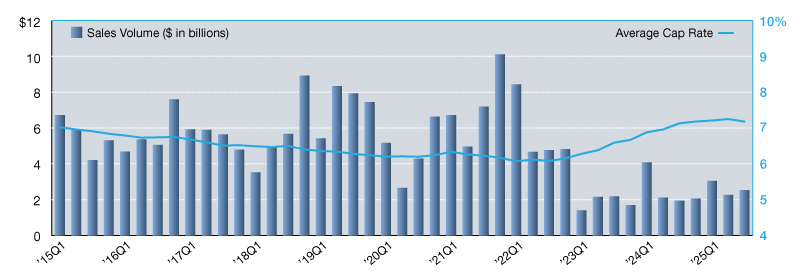

The single-tenant office sector posted $2.5 billion in third-quarter sales volume, up 11.5 percent from the second quarter and nearly 28 percent year-over-year. Cap rates declined, falling 7 basis points to 7.18 percent, though they remain up 5 basis points year-over-year.

The West region dominated transaction activity in the third quarter, recording $864.0 million in volume and accounting for 34.2 percent of the total. The Southeast followed with $550.0 million, representing 21.8 percent of overall volume. The Midwest ranked third with $510.3 million, or 20.2 percent, while the Northeast recorded $255.5 million, representing 10.1 percent. The Southwest contributed $199.0 million, or 7.9 percent of total volume, and the Mid-Atlantic region trailed with $149.5 million, accounting for 5.9 percent.

READ ALSO: Top 10 Markets for Office Deliveries in 2025

By region, cap rates ranged from a low of 6.61 percent in the West to a high of 8.03 percent in the Midwest. Cap rates were mixed across all regions. Average cap rates are up 110 basis points from the recent low of 6.08 percent recorded in the first quarter of 2022.

Private buyers accounted for 58 percent of single-tenant office acquisitions through the third quarter of 2025, followed by institutional investors at 23 percent. The private share increased sharply by 29 percent from 2024, while institutional investment activity increased by 4 percent over the same period. REIT/Listed acquisitions fell from 26 percent of investment activity in 2024 to 2 percent as of the third quarter of 2025.

—Posted on Feb. 26, 2026

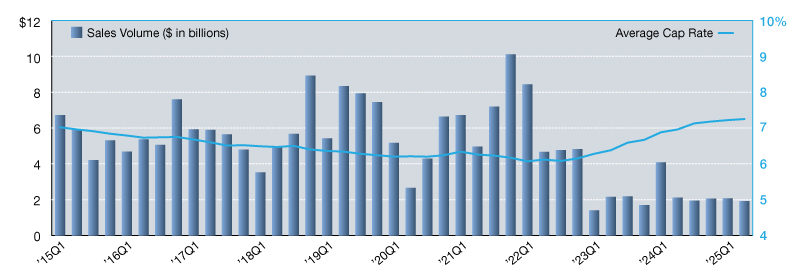

Single-tenant office investment sales totaled $1.9 billion in the second quarter, down 7.3 percent from the previous quarter and 9.1 percent year-over-year. The West region led in volume, with nearly $860 million in recorded transactions. One of the quarter’s highest-profile deals included the sale of a Class A office building in Bellevue, Wash.’s mixed-use Spring District—a recently constructed nine-story property fully leased by Meta—for more than $900 per square foot.

READ ALSO: 2026 CRE Outlook: Key Expectations for the Year Ahead

Cap rates rose three basis points to an average of 7.25 percent, continuing a slow upward climb. The average is now 27 basis points higher than a year ago and 118 basis points above the market’s low in early 2022. While pricing remains under pressure, the pace of change has moderated in the past six to nine months.

Private buyers reclaimed market share from REITs in the first half of 2025. Compared to last year, when REITs accounted for 26 percent of office acquisitions and private buyers 29 percent, dynamics have shifted significantly.

Office REIT buyer pool shrinks

Currently, REITs make up just 2 percent of the single-tenant office buyer pool, allowing private investors to reclaim dominant market share with 43 percent. With the pullback from REITs, the market has also seen an influx of institutional buyer activity over the last six months. This group represents 34 percent of the single-tenant office buyer pool, which is the highest ratio seen for institutional investors since 2016.

The office market continues to face headwinds from elevated vacancy and shifting demand, particularly in urban areas and central business districts. However, as illustrated by the Bellevue sale, stabilized assets with long-term leases in secondary and tertiary markets are still attracting capital, especially from private buyers seeking yield. Additionally, well-located health-care assets and medical office buildings continue to drive activity across the sector and are expected to contribute meaningfully to second half investment volume.

John Tagg is the Research Manager at Northmarq. He is responsible for coordinating the production and distribution of research reports that support the company’s commercial real estate brokerage and investment sales teams across local offices nationwide.

—Posted on November 24, 2025

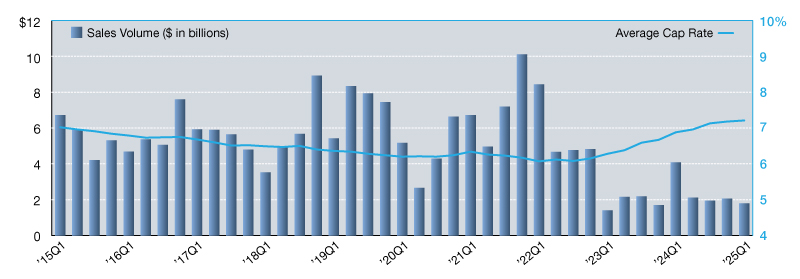

The single-tenant office sector continued to grapple with significant challenges in first quarter 2025, as investor caution dampened transaction activity. Total sales volume fell to $1.8 billion, marking a 13 percent decline from fourth-quarter 2024 and a dramatic 56.2 percent decrease year-over-year. This ongoing contraction reflects persistent headwinds in tenant demand, rising vacancies and sluggish corporate leasing activity.

READ ALSO: Global Trade Rebalancing

Cap rates within the sector edged higher for the 10th consecutive quarter, averaging 7.21 percent at the close of first-quarter 2025. However, the pace of cap rate expansion has slowed dramatically. When comparing the 3-basis-point increase reported in the most recent quarter to a 30-point rise in the nine months preceding, trends suggest the greatest volatility is now behind us.

Buyer distribution data highlighted a surprising shift in the profile of active participants in the single-tenant office sector. Institutional investors dominated early 2025 acquisitions, making up 43 percent of total buyers. Predictions in late 2024 called for this buyer segment to reduce their exposure to office space this year. Instead, we’ve seen institutional investors involved in both large and small transactions across the country – from small dialysis facilities to corporate campus sale leasebacks.

Office investor sentiment

Private buyers, with 31 percent of the sector’s market share, displayed strong engagement to start the year, while REITs were entirely absent, illustrating their heightened uncertainty and limited long-term confidence in the asset class.

Ongoing tenant downsizing and challenges in backfilling vacant spaces weigh heavily on investor sentiment. Many office properties are struggling to align lease terms with market demands, leading to extended periods of underperformance. To further complicate matters, billions in loans are set to mature in 2025, putting additional pressure on current owners.

Looking forward, the net lease office sector will require creative repositioning strategies to regain investor interest and stabilize leasing fundamentals. However, with macroeconomic uncertainties and persistent financing hurdles, near-term activity is expected to remain muted.

—Posted on July 29, 2025

You must be logged in to post a comment.