2022 Net Lease Industrial Sales and Cap Rates

Where are these trends heading? The latest update from Stan Johnson Co.

Source: Stan Johnson Co. Research, Real Capital Analytics

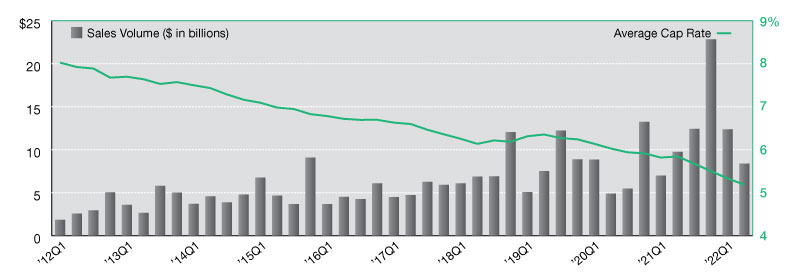

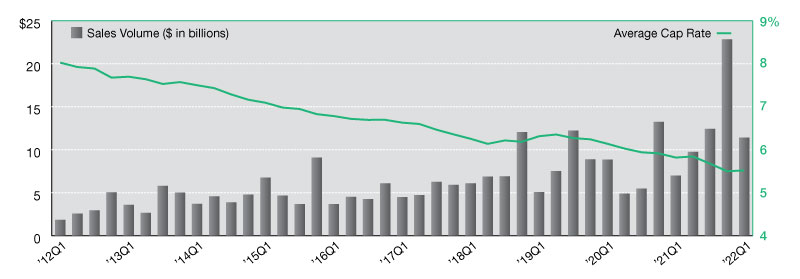

Industry experts have been suggesting for months that a slowdown is looming for the industrial sector. Several headwinds continue to impact the market, and investment sales activity in the first half of 2022 have indeed witnessed declines from recent record-setting periods. In second quarter 2022, the single-tenant industrial sector reported $8.4 billion in transaction volume. This was down 32.2 percent from first quarter 2022, when approximately $12.4 billion in sales were reported. When compared to the astronomically high activity reported at year-end 2021 and studying the $52-billion-year, the industrial sector looks to be significantly off-pace midway through 2022. However, strip out just fourth quarter 2021, and the market is performing equal to the five-year trailing quarterly average and outpacing the 10-year average.

Current activity appears to be right-sizing, returning to levels more in-line with a hot, but not overly frothy, market. Additionally, if investment activity doesn’t decline further in the second half of the year, 2022 could easily become the second strongest year on record. As tenants grapple with increasing rents and low vacancy, investors are watching interest rates and inflation, trying to make deals make sense. Part of today’s pullback in sales volume is likely influenced by the repricing of deals as buyers are no longer able to lock in debt at yesterday’s costs. However, with demand still very high and new supply lagging, there is no shortage of bidders on most of today’s offerings.

John Tagg is the Research Manager at Northmarq. He is responsible for coordinating the production and distribution of research reports that support the company’s commercial real estate brokerage and investment sales teams across local offices nationwide.

—Posted on Jul. 29, 2022

Source: Stan Johnson Co. Research, Real Capital Analytics

To say activity in the single-tenant industrial market has been strong in recent years is an understatement. The growing importance of the sector–from manufacturing to last-mile delivery and everything in between–has real estate investors scrambling to acquire industrial assets. Newly built and second-generation facilities are both in high demand, and with the scarcity of supply in primary markets, investors are relaxing their criteria. They are pursuing opportunities in secondary and tertiary markets, outlying suburbs of primary markets, and evaluating rural markets too, as consumers in all geographies have come to expect fast access to goods.

In first quarter 2022, the net lease industrial sector posted more than $11.4 billion in investment sales. Despite activity falling 50 percent quarter-to-quarter, sales volume is still incredibly strong–fourth quarter 2021, with $22.8 billion in sales, was simply an unprecedented anomaly. Activity levels over the last several quarters accurately illustrate current demand, and in just the last 12 months, the single-tenant industrial sector has logged $56.5 billion in sales. To put this in perspective, this is roughly the same amount as the entire net lease market, with all property types combined, recorded in the three-year span from 2009 to 2011. The industrial sector is expected to continue driving activity levels for the net lease market in both the short and long-term. Additionally, cap rates, which now sit just two basis points above the all-time record low of 5.5 percent, should continue to be the lowest rates compared to other property sectors even if we begin to see them trend upward.

—Posted on Apr. 29, 2022

You must be logged in to post a comment.